Classification and Logistic Regression

EE 541 - Unit 5

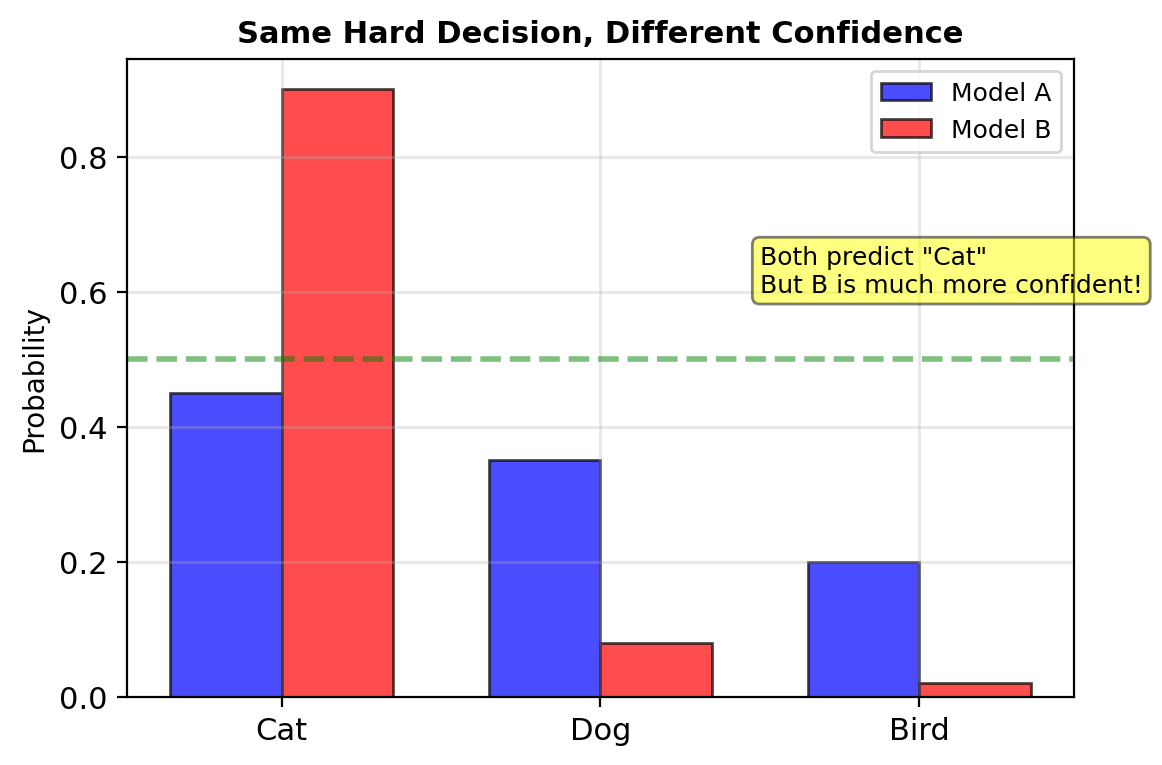

Threshold Rules Convert Probabilities to Labels

Classification pipeline:

- Model: Estimate \(P(y=1|\mathbf{x})\)

- Training: Learn parameters from data

- Inference: Compute \(p = P(y=1|\mathbf{x}_{\text{new}})\)

- Decision: Choose \(\hat{y} \in \{0, 1\}\)

The decision rule maps \(p\) to \(\hat{y}\):

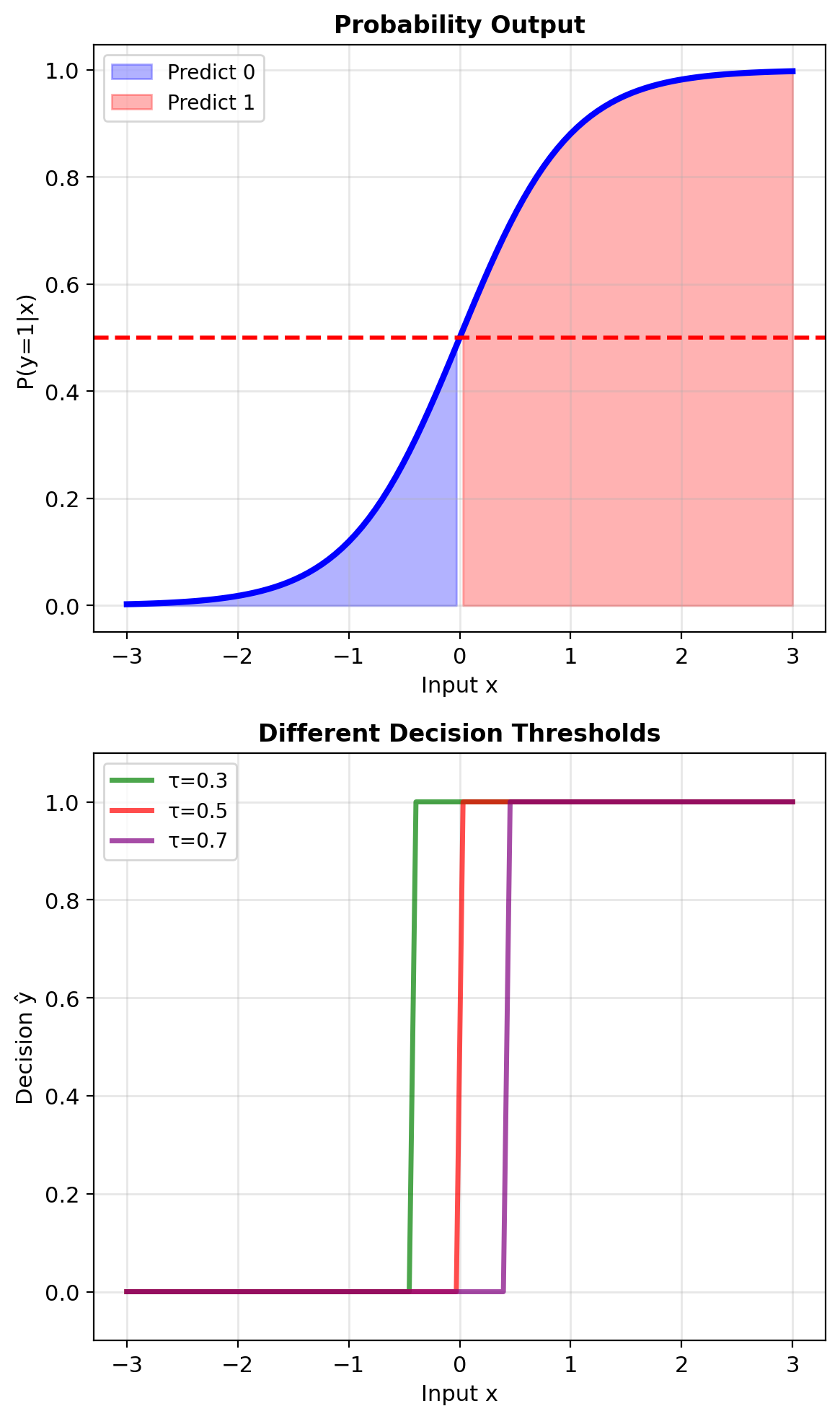

Simple threshold: \[\hat{y} = \begin{cases} 1 & p > 0.5 \\ 0 & p \leq 0.5 \end{cases}\]

This assumes all errors cost the same

Example: Credit card fraud

- False positive: Block legitimate transaction ($10 cost)

- False negative: Approve fraud ($1000 loss)

Optimal threshold depends on these costs

Different thresholds lead to different decisions

Decision Theory – States, Actions, Rules, and Loss

States (observations): \(\Omega = \{\omega_1, \omega_2, \ldots\}\)

- True class labels: \(y \in \{0, 1\}\) or \(\{1, 2, \ldots, K\}\)

Actions: \(\mathcal{A} = \{a_1, a_2, \ldots\}\)

- Predicted labels: \(\hat{y}\)

- Or “reject” option (defer to human)

Decision rule: \(\delta: \mathcal{X} \to \mathcal{A}\)

- Maps observations to actions

Loss function: \(L: \Omega \times \mathcal{A} \to \mathbb{R}\)

- Cost of action \(a\) when true state is \(\omega\)

Objective: Minimize expected loss \[R(\delta) = \mathbb{E}[L(Y, \delta(X))]\]

Bayes risk: Minimum achievable expected loss \[R^* = \inf_\delta R(\delta)\]

Bayesian Decision Theory Foundation

Bayes risk minimization:

Given observation \(\mathbf{x}\), choose action to minimize expected loss:

\[\delta^*(\mathbf{x}) = \arg\min_{a \in \mathcal{A}} \mathbb{E}[L(Y, a) | \mathbf{X} = \mathbf{x}]\]

Expanding the expectation: \[= \arg\min_{a} \sum_{k} L(k, a) \cdot P(Y=k|\mathbf{x})\]

For binary classification with \(y \in \{0, 1\}\): \[\delta^*(\mathbf{x}) = \arg\min_{a \in \{0,1\}} \left[ L(0,a)(1-p) + L(1,a)p \right]\]

where \(p = P(Y=1|\mathbf{x})\)

Optimal decisions depend on:

- Posterior probabilities \(P(Y=k|\mathbf{x})\)

- Loss function \(L(k, a)\)

Bayes rule minimizes expected loss at each point

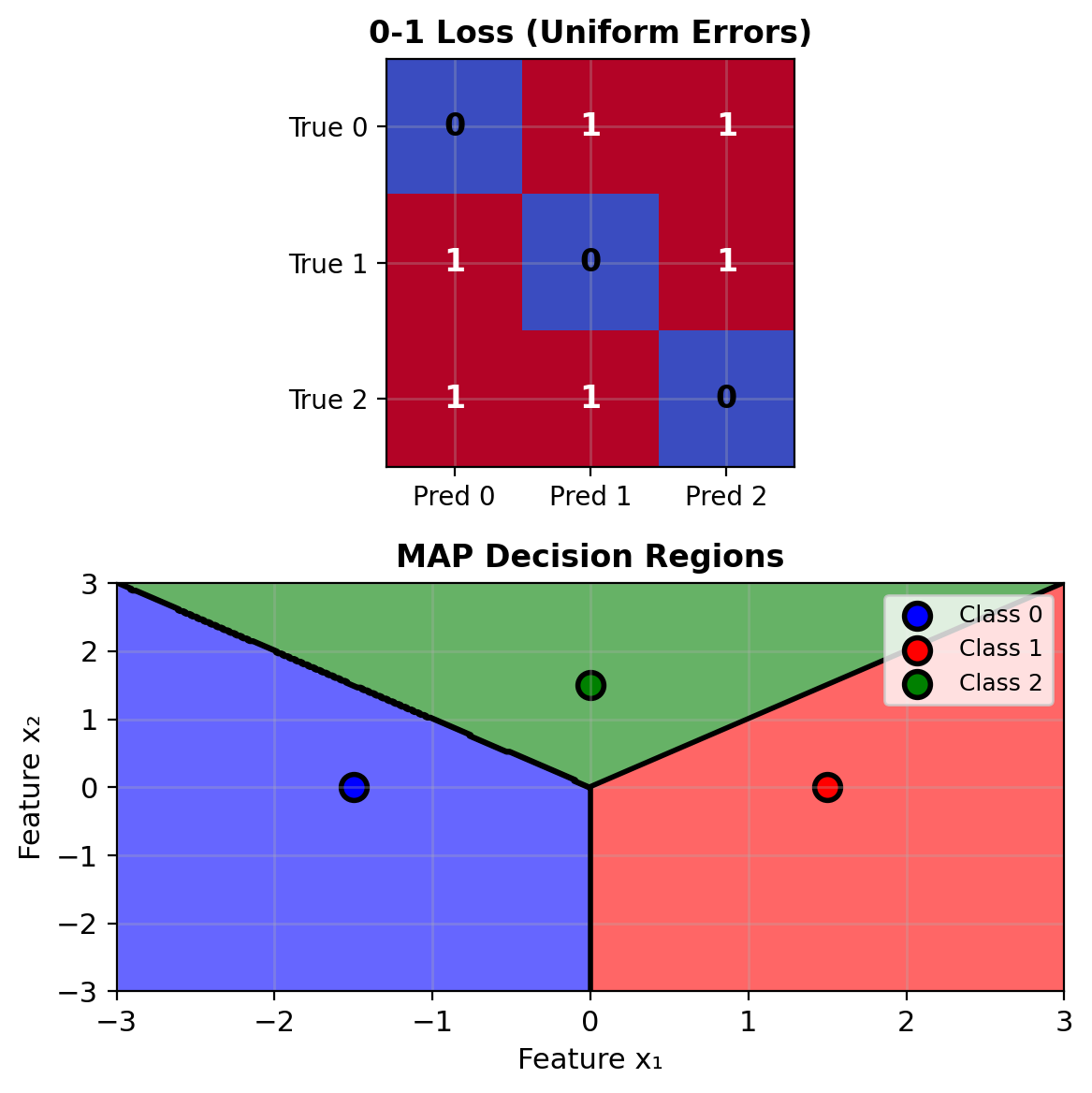

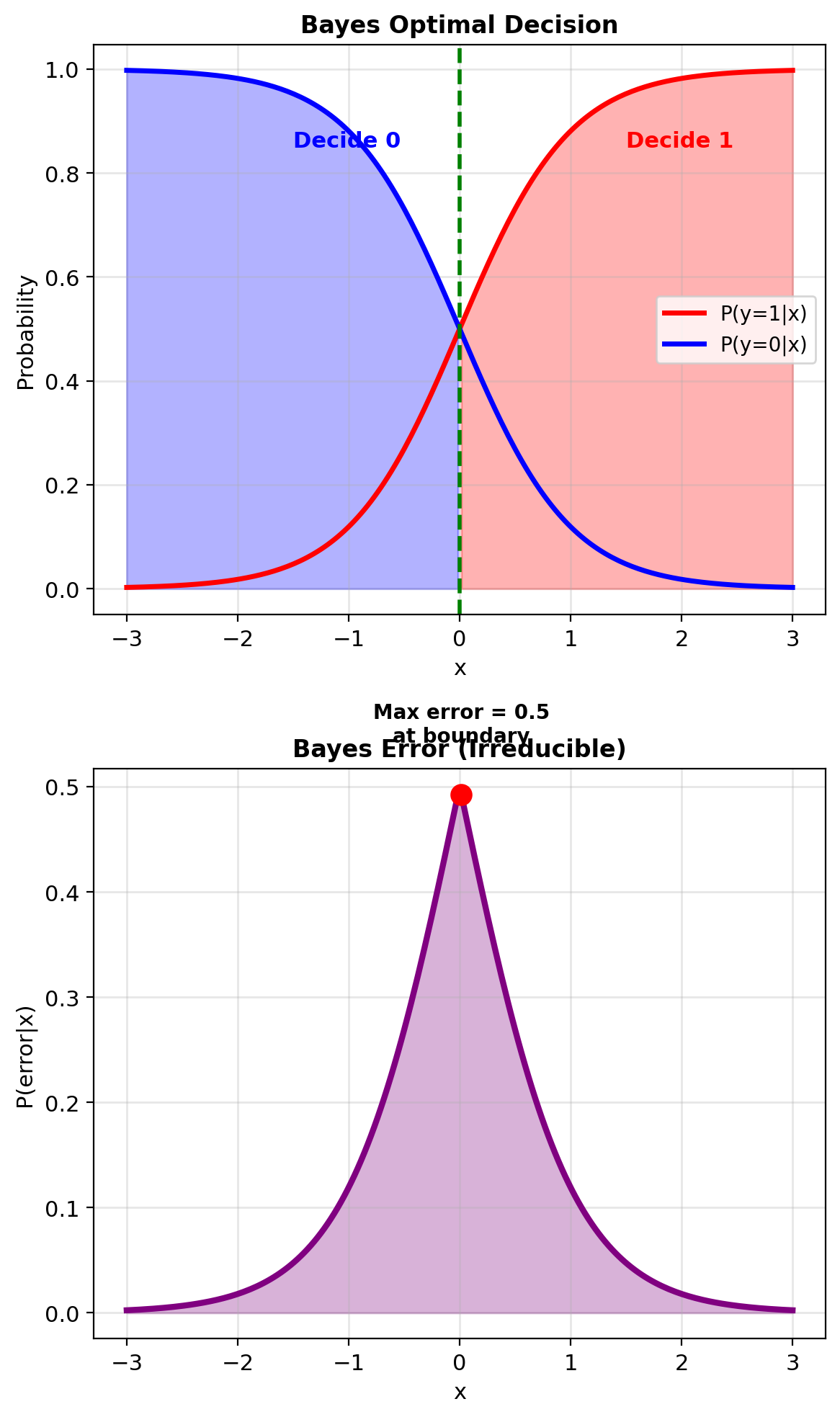

Uniform Loss Leads to MAP Rule

0-1 Loss (uniform error cost): \[L(y, \hat{y}) = \begin{cases} 0 & \text{if } y = \hat{y} \\ 1 & \text{if } y \neq \hat{y} \end{cases}\]

Expected loss for action \(a\): \[\mathbb{E}[L(Y, a) | \mathbf{x}] = \sum_{k \neq a} P(Y=k|\mathbf{x}) = 1 - P(Y=a|\mathbf{x})\]

Minimizing expected loss: \[\delta^*(\mathbf{x}) = \arg\min_a [1 - P(Y=a|\mathbf{x})] = \arg\max_a P(Y=a|\mathbf{x})\]

This is the MAP rule!

\[\boxed{\delta_{\text{MAP}}(\mathbf{x}) = \arg\max_k P(Y=k|\mathbf{x})}\]

MAP minimizes error probability when all errors cost the same

Bayes error rate (irreducible error): \[\epsilon^* = \mathbb{E}[1 - \max_k P(Y=k|X)]\]

No classifier can do better — this is the error from class overlap

Each region: highest posterior probability wins

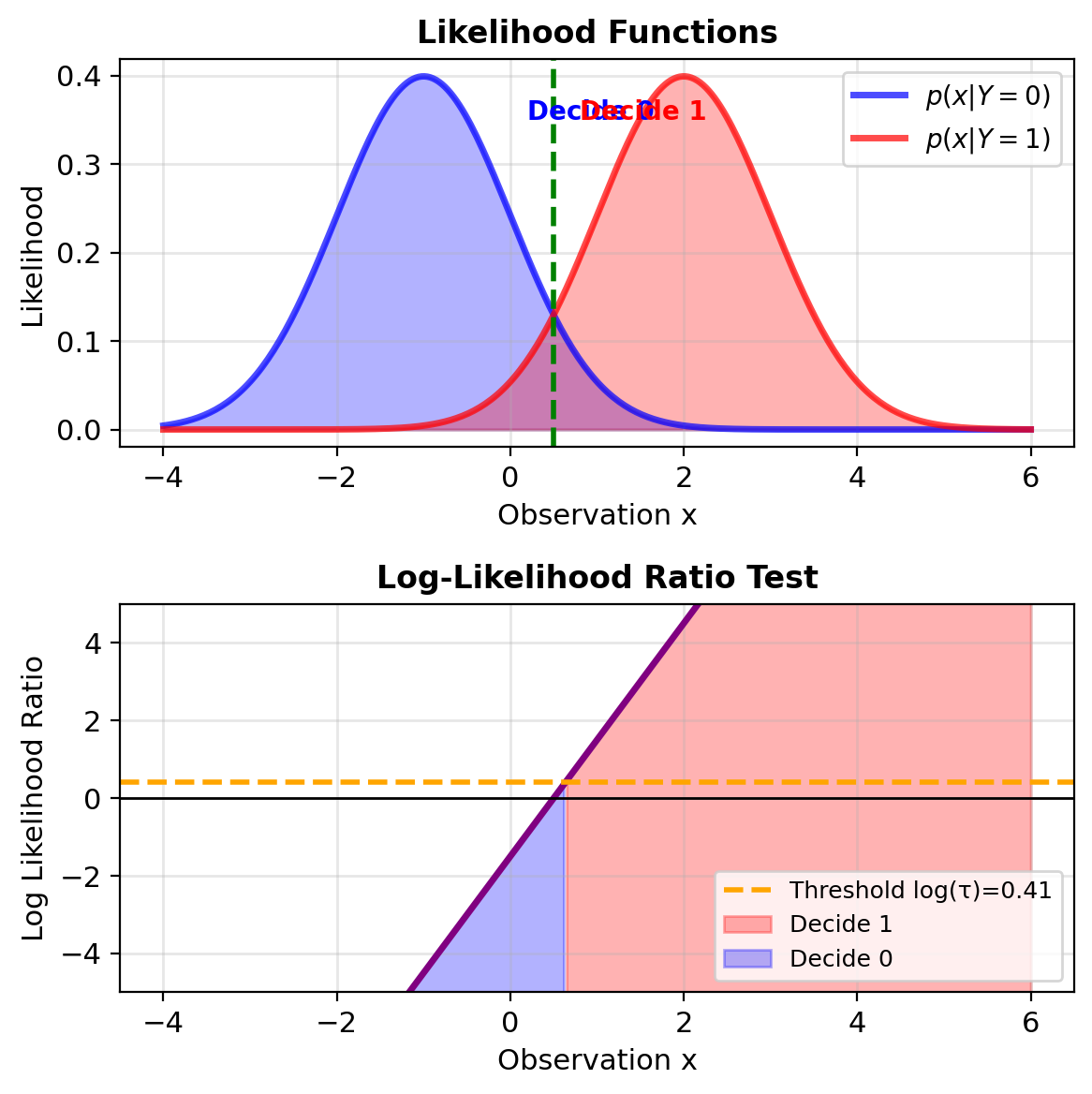

Likelihood Ratio Test for Binary Classification

Binary Bayes decision rule:

Choose class 1 if “expected loss of choosing 1” < “expected loss of choosing 0”:

\[L_{01}P(Y=0|\mathbf{x}) < L_{10}P(Y=1|\mathbf{x})\]

where \(L_{ij}\) = loss of predicting \(j\) when true class is \(i\)

Using Bayes theorem: \[P(Y=k|\mathbf{x}) = \frac{p(\mathbf{x}|Y=k)P(Y=k)}{p(\mathbf{x})}\]

Rearranging: \[\frac{p(\mathbf{x}|Y=1)}{p(\mathbf{x}|Y=0)} > \frac{L_{01}P(Y=0)}{L_{10}P(Y=1)}\]

Likelihood Ratio Test: \[\boxed{\Lambda(\mathbf{x}) = \frac{p(\mathbf{x}|Y=1)}{p(\mathbf{x}|Y=0)} \underset{H_0}{\overset{H_1}{\gtrless}} \tau}\]

where threshold \(\tau = \frac{L_{01}P(Y=0)}{L_{10}P(Y=1)}\)

Log-likelihood ratio (more stable): \[\log \Lambda(\mathbf{x}) = \log p(\mathbf{x}|Y=1) - \log p(\mathbf{x}|Y=0)\]

Linear boundary in log-space → stability

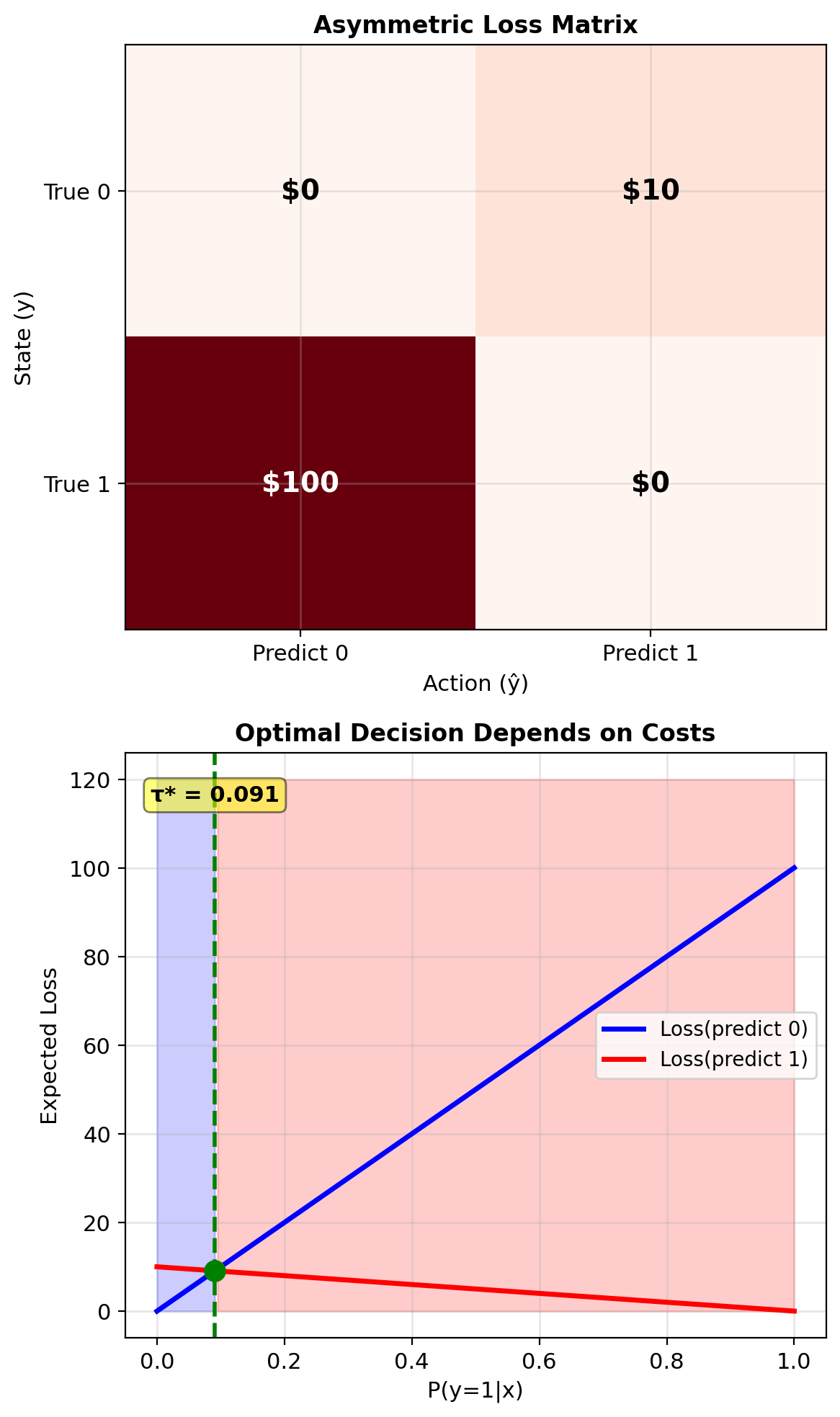

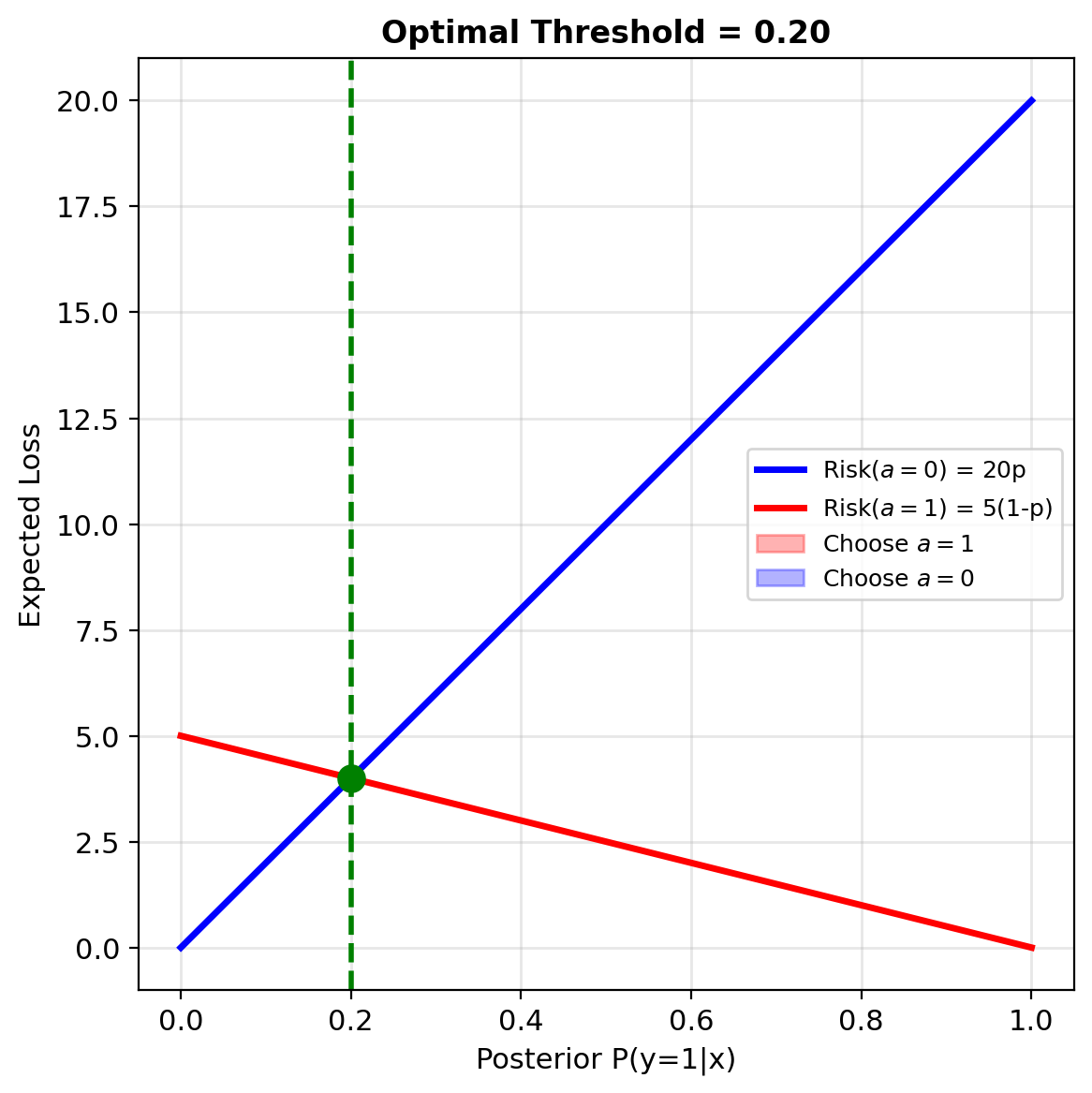

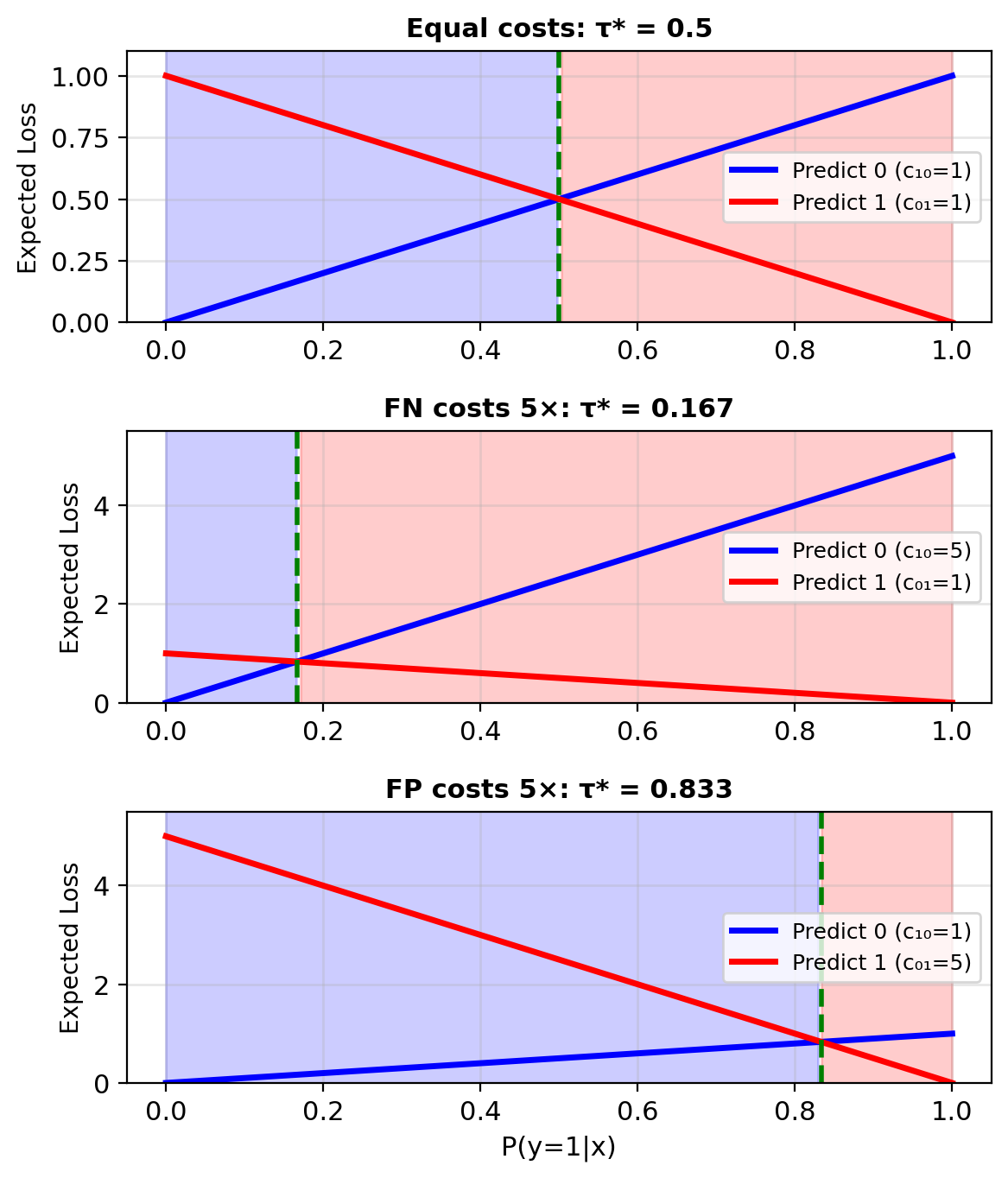

When Errors Have Different Costs

Binary classification with costs:

\[L = \begin{bmatrix} 0 & c_{01} \\ c_{10} & 0 \end{bmatrix}\]

where:

- \(c_{01}\): Cost of false positive (say 1 when true is 0)

- \(c_{10}\): Cost of false negative (say 0 when true is 1)

Expected loss of predicting 1: \[R_1(\mathbf{x}) = c_{01} \cdot P(y=0|\mathbf{x})\]

Expected loss of predicting 0: \[R_0(\mathbf{x}) = c_{10} \cdot P(y=1|\mathbf{x})\]

Optimal decision: Predict 1 if \(R_1(\mathbf{x}) < R_0(\mathbf{x})\)

\[c_{01}(1-p) < c_{10} \cdot p\] \[p > \frac{c_{01}}{c_{01} + c_{10}}\]

Optimal threshold: \(\tau^* = \frac{c_{01}}{c_{01} + c_{10}}\)

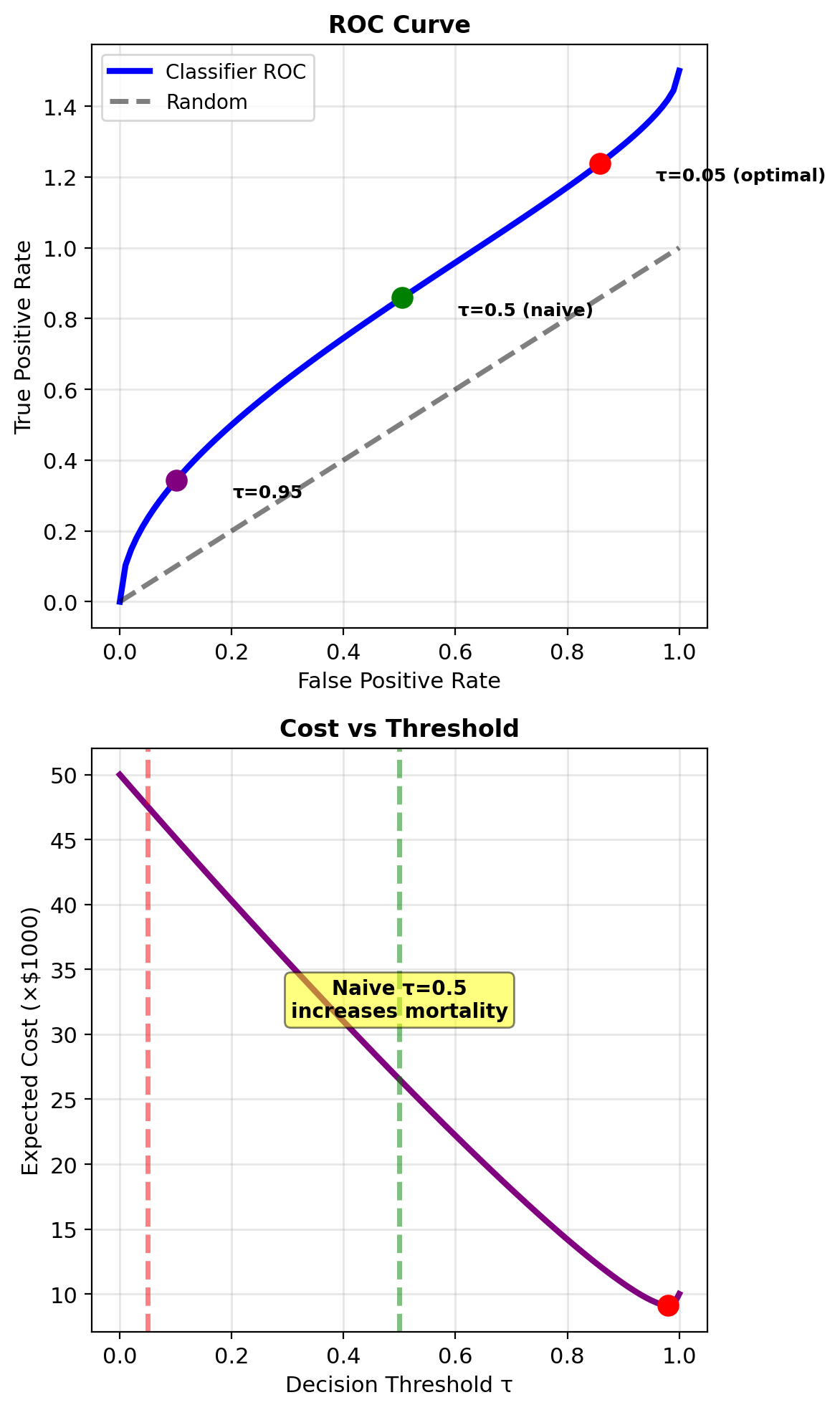

Medical Diagnosis as a Decision Problem

Cancer screening scenario:

- State: Cancer (1) or Healthy (0)

- Action: Treat (1) or Don’t treat (0)

Realistic costs:

- False negative (miss cancer): Death = $1,000,000

- False positive (unnecessary treatment): $50,000

- True positive (treat cancer): $50,000

- True negative (no treatment): $0

Loss matrix: \[L = \begin{bmatrix} 0 & 50,000 \\ 1,000,000 & 50,000 \end{bmatrix}\]

Note: treatment cost even for true positives

Optimal threshold: \[\tau^* = \frac{50,000}{50,000 + 950,000} = 0.05\]

Treat if \(P(\text{cancer}|\text{test}) > 0.05\)

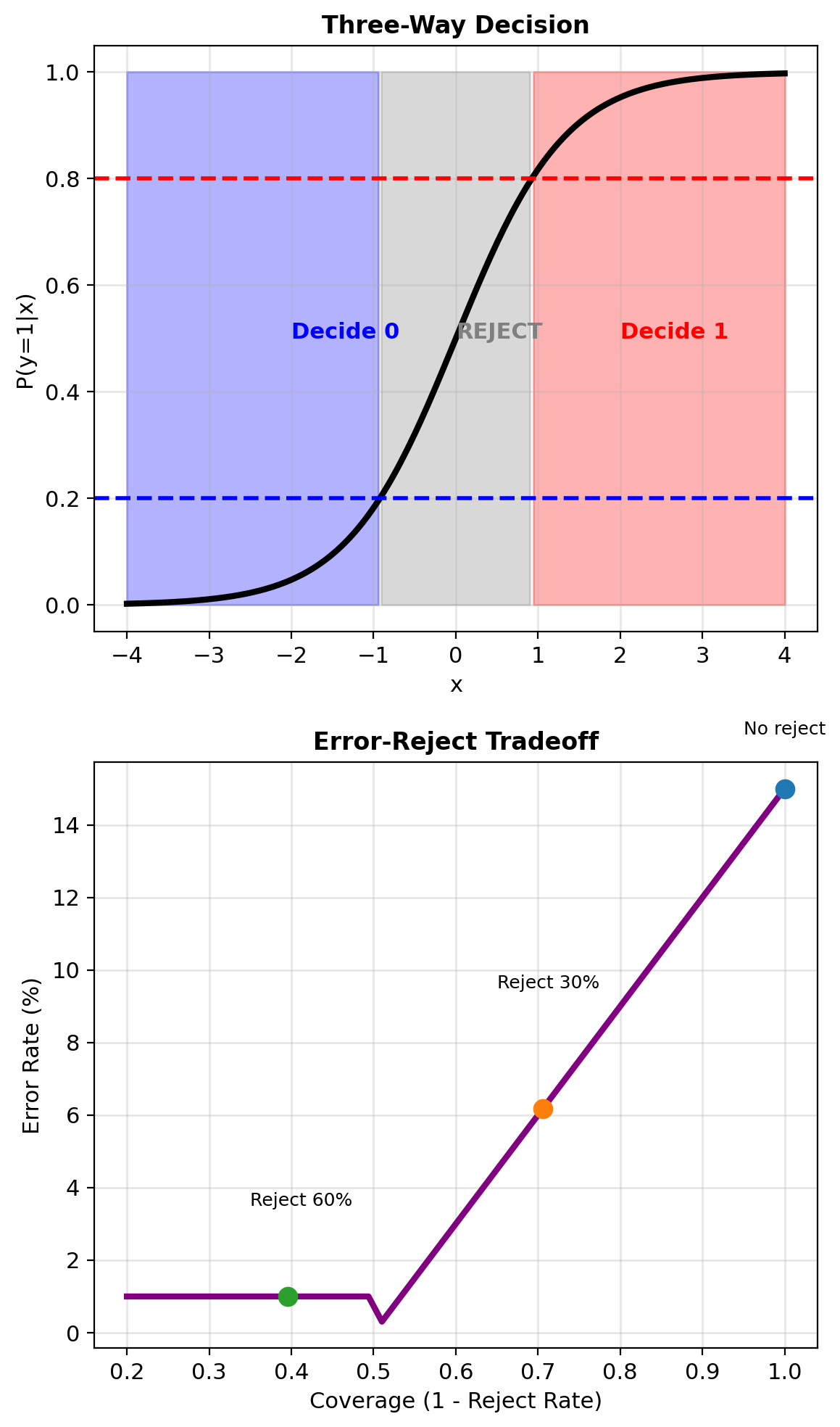

Rejecting – Deferring When Confidence Is Low

Three-way decision:

- Predict class 0

- Predict class 1

- Reject (defer to expert)

Extended loss matrix: \[L = \begin{bmatrix} 0 & c_{01} & c_r \\ c_{10} & 0 & c_r \end{bmatrix}\]

where \(c_r\) = cost of rejection (expert review)

Decision regions:

- Predict 0 if \(p < \tau_1\)

- Reject if \(\tau_1 \leq p \leq \tau_2\)

- Predict 1 if \(p > \tau_2\)

Optimal thresholds (for symmetric costs): \[\tau_1 = \frac{c_r}{c_{10}}, \quad \tau_2 = 1 - \frac{c_r}{c_{01}}\]

Reject when model confidence is low

Reject option reduces error on uncertain samples

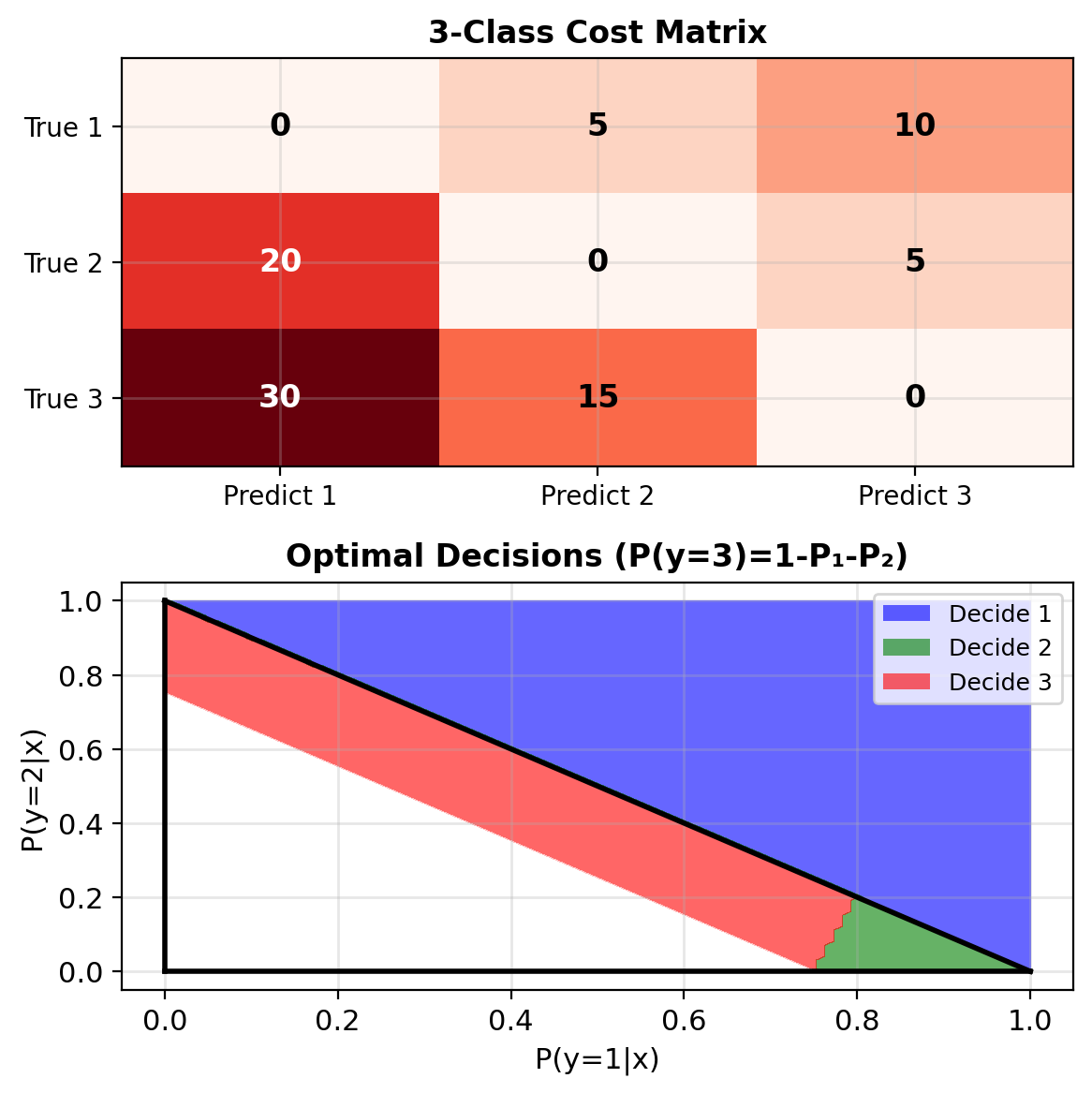

Extending Bayes Decisions to K Classes

K-class cost matrix: \(L \in \mathbb{R}^{K \times K}\)

\[L_{ij} = \text{cost of predicting } j \text{ when true is } i\]

Expected loss for action \(a\): \[R_a(\mathbf{x}) = \sum_{k=1}^K L_{ka} \cdot P(y=k|\mathbf{x})\]

Optimal decision: \[\hat{y}^* = \arg\min_a R_a(\mathbf{x})\]

Example: 3-class with varying costs \[L = \begin{bmatrix} 0 & 5 & 10 \\ 20 & 0 & 5 \\ 30 & 15 & 0 \end{bmatrix}\]

Must compute expected loss for each action

Special case: If \(L_{ij} = 1 - \delta_{ij}\) (0-1 loss), reduces to argmax of posteriors

Soft Decisions Preserve Uncertainty for Downstream Use

Hard decisions: \(\hat{y} \in \{0, 1, ..., K-1\}\)

- Single class prediction

- Required for final action

- Information loss through discretization

Soft decisions: \(\mathbf{p} = [p_0, p_1, ..., p_{K-1}]\)

- Full distribution of outcomes

- Preserves uncertainty information

- Useful for downstream processing

Soft decisions ideal for:

- Cascaded systems: Next stage uses probabilities

- Speech recognition → language model

- Object detection → tracking

- Confidence assessment: Reliability measures

- Medical diagnosis (refer if uncertain)

- Autonomous driving (hand off to human)

- Cost-sensitive decisions: Context-dependent losses

- Fraud detection (amount matters)

- Email filtering (sender importance)

- Ensemble methods: Combining multiple models

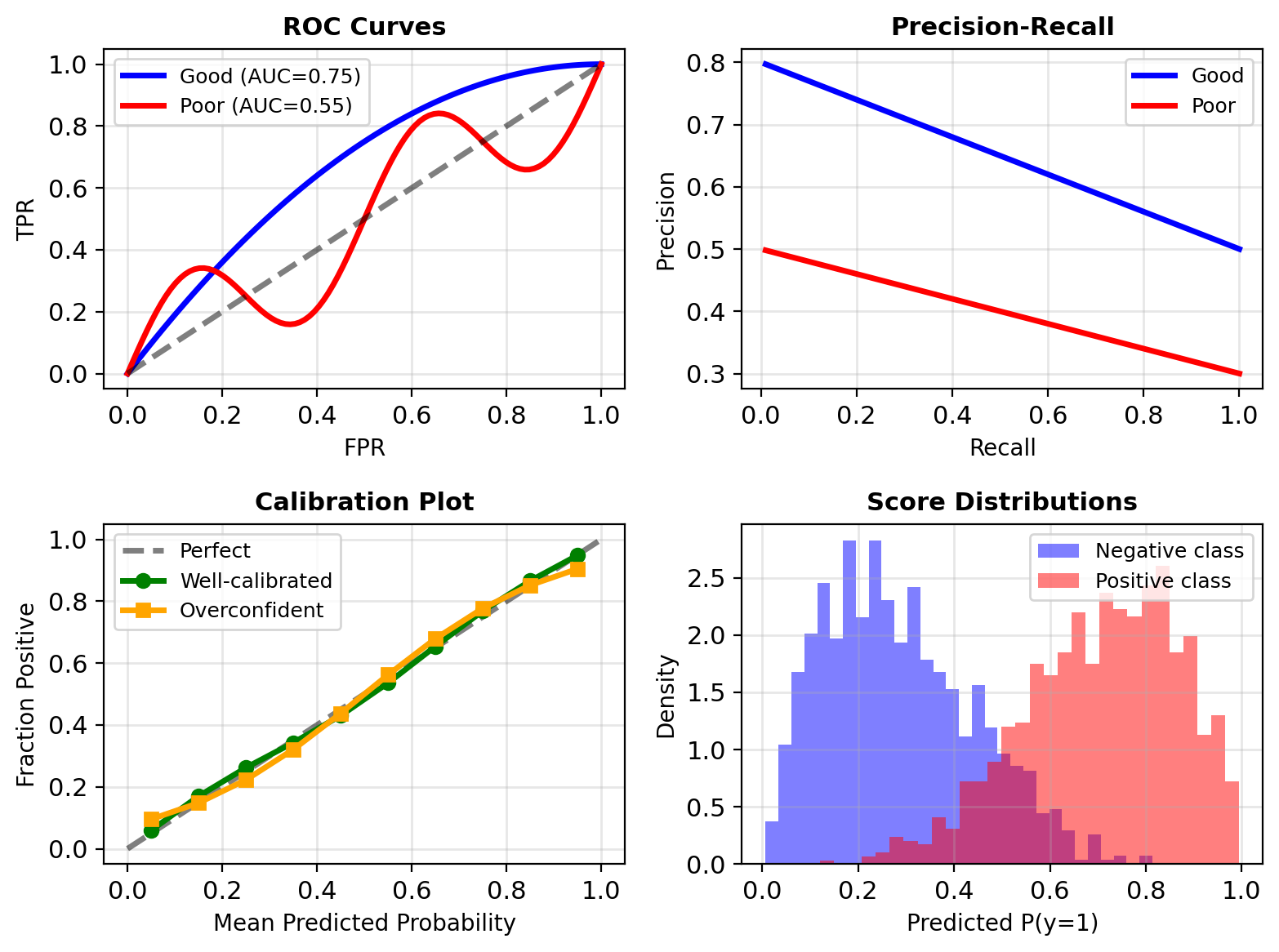

Beyond Accuracy – Evaluating Probabilistic Classifiers

1. Discrimination (ranking ability):

- ROC curve: TPR vs FPR

- AUC: Area under ROC

- Precision-Recall curve

2. Calibration (probability accuracy):

- Do predicted probabilities match frequencies?

- Among all \(\mathbf{x}\) where \(P(y=1|\mathbf{x}) = 0.7\), is the true fraction positive ≈ 70%?

3. Proper scoring rules:

- Log-loss: \(-\sum_i [y_i \log p_i + (1-y_i)\log(1-p_i)]\)

- Brier score: \(\sum_i (y_i - p_i)^2\)

These penalize both discrimination and calibration errors

Note: Good discrimination ≠ Good calibration

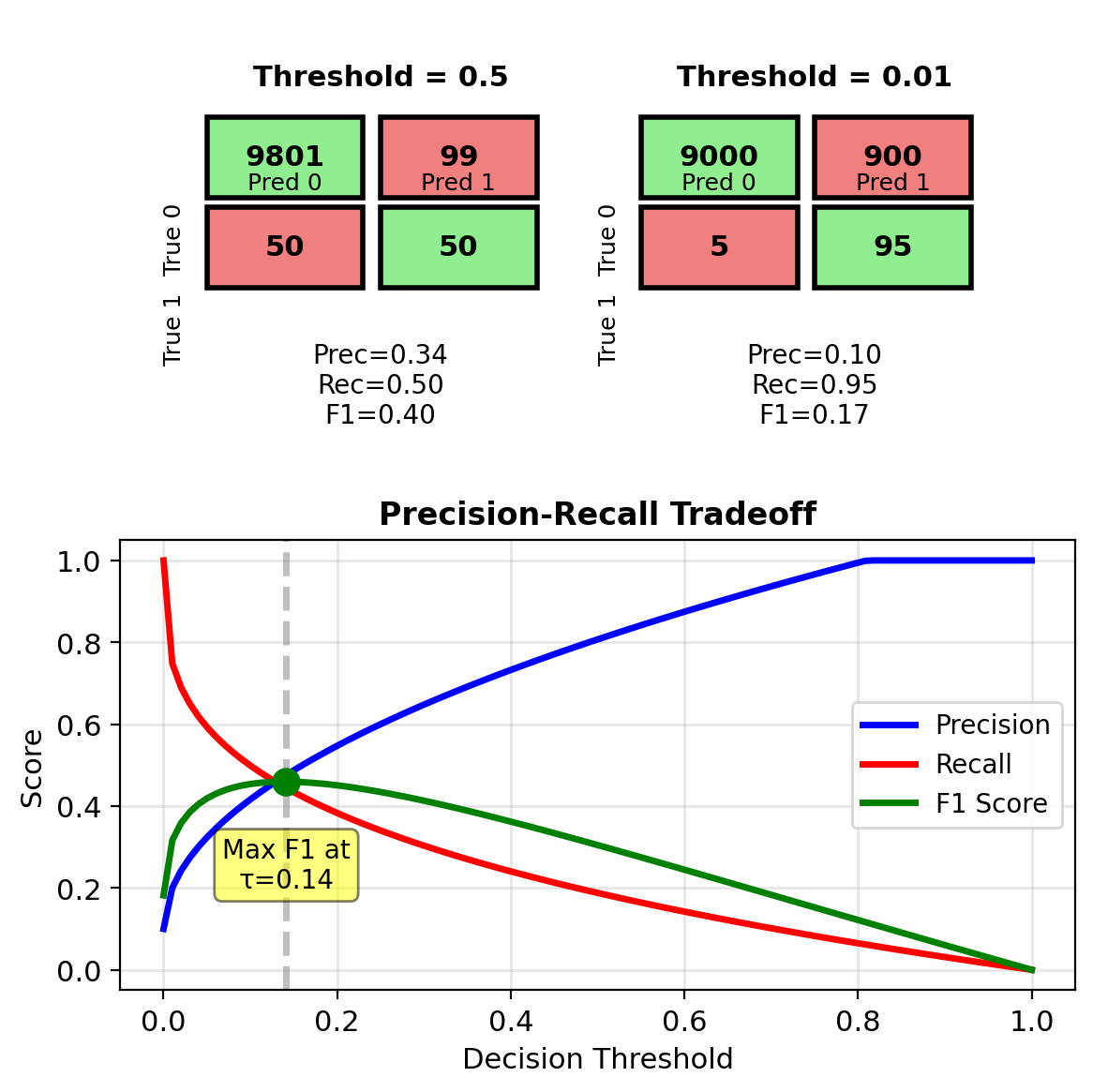

Class Imbalance Makes Accuracy Misleading

Imbalanced data: 99% negative, 1% positive

Problem with accuracy:

- Trivial classifier (always predict negative): 99% accurate

- Does not detect rare positive cases

Metrics for imbalanced data:

Precision: Of predicted positives, how many correct? \[\text{Precision} = \frac{\text{TP}}{\text{TP} + \text{FP}}\]

Recall (Sensitivity): Of true positives, how many found? \[\text{Recall} = \frac{\text{TP}}{\text{TP} + \text{FN}}\]

F1 Score: Harmonic mean \[F_1 = \frac{2 \cdot \text{Precision} \cdot \text{Recall}}{\text{Precision} + \text{Recall}}\]

Connection to costs: Optimize threshold based on \[\tau^* = \frac{c_{01} \cdot (1-\pi)}{c_{01}(1-\pi) + c_{10} \cdot \pi}\]

where \(\pi\) = class prior P(y=1)

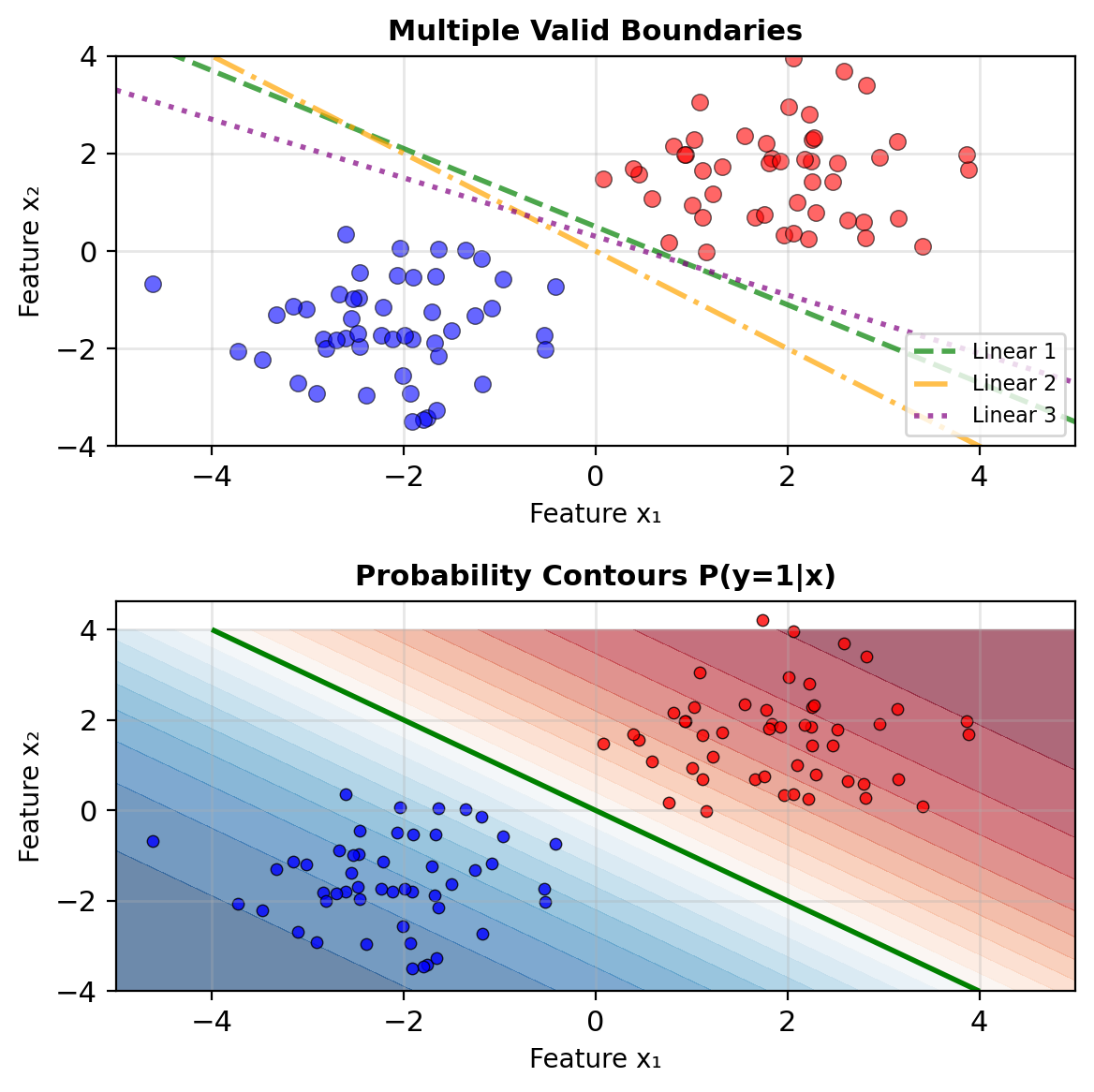

Why Linear Models Fail

Try modeling probability directly: \[p(\mathbf{x}) = \mathbf{w}^T\mathbf{x} + b\]

With \(w = 0.3\), \(b = 0.5\):

- \(p(x=-2) = -0.1\) (invalid)

- \(p(x=0) = 0.5\)

- \(p(x=2) = 1.1\) (invalid)

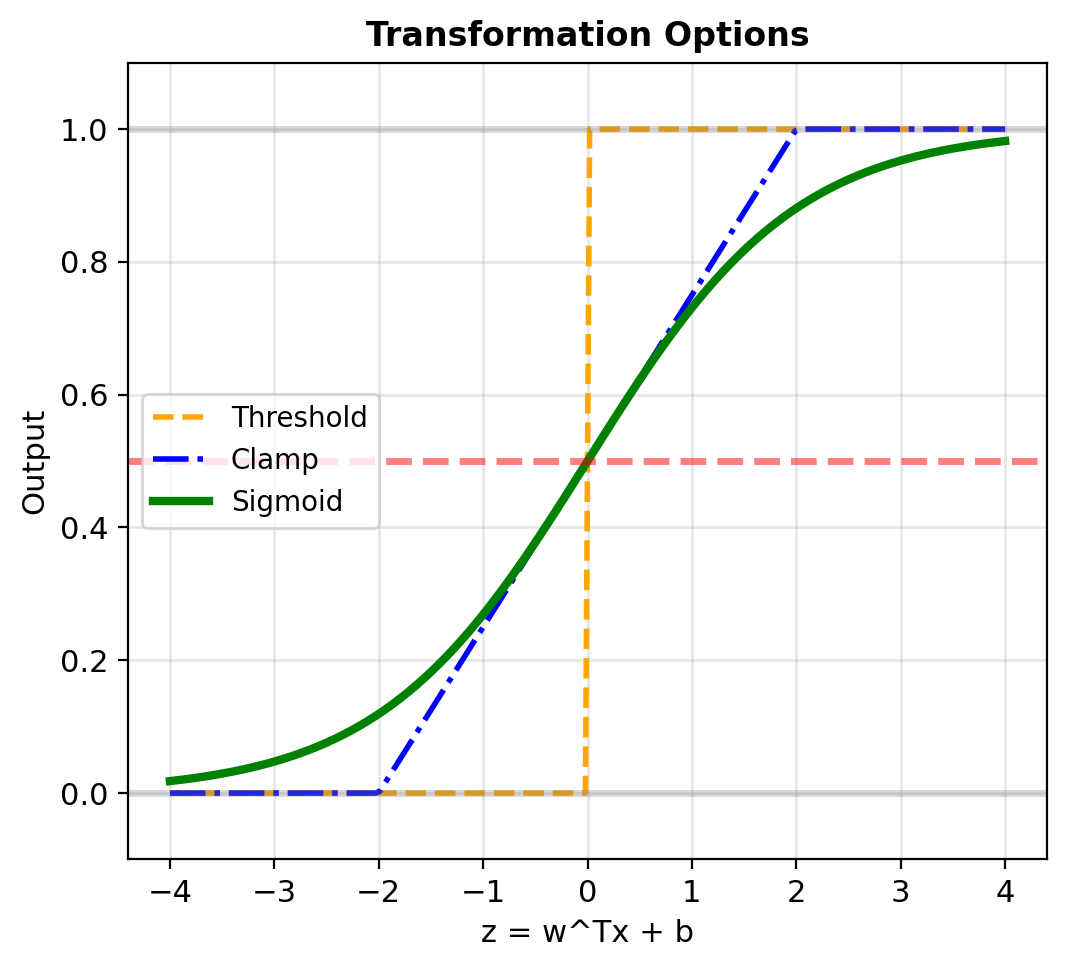

Problem: Linear outputs \(\in (-\infty, \infty)\) but probabilities need \(\in [0, 1]\)

Need transformation \(\mathbb{R} \to [0, 1]\) that:

- Outputs valid probabilities

- Preserves linear decision boundaries

- Is differentiable for optimization

Candidates:

- Threshold: \(p = \mathbb{1}[z > 0]\)

- Clamp: \(p = \max(0, \min(1, z))\) – Not differentiable

- Sigmoid: \(p = \frac{1}{1 + e^{-z}}\)

Log-Odds Map Probabilities to the Real Line

Odds: Alternative to probability

\[\text{Odds}(A) = \frac{P(A)}{P(A^C)}\]

For binary outcome

\[\text{Odds} = \frac{p}{1-p} = \frac{P(y=1)}{P(y=0)}\]

Examples:

- \(p = 0.5\): Odds = 1 (1:1, “even odds”)

- \(p = 0.75\): Odds = 3 (3:1 in favor)

- \(p = 0.25\): Odds = 1/3 (1:3 against)

Range: \([0, \infty)\)

Log-odds (logit): \[\text{logit}(p) = \log\left(\frac{p}{1-p}\right)\]

Range: \((-\infty, \infty)\)

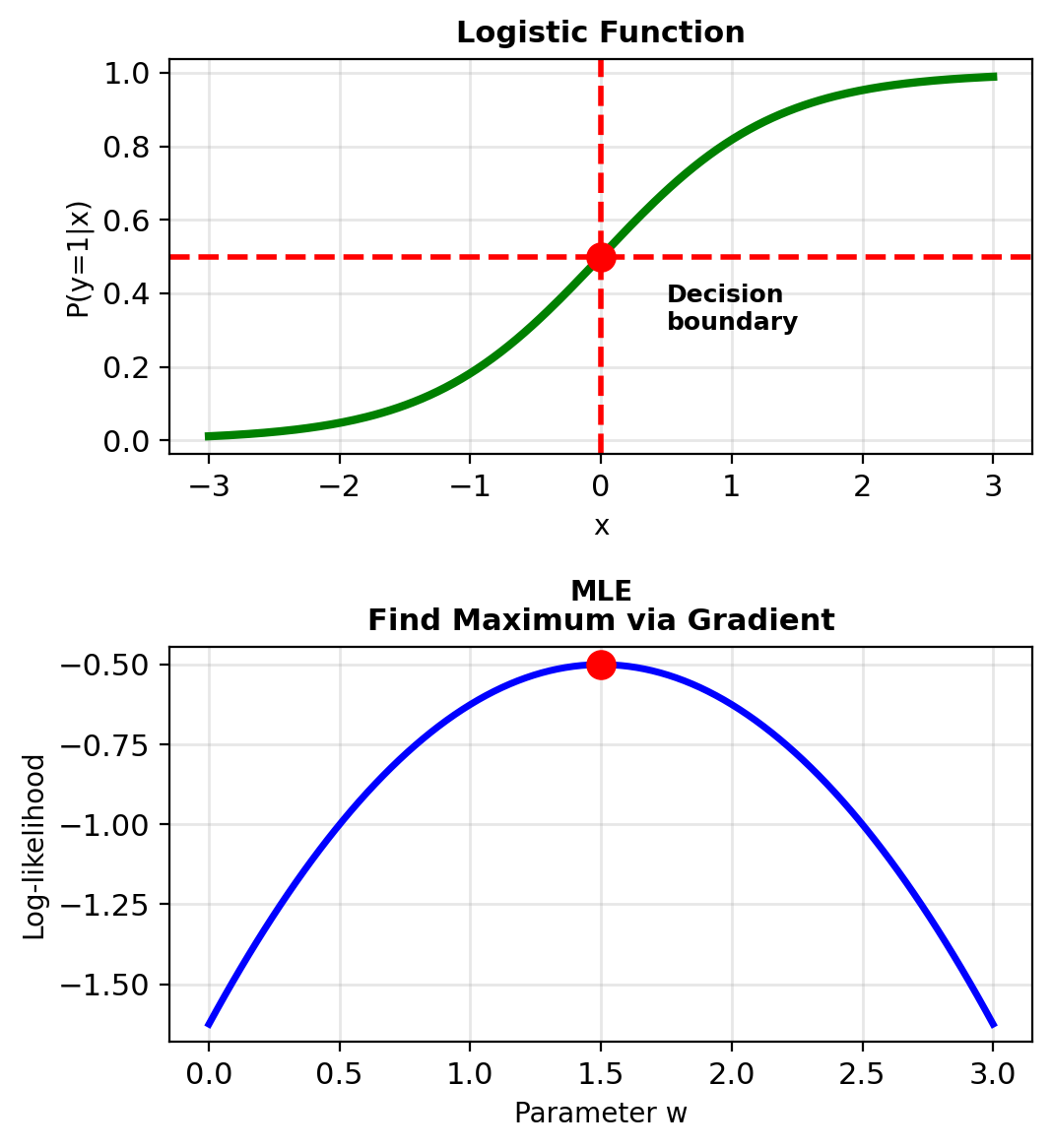

The Logistic Model

Model log-odds linearly: \[\log\left(\frac{p(\mathbf{x})}{1-p(\mathbf{x})}\right) = \mathbf{w}^T\mathbf{x} + b\]

Solving for \(p(\mathbf{x})\):

Let \(z = \mathbf{w}^T\mathbf{x} + b\)

\[\frac{p}{1-p} = e^z\]

\[p = (1-p)e^z\]

\[p = e^z - pe^z\]

\[p(1 + e^z) = e^z\]

\[p = \frac{e^z}{1 + e^z} = \frac{1}{1 + e^{-z}}\]

Gives the logistic (sigmoid) function

\[\boxed{p(\mathbf{x}) = \sigma(\mathbf{w}^T\mathbf{x} + b) = \frac{1}{1 + e^{-(\mathbf{w}^T\mathbf{x} + b)}}}\]

The Sigmoid Unit

Inputs: \(\mathbf{x} = [x_1, x_2, \ldots, x_d]^T\)

Weights: \(\mathbf{w} = [w_1, w_2, \ldots, w_d]^T\)

Bias: \(b\)

Linear combination: \[z = \mathbf{w}^T\mathbf{x} + b = \sum_{j=1}^d w_j x_j + b\]

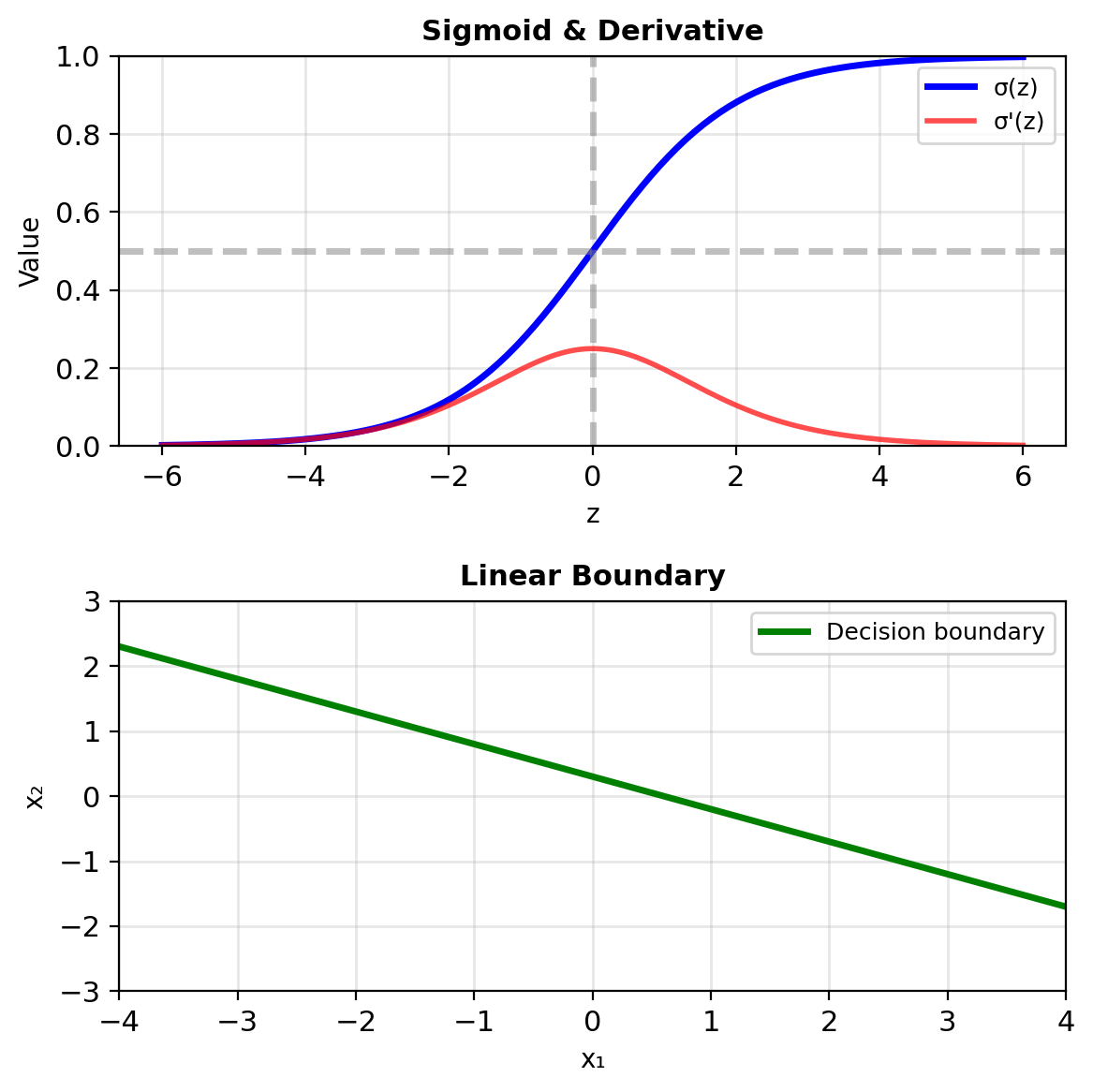

Activation function: \[p = \sigma(z) = \frac{1}{1 + e^{-z}}\]

Output: \(p = P[\text{class 1}] \in (0, 1)\)

Decision rule: Predict class 1 if \(p > 0.5\)

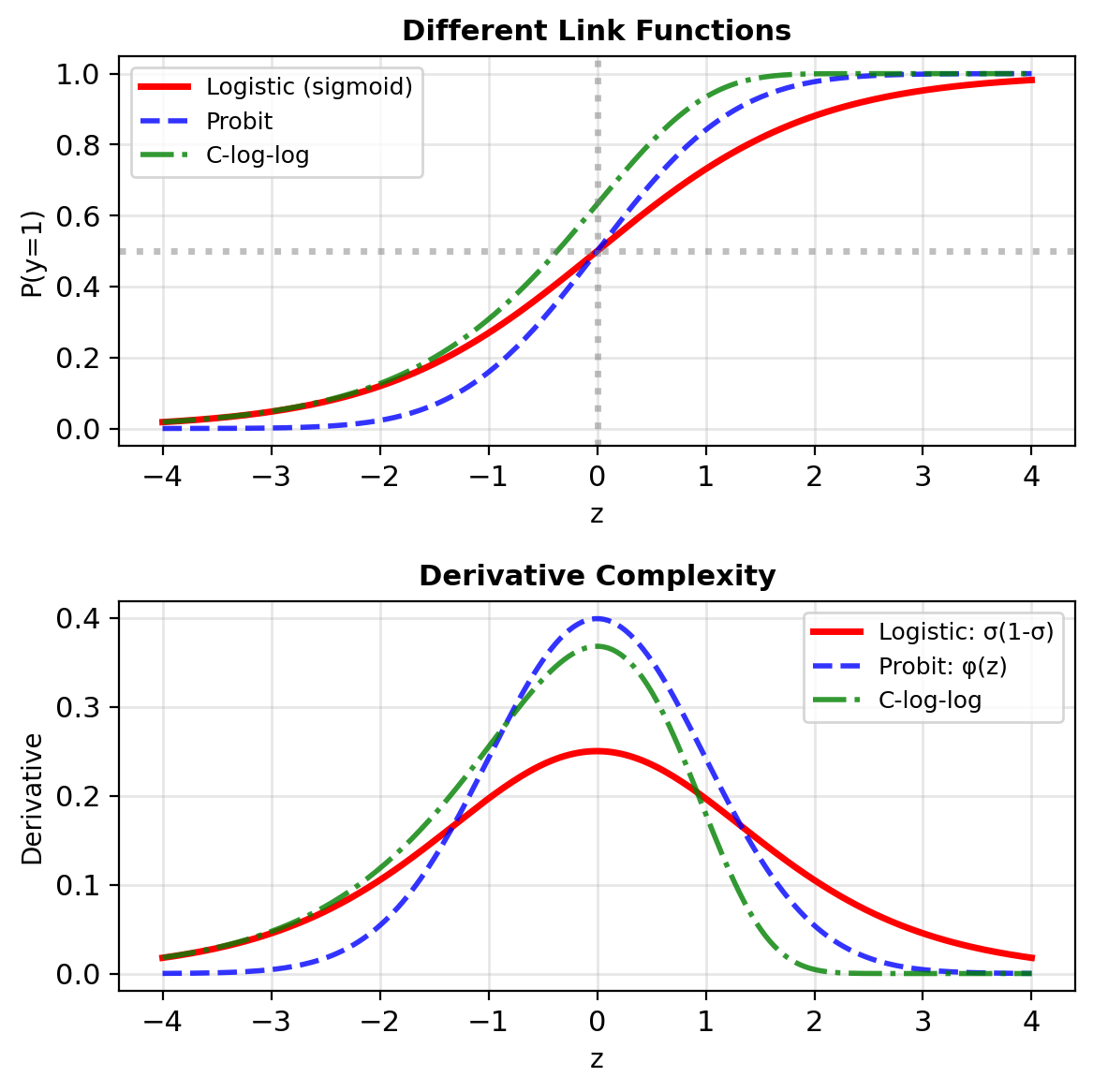

Why Log-Odds (Not Other Transformations)?

Other candidates that map \(\mathbb{R} \to [0,1]\):

Probit (cumulative normal): \[p = \Phi(z) = \int_{-\infty}^z \frac{1}{\sqrt{2\pi}}e^{-t^2/2}dt\]

- No closed form

- Derivative involves normal PDF

- Used in econometrics

Complementary log-log: \[p = 1 - e^{-e^z}\]

- Asymmetric

- Good for rare events

- Different tail behavior

Logistic function advantages:

- Natural interpretation: Log-odds are intuitive

- Simple derivative: \(\sigma'(z) = \sigma(z)(1-\sigma(z))\)

- Computational efficiency: Closed form everything

- Information theory: Maximizes entropy given constraints

Sigmoid – Valid Probabilities, Linear Boundaries, Interpretable Weights

The sigmoid function \(\sigma(z) = \frac{1}{1 + e^{-z}}\):

Valid probabilities: \(\sigma(z) \in (0, 1)\) always

Smooth and differentiable: \[\sigma'(z) = \sigma(z)(1 - \sigma(z))\]

Linear decision boundary:

- Predict 1 if \(p > 0.5\)

- This occurs when \(\mathbf{w}^T\mathbf{x} + b > 0\)

- Boundary: \(\mathbf{w}^T\mathbf{x} + b = 0\) (hyperplane)

Interpretable coefficients:

- \(w_j\) = change in log-odds per unit \(x_j\)

- \(e^{w_j}\) = odds multiplication factor

When the Log-Odds Linearity Assumption Breaks

Logistic regression assumes: \[\log\frac{P(y=1|\mathbf{x})}{P(y=0|\mathbf{x})} = \mathbf{w}^T\mathbf{x} + b\]

Nonlinear boundaries: Concentric classes, XOR — no linear \(f(\mathbf{x})\) works

- Best linear classifier on XOR: 50% accuracy

- More data doesn’t help — the model class is wrong

Outlier sensitivity: One extreme point pulls \(\|\mathbf{w}\| \to \infty\)

- MLE maximizes confidence on every sample

- No mechanism to downweight outliers

High dimensions (\(d > n\)): Perfect separation \(\Rightarrow\) \(\hat{\mathbf{w}}_{\text{MLE}}\) diverges

- 100 features, 80 samples: \(\|\mathbf{w}\|\) grows without bound

- Regularization (Section 5) fixes this

Misspecification: MLE finds best sigmoid approximation in KL divergence \[\hat{\mathbf{w}} = \arg\min_{\mathbf{w}} D_{\text{KL}}(p_{\text{true}} \| p_{\sigma}(\cdot; \mathbf{w}))\]

Finding \(\mathbf{w}\) and \(b\) That Fit the Data

Model: \(P(y=1|\mathbf{x}) = \sigma(\mathbf{w}^T\mathbf{x} + b)\)

Training data: \(\{(\mathbf{x}_i, y_i)\}_{i=1}^n\)

Objective: Find \(\mathbf{w}, b\) that make observed labels most probable

\[\hat{\mathbf{w}} = \arg\max_{\mathbf{w}} \prod_{i=1}^n p_i^{y_i}(1-p_i)^{1-y_i}\]

Equivalent to minimizing cross-entropy: \[\mathcal{L} = -\sum_{i=1}^n [y_i \log p_i + (1-y_i)\log(1-p_i)]\]

Gradient: \(\nabla_\mathbf{w} \ell = \sum_{i=1}^n (y_i - p_i)\mathbf{x}_i\)

Errors weighted by features — intuitive and cheap to compute

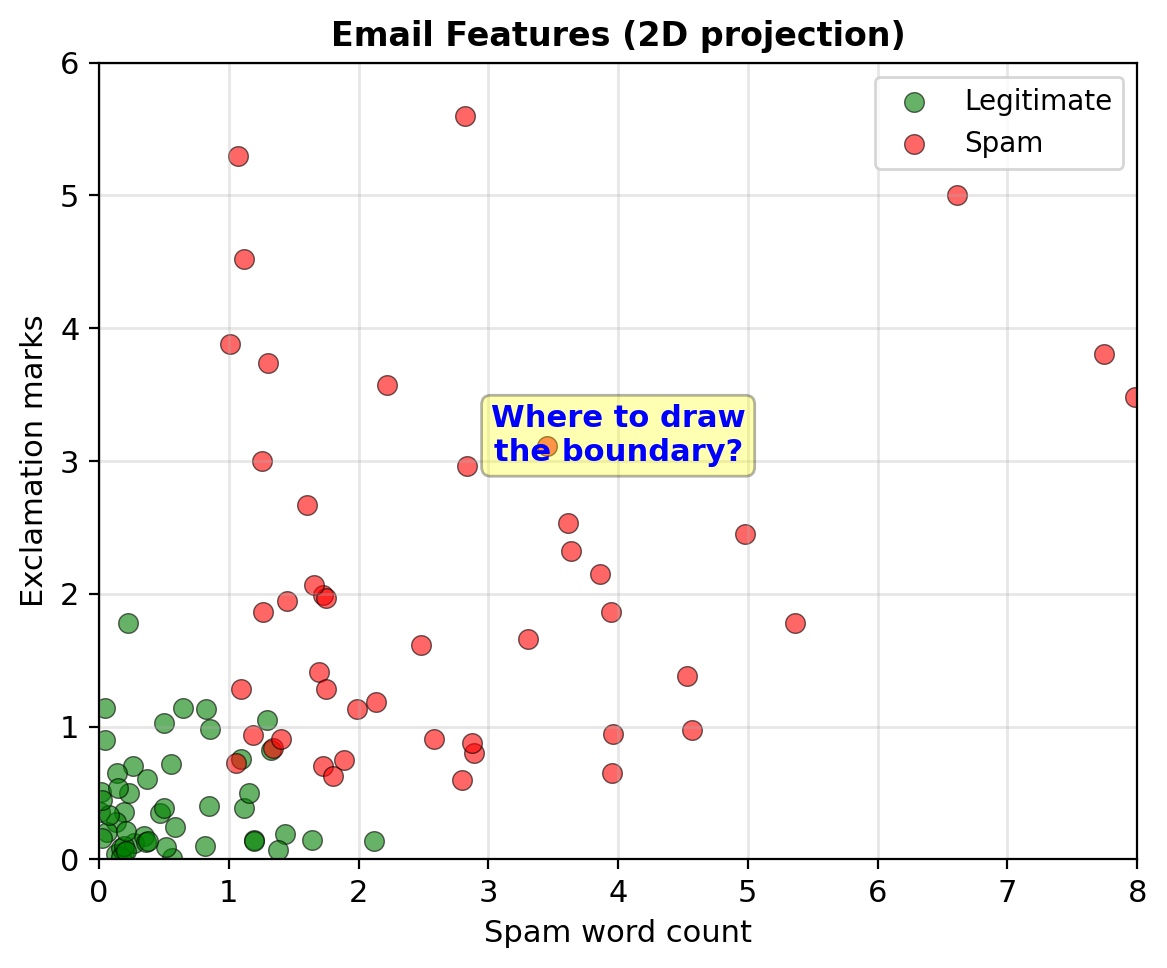

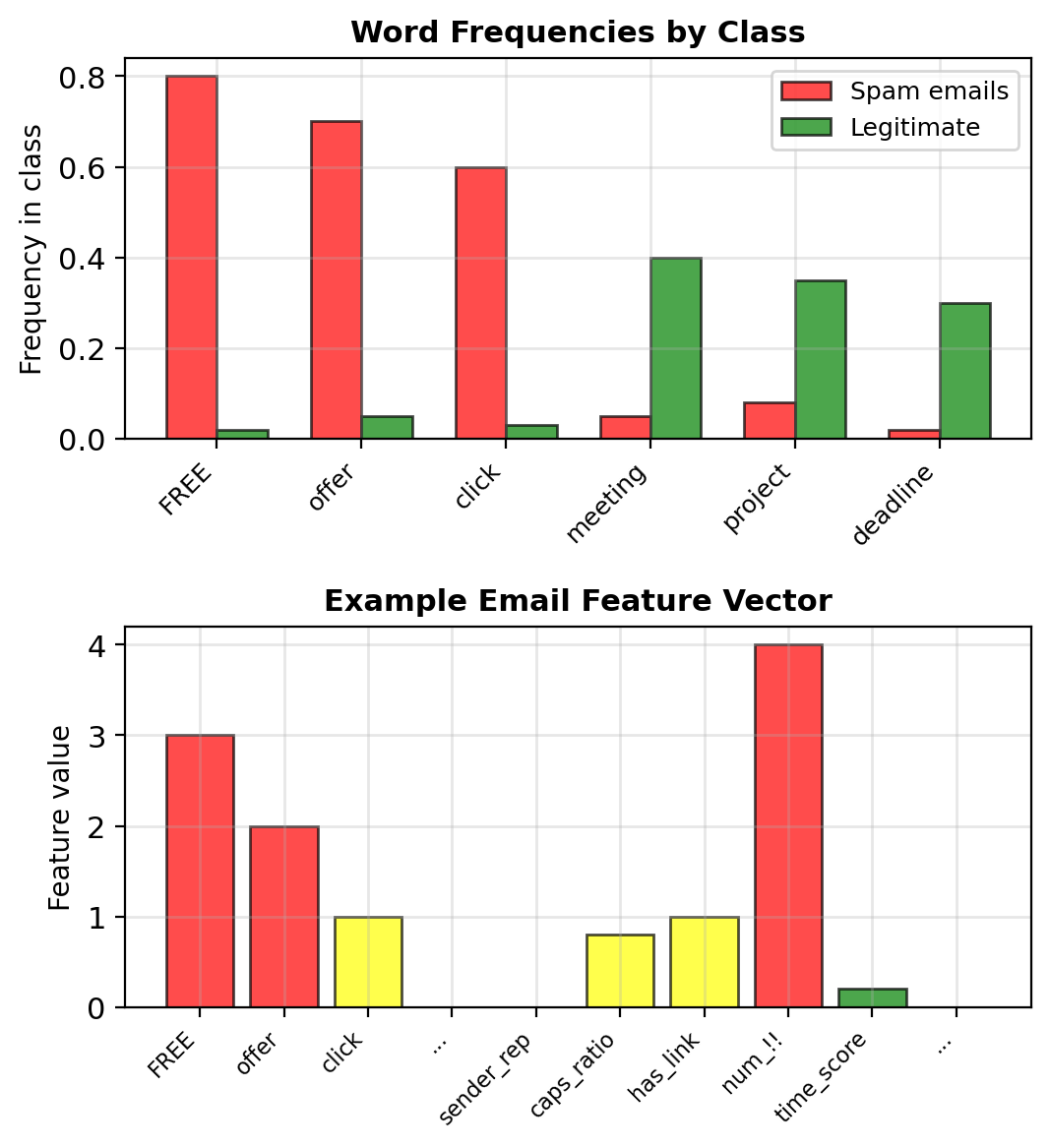

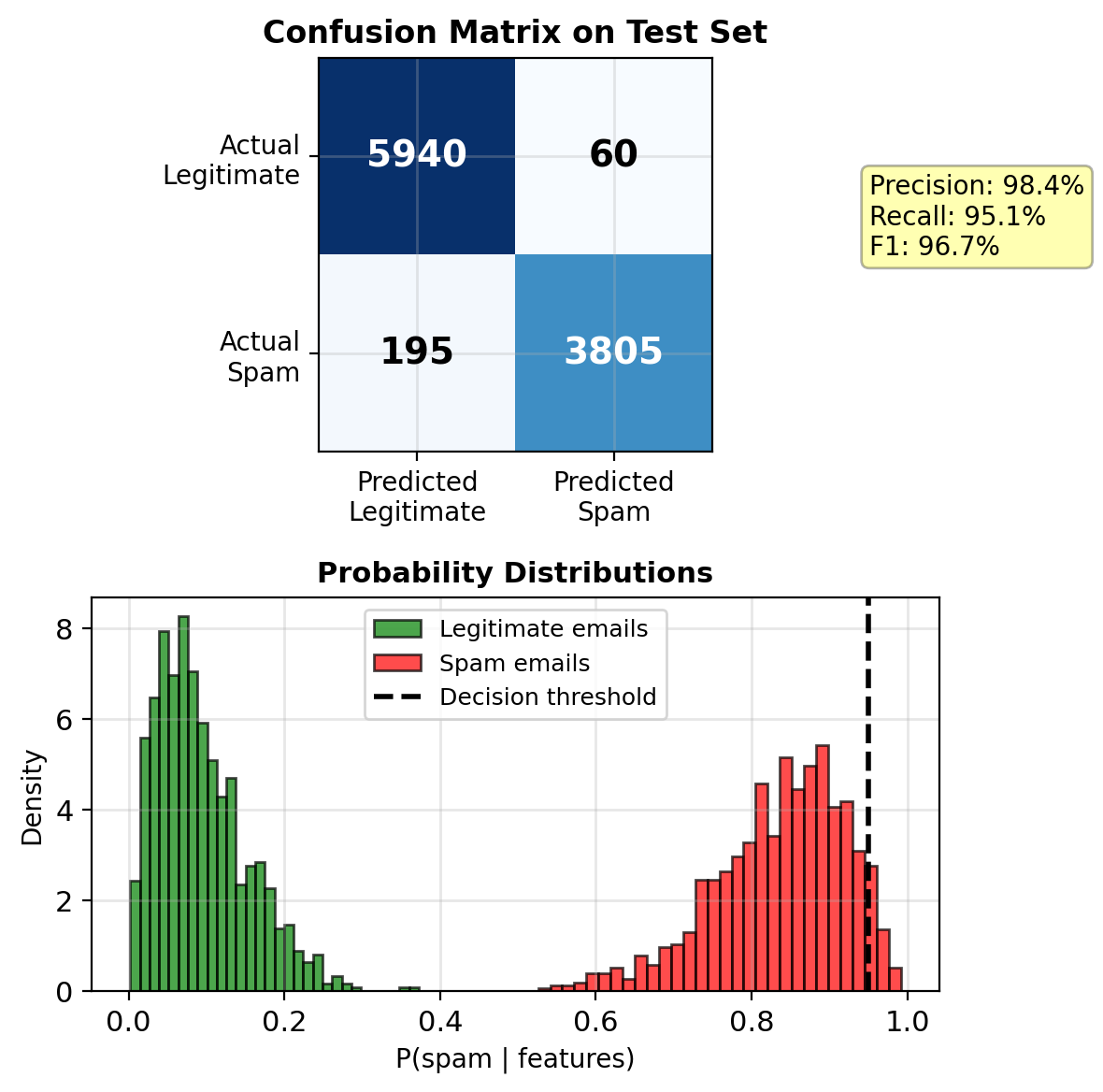

Example: Spam Detection

Problem: Classify emails as spam or legitimate

Features extracted from email:

- Word frequencies: “FREE”, “CLICK”, “offer”

- Sender reputation score

- Number of ALL CAPS words

- Exclamation marks count

- Links to external domains

- Time of day sent

Example vector \(\mathbf{x} \in \mathbb{R}^6\):

Email: "FREE OFFER! Click HERE!!!"

x = [2, 0.1, 2, 3, 1, 0.3]

↑ ↑ ↑ ↑ ↑ ↑

FREE low 2 3 1 3am

offer rep CAPS !! linkIn practice, \(d\) = 100–10,000 features (bag-of-words counts, TF-IDF weights, metadata)

Goal: Learn \(P(\text{spam}|\mathbf{x})\)

Spam filters use 1000s of features

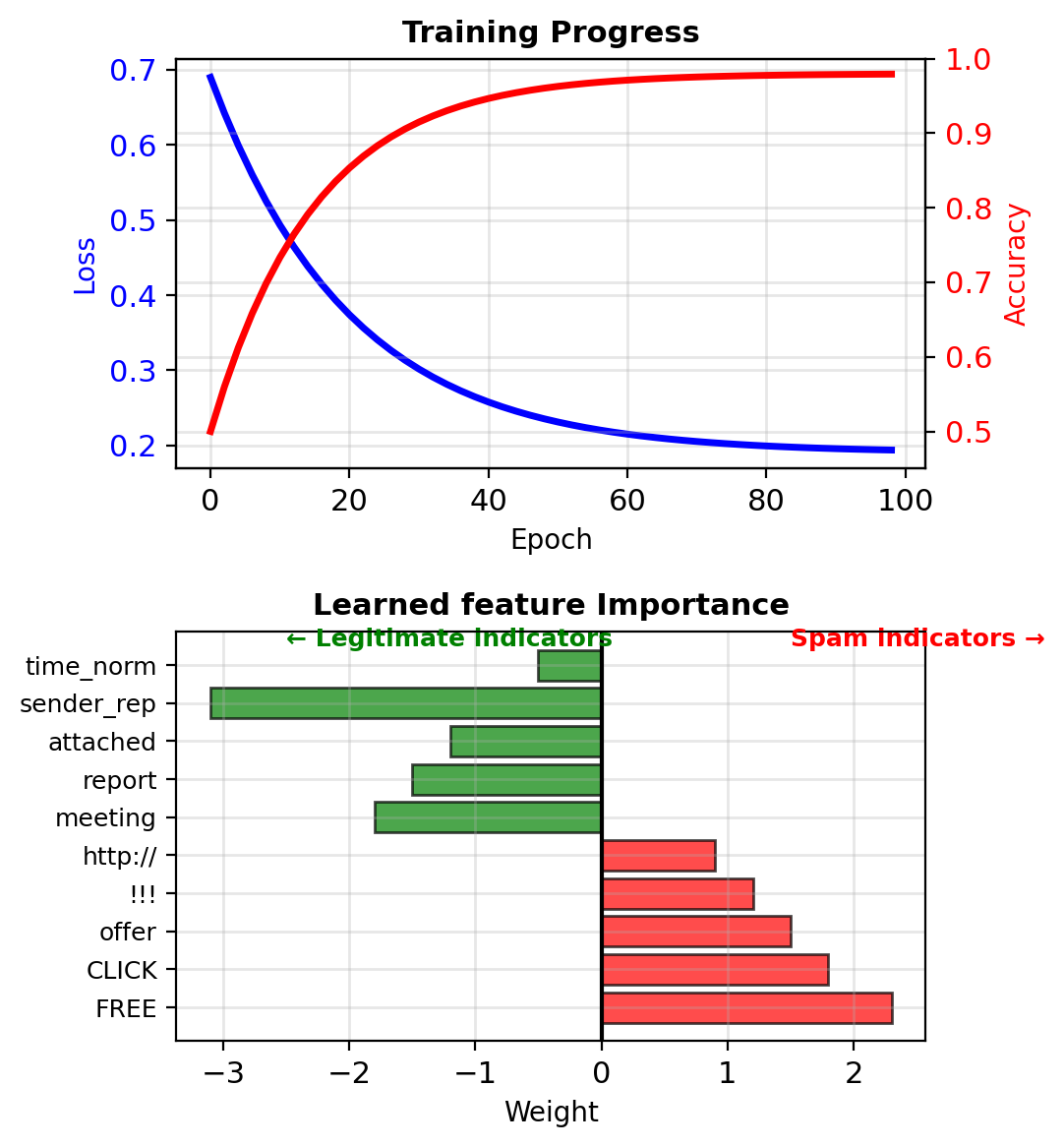

Training Logistic Regression

Model: \[P(\text{spam}|\mathbf{x}) = \sigma(\mathbf{w}^T\mathbf{x} + b)\]

Training (gradient ascent on log-likelihood):

# Initialize

w = np.random.randn(100) * 0.01

b = 0

for epoch in range(100):

# Compute predictions

z = X @ w + b

p = sigmoid(z)

# Gradient step

grad_w = X.T @ (y - p) / n

grad_b = np.mean(y - p)

w += learning_rate * grad_w

b += learning_rate * grad_bLearned weights reveal spam indicators:

- \(w_{\text{FREE}} = 2.3\) (strong spam signal)

- \(w_{\text{meeting}} = -1.8\) (legitimate signal)

- \(w_{\text{sender_rep}} = -3.1\) (reputation matters)

Target: >95% detection, <0.1% false positive, <10ms latency

Calibrated Probabilities Enable Threshold Tuning

Inference for new email:

def classify_email(email_text, w, b):

# Extract features

x = extract_features(email_text)

# Compute probability

z = np.dot(w, x) + b

p_spam = sigmoid(z)

# Decision with threshold

if p_spam > 0.95: # High threshold

return "spam", p_spam

else:

return "legitimate", p_spamExample performance:

- Accuracy: 97.2%

- Spam recall: 95.1%

- False positive rate: 0.08%

- Inference time: 0.3ms per email

Advantages:

- Interpretable: see why email flagged

- Fast: millions of emails per second

- Updatable: online learning for new spam

Threshold tuning possible since calibrated probabilities

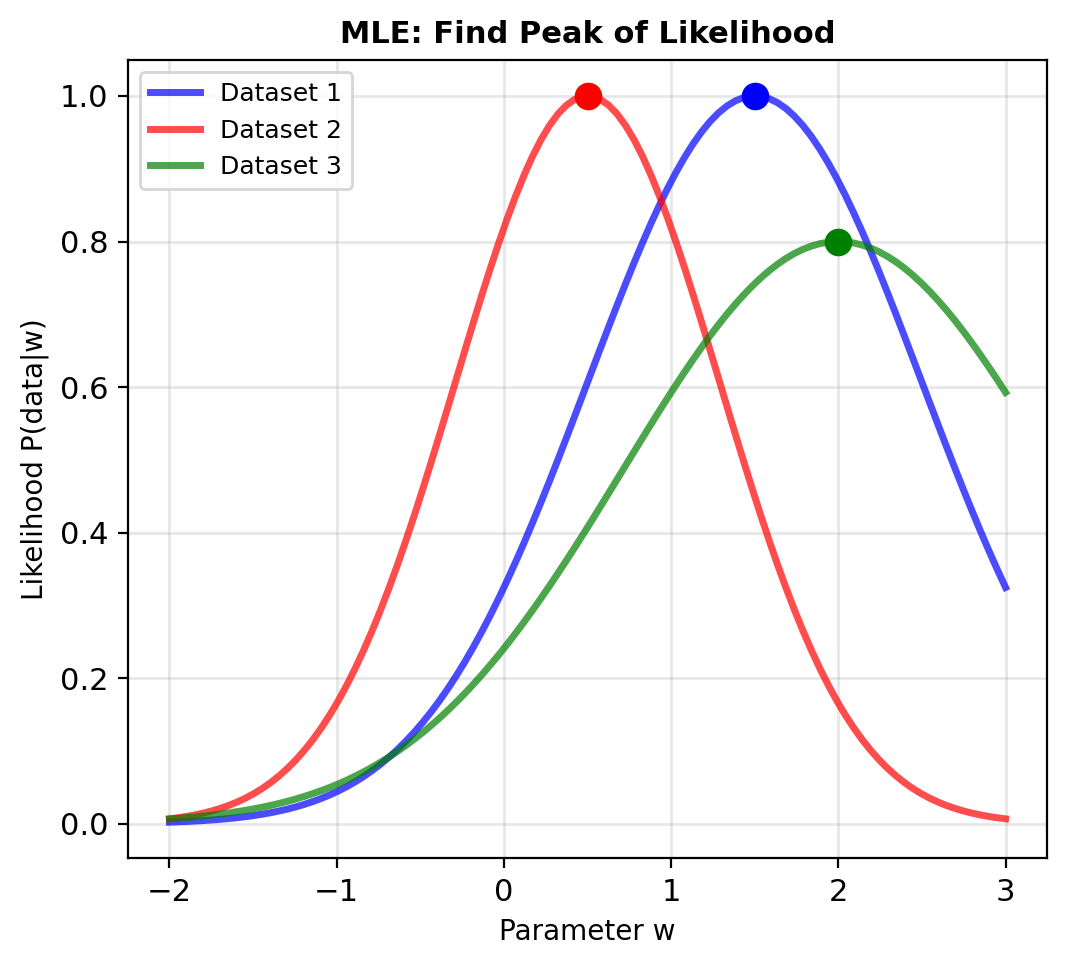

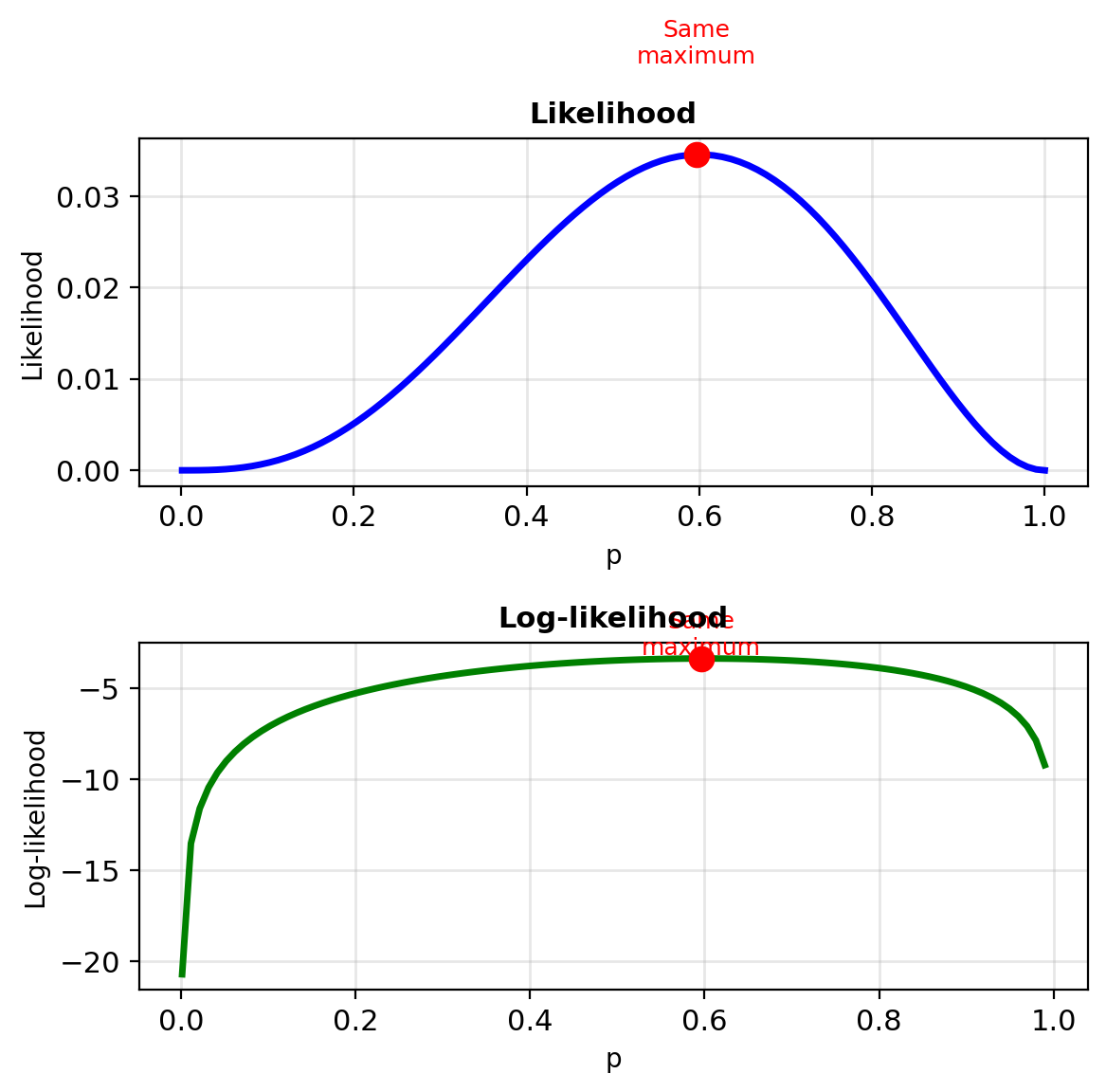

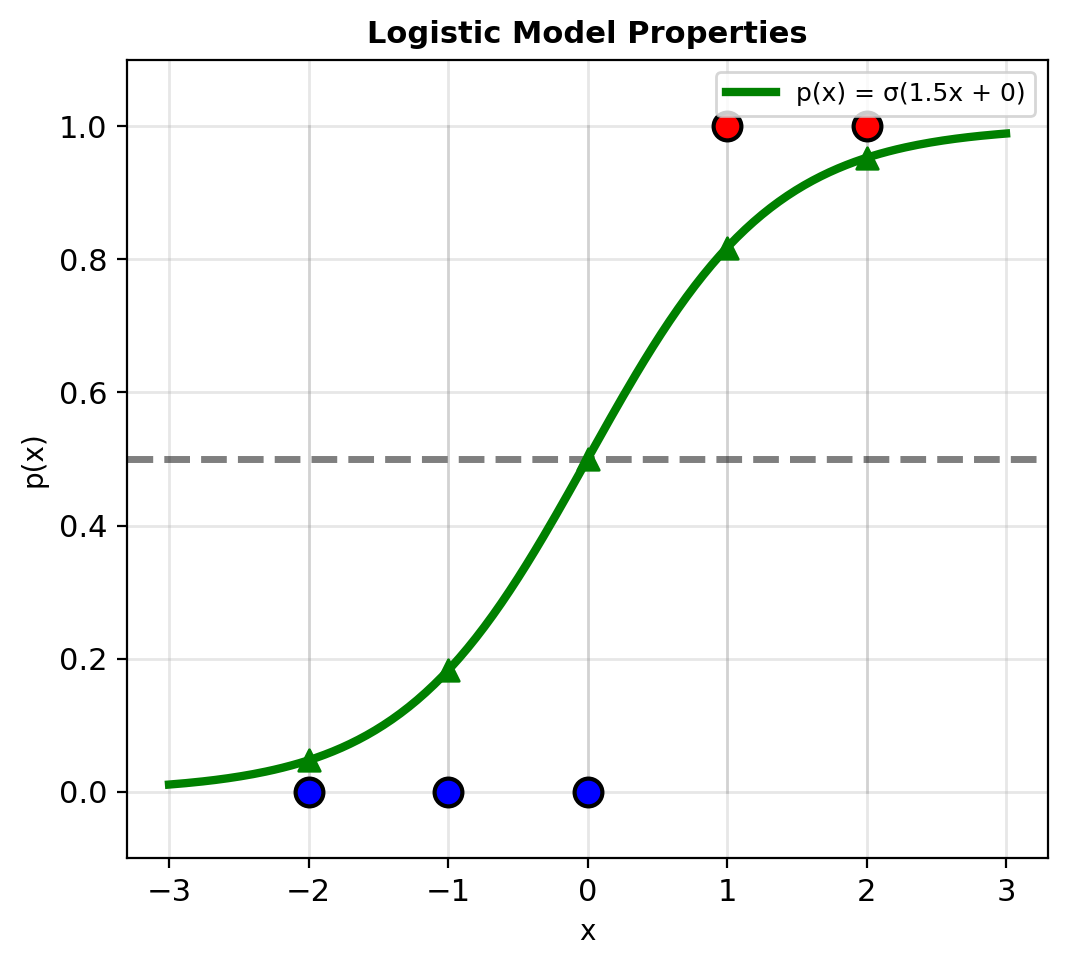

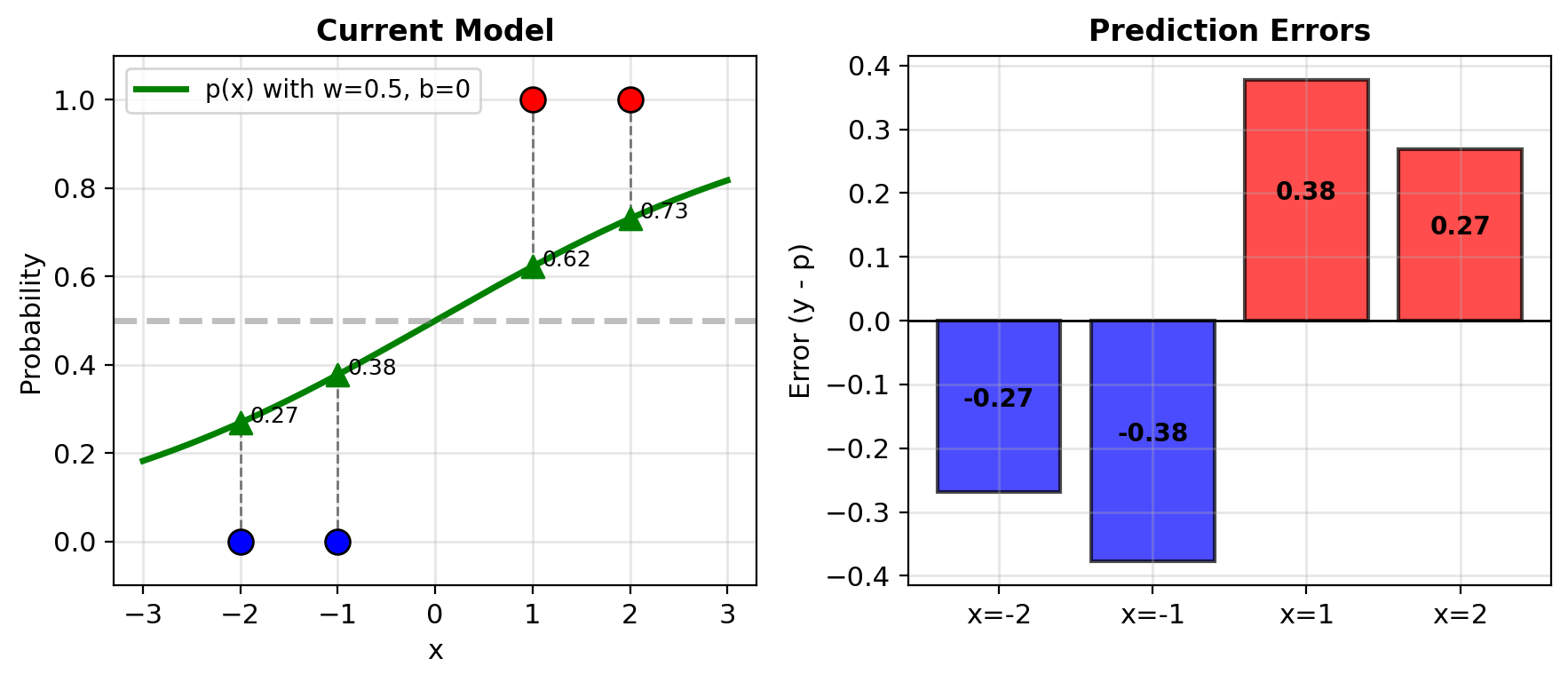

Example: MLE with 4 Points – Compute the Likelihood

Dataset: 4 points in 1D

X = [-2, -1, 1, 2]

y = [0, 0, 1, 1]Current Model: \(p(x) = \sigma(wx + b)\)

with \(w = 0.5\), \(b = 0\)

Compute predictions:

- \(z_1 = 0.5(-2) + 0 = -1\), \(p_1 = \sigma(-1) = 0.27\)

- \(z_2 = 0.5(-1) + 0 = -0.5\), \(p_2 = \sigma(-0.5) = 0.38\)

- \(z_3 = 0.5(1) + 0 = 0.5\), \(p_3 = \sigma(0.5) = 0.62\)

- \(z_4 = 0.5(2) + 0 = 1\), \(p_4 = \sigma(1) = 0.73\)

Errors \(y - p\):

- Point 1: \(0 - 0.27 = -0.27\)

- Point 2: \(0 - 0.38 = -0.38\)

- Point 3: \(1 - 0.62 = +0.38\)

- Point 4: \(1 - 0.73 = +0.27\)

Log-Likelihood for the 4-Point Example

Log-likelihood: \[\ell = \sum_{i=1}^4 [y_i \log p_i + (1-y_i)\log(1-p_i)]\]

So:

- \(i=1\): \(0 \cdot \log(0.27) + 1 \cdot \log(0.73) = -0.31\)

- \(i=2\): \(0 \cdot \log(0.38) + 1 \cdot \log(0.62) = -0.48\)

- \(i=3\): \(1 \cdot \log(0.62) + 0 \cdot \log(0.38) = -0.48\)

- \(i=4\): \(1 \cdot \log(0.73) + 0 \cdot \log(0.27) = -0.31\)

Total: \(\ell = -1.58\)

Negative log-likelihood: \(\text{NLL} = 1.58\)

Minimize this loss function

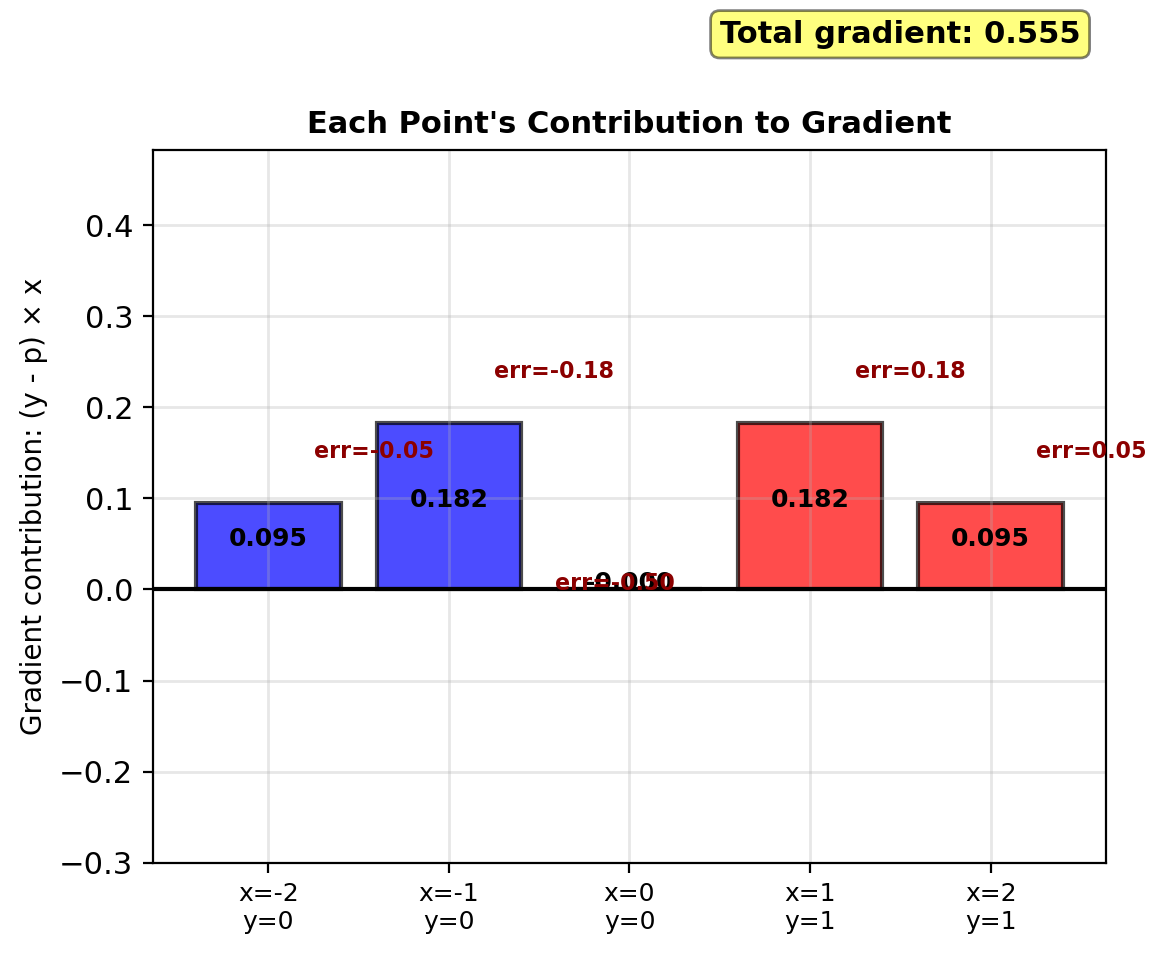

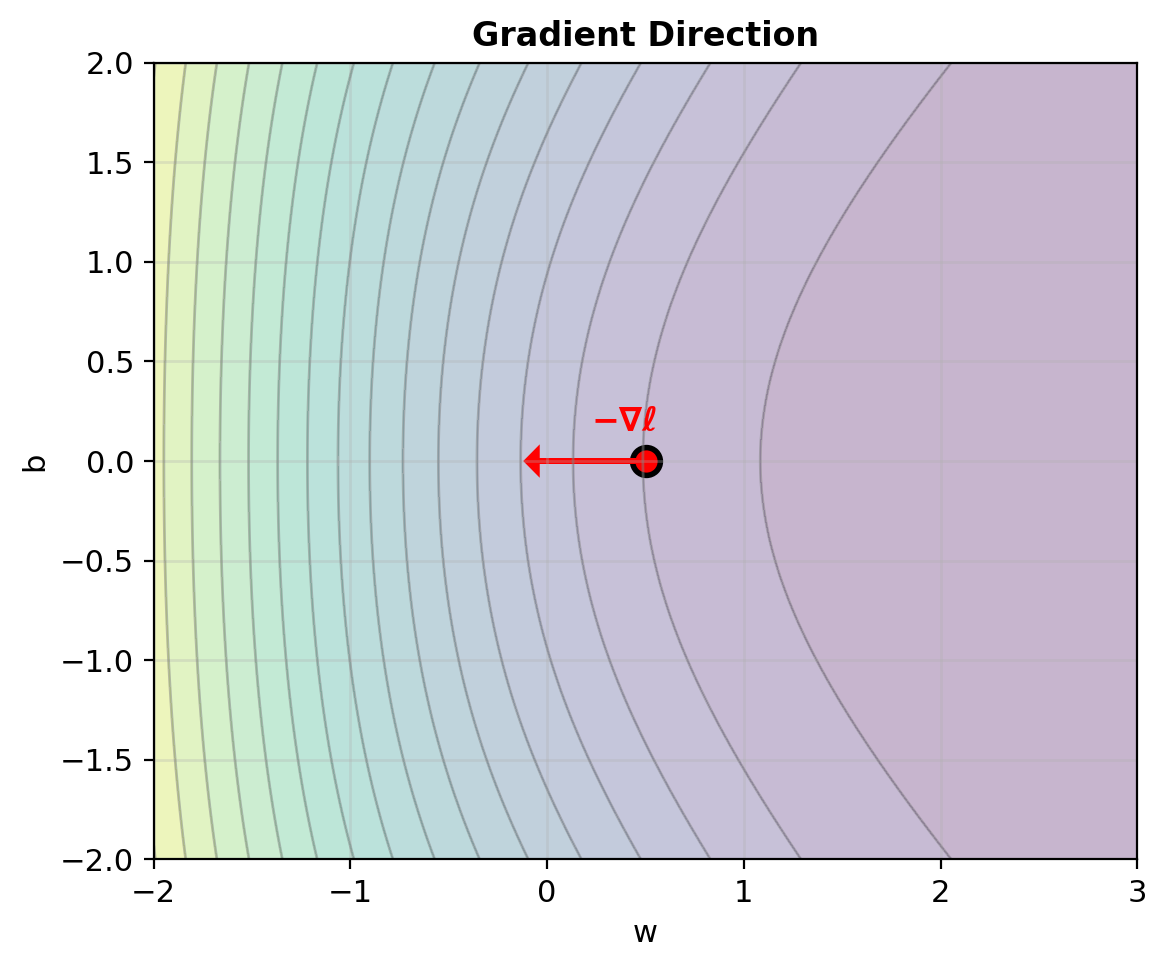

Gradient – Errors Weighted by Features

Gradient formulas (from earlier): \[\frac{\partial \ell}{\partial w} = \sum_{i=1}^n (y_i - p_i)x_i\] \[\frac{\partial \ell}{\partial b} = \sum_{i=1}^n (y_i - p_i)\]

For our example:

\(\frac{\partial \ell}{\partial w}\): \[\begin{align} &= (-0.27)(-2) + (-0.38)(-1)\\ &\quad + (0.38)(1) + (0.27)(2)\\ &= 0.54 + 0.38 + 0.38 + 0.54\\ &= 1.84 \end{align}\]

\(\frac{\partial \ell}{\partial b}\): \[= -0.27 - 0.38 + 0.38 + 0.27 = 0\]

Computing contributions:

| \(i\) | \(x_i\) | \(y_i\) | \(p_i\) | \((y_i - p_i)x_i\) |

|---|---|---|---|---|

| 1 | -2 | 0 | 0.27 | 0.54 |

| 2 | -1 | 0 | 0.38 | 0.38 |

| 3 | 1 | 1 | 0.62 | 0.38 |

| 4 | 2 | 1 | 0.73 | 0.54 |

Sum: \(\nabla_w \ell = 1.84\)

Gradient w.r.t. \(w\) positive: increase \(w\)

Gradient w.r.t. \(b\) zero: \(b\) locally optimal

Larger errors \(|y_i - p_i|\) contribute more to gradient.

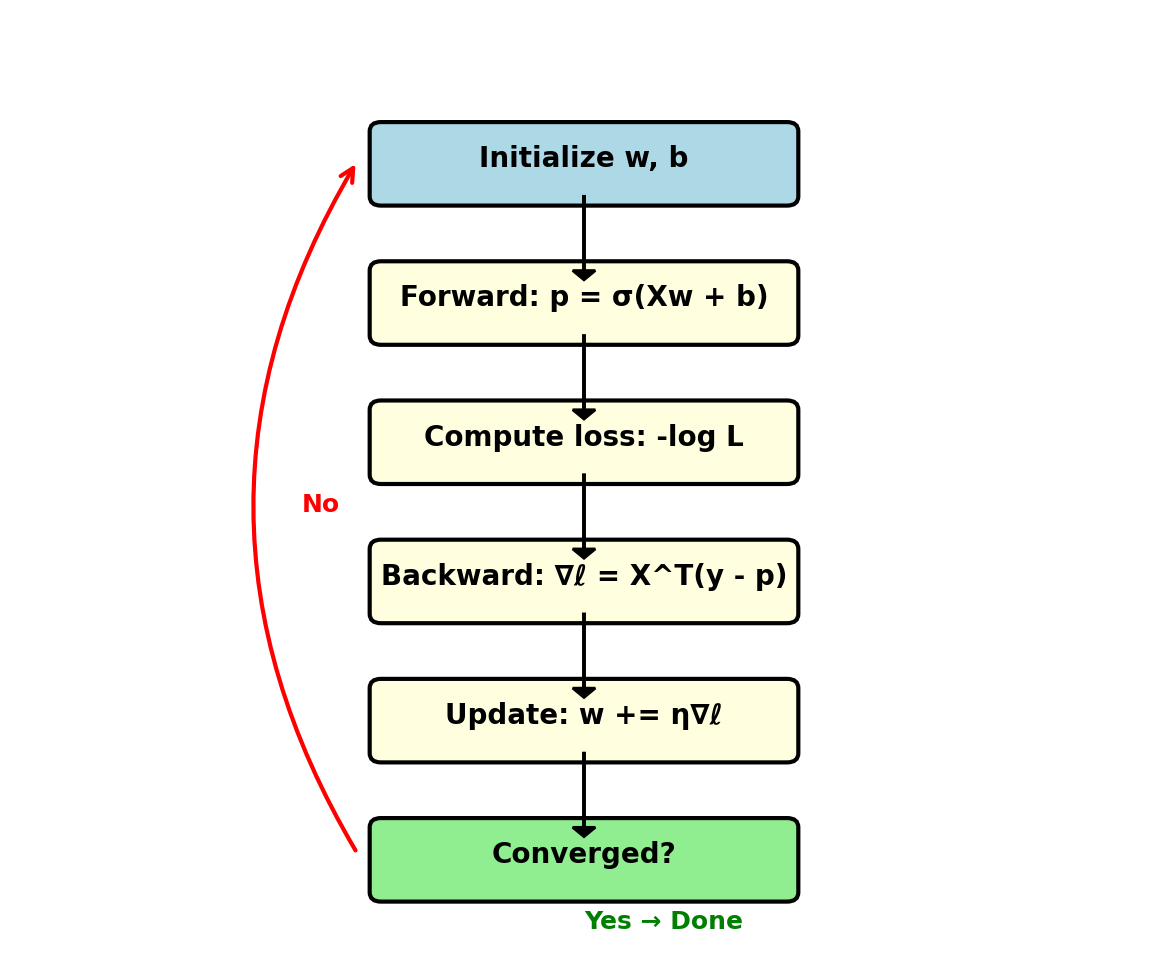

The Complete Logistic Regression Training Loop

Model: \(p = \sigma(\mathbf{w}^T\mathbf{x} + b)\)

Objective: Maximize log-likelihood \[\ell = \sum_{i=1}^n [y_i \log p_i + (1-y_i)\log(1-p_i)]\]

Gradient: \[\nabla_\mathbf{w} \ell = \mathbf{X}^T(\mathbf{y} - \mathbf{p})\]

Update: Gradient ascent \[\mathbf{w} \leftarrow \mathbf{w} + \eta \nabla_\mathbf{w} \ell\]

Converge: When \(||\nabla \ell|| < \epsilon\)

Iterate until convergence (typical: 100s of steps)

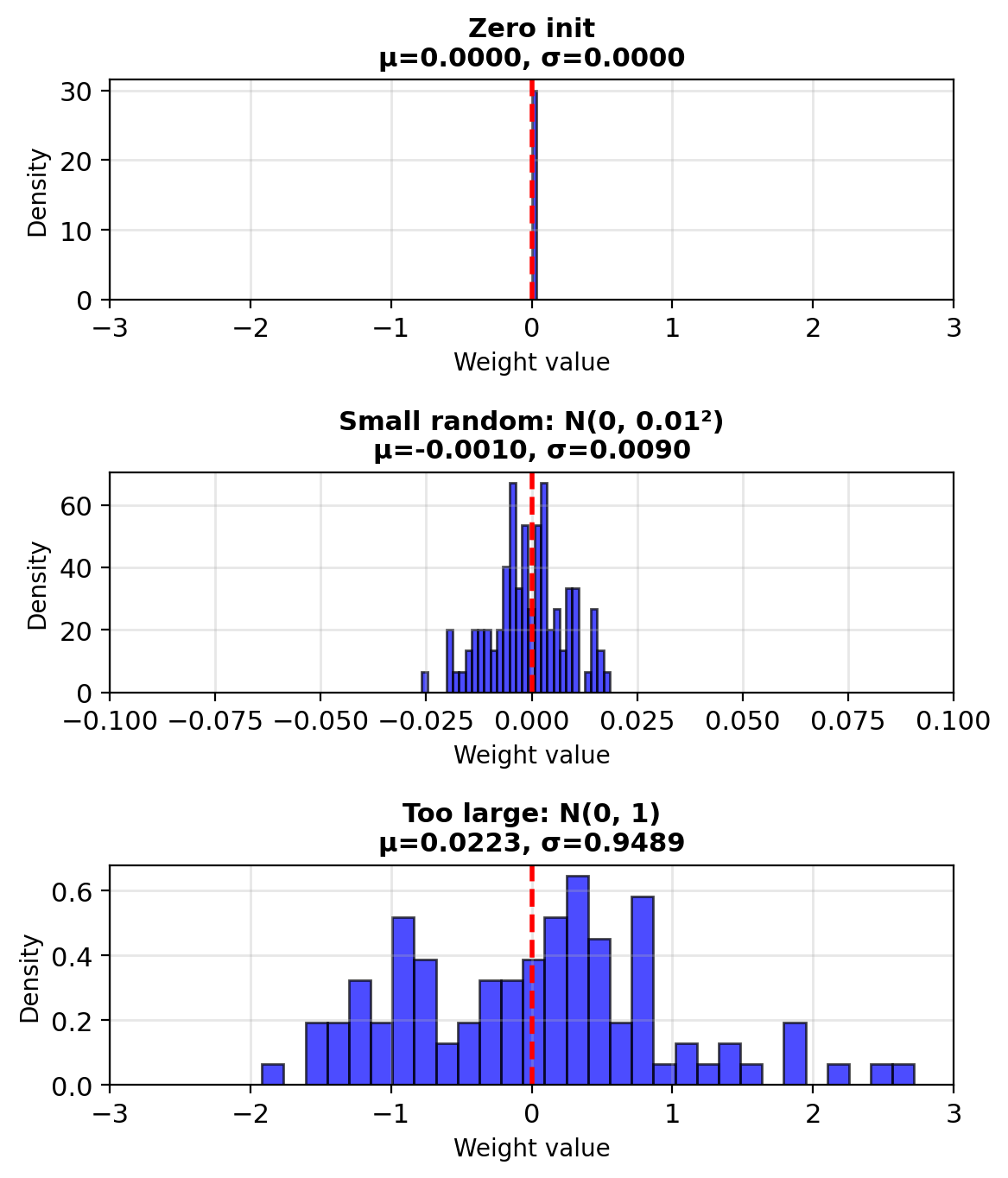

Initialize Weights Before Optimization

Standard initialization:

w = np.random.randn(d) * 0.01

b = 0Why random: Zero works but random is standard

- Gradient: \(\nabla_\mathbf{w} \ell = \mathbf{X}^T(\mathbf{y} - \mathbf{p})\)

- Gradient depends only on data, not symmetry

- With \(\mathbf{w} = \mathbf{0}\): all predictions \(p_i = 0.5\)

- Works for logistic regression (unlike neural networks)

- Random initialization is standard practice

Why small (0.01 scale):

- Prevents sigmoid saturation: \(\sigma(z) \approx 0\) or \(1\) when \(|z|\) large

- Keeps gradients large: \(\sigma'(z) = \sigma(z)(1-\sigma(z))\) peaks at \(z=0\)

- Scale of 0.01 typical for normalized features

Gradient Descent — \(\nabla_\mathbf{w}\)

Update rule (minimize NLL): \[\mathbf{w}^{\text{new}} = \mathbf{w}^{\text{old}} + \eta \cdot \nabla \ell\]

Addition follows from maximizing log-likelihood (equivalent to subtracting gradient of NLL)

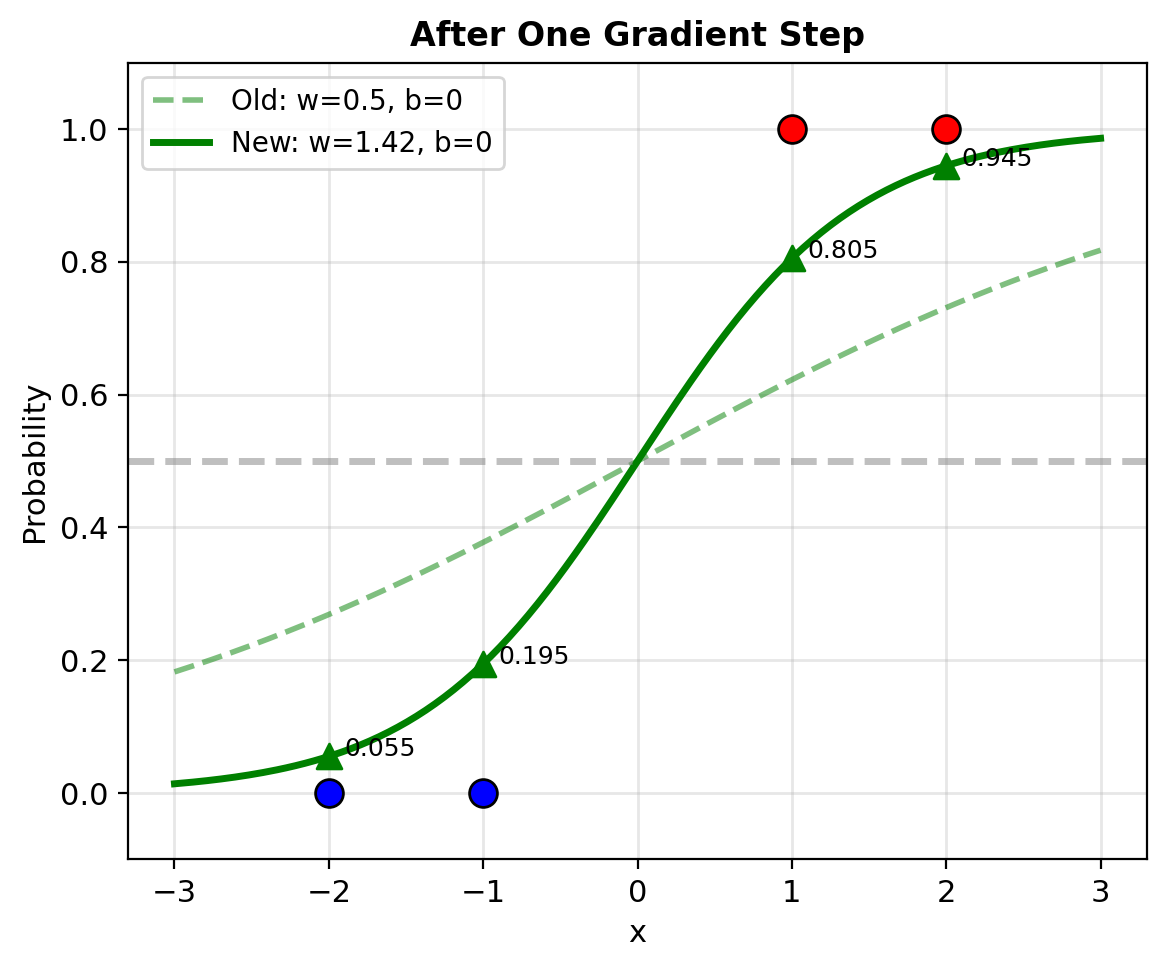

With learning rate \(\eta = 0.5\):

- \(w^{\text{new}} = 0.5 + 0.5 \cdot 1.84 = 1.42\)

- \(b^{\text{new}} = 0 + 0.5 \cdot 0 = 0\)

New predictions:

- \(p_1^{\text{new}} = \sigma(1.42 \cdot (-2)) = 0.055\)

- \(p_2^{\text{new}} = \sigma(1.42 \cdot (-1)) = 0.195\)

- \(p_3^{\text{new}} = \sigma(1.42 \cdot 1) = 0.805\)

- \(p_4^{\text{new}} = \sigma(1.42 \cdot 2) = 0.945\)

NLL decreased from 1.582 to 0.506

- Class 0 predictions closer to 0

- Class 1 predictions closer to 1

- Better separation between classes

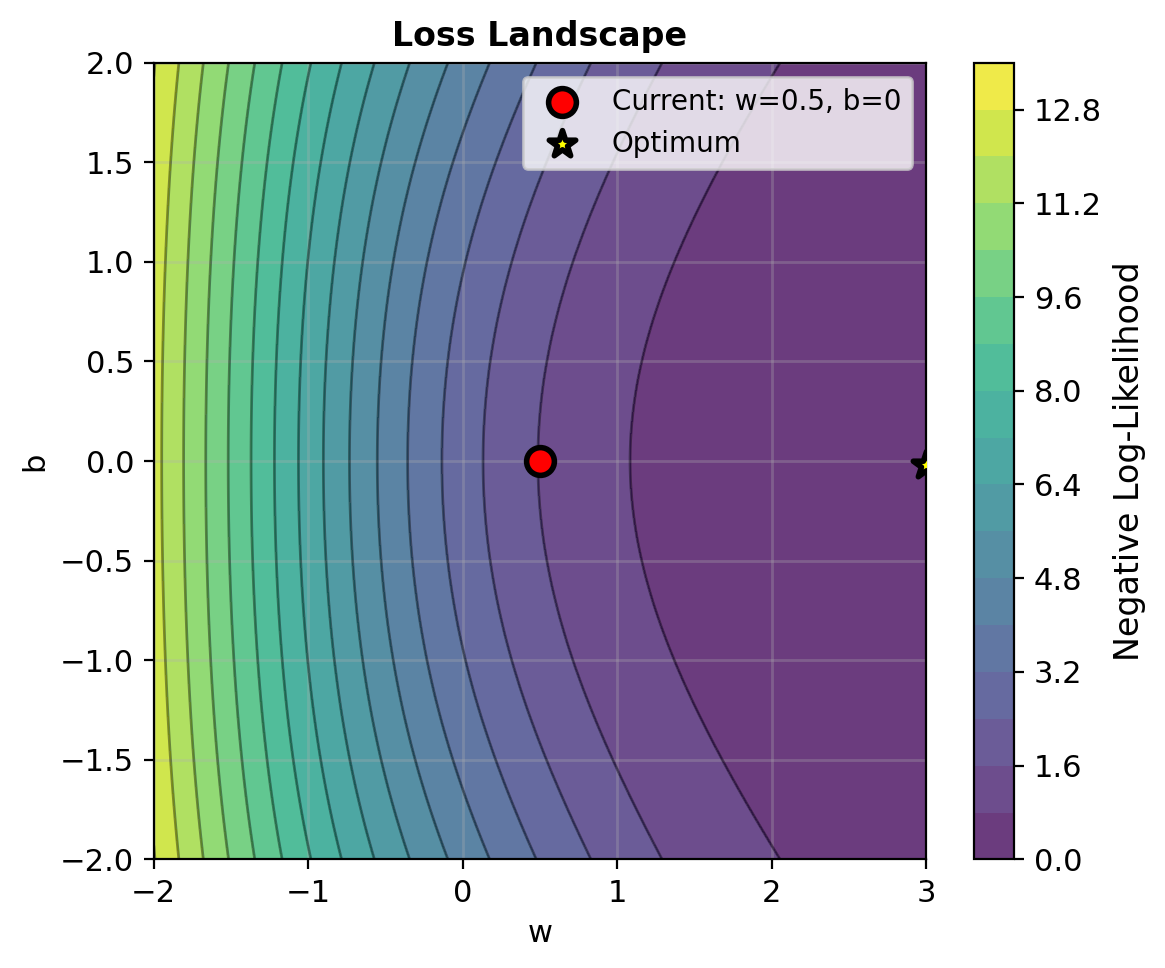

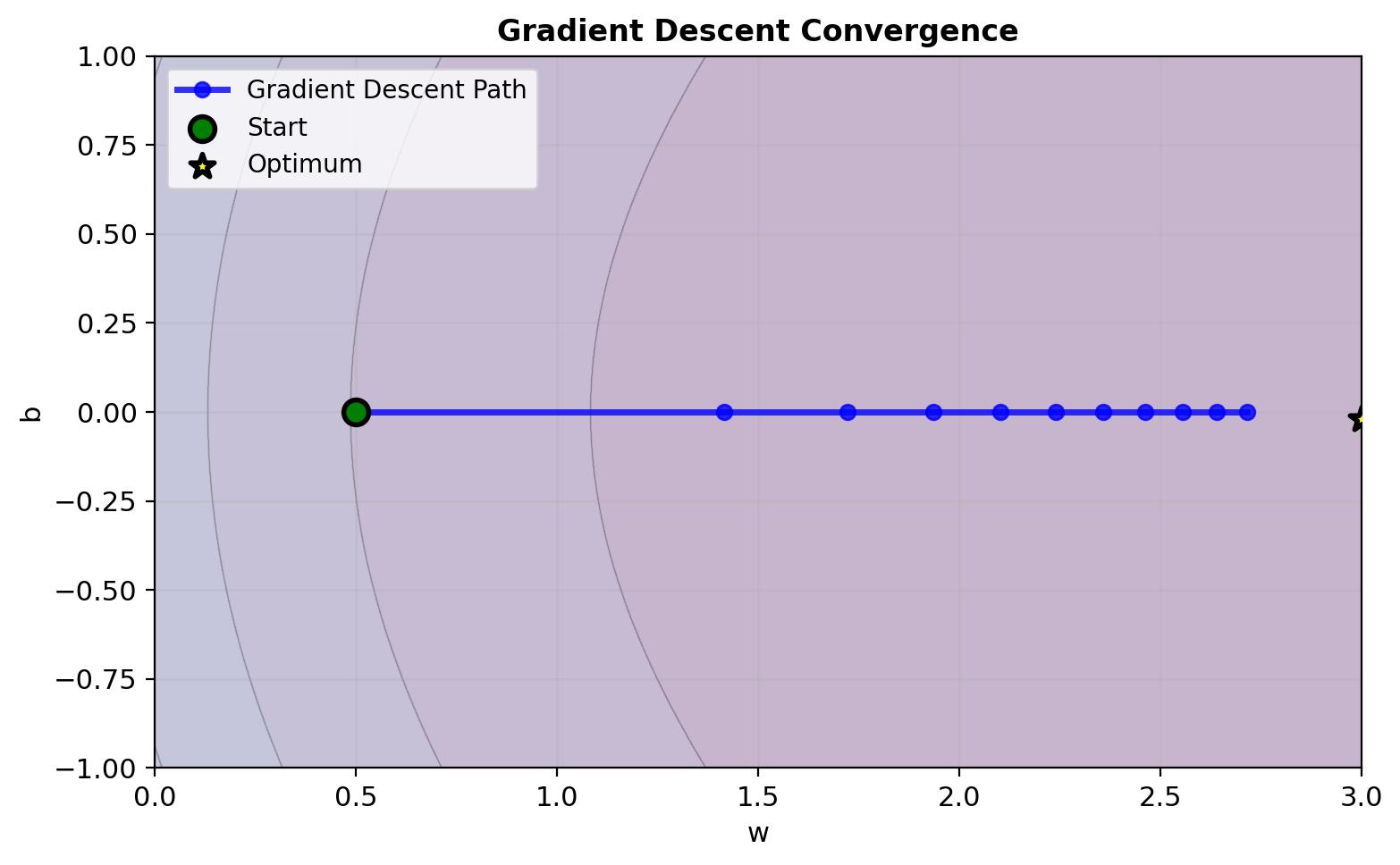

Convergence Analysis (Gradient Descent)

Convexity guarantees convergence to global optimum

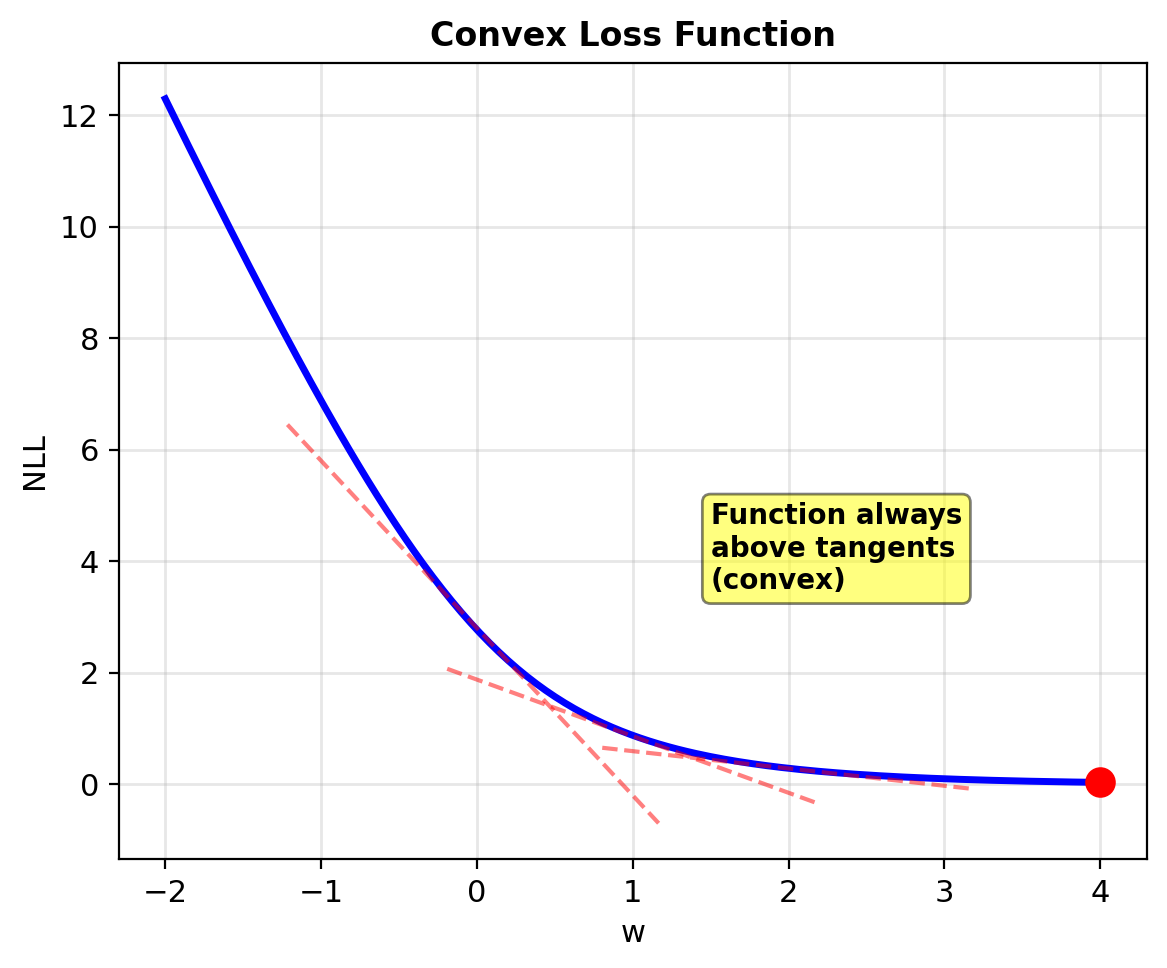

Why Is Logistic Regression Convex?

Theorem: NLL is strictly convex if \(\mathbf{X}\) has full rank.

Proof sketch:

Hessian: \(\mathbf{H} = -\mathbf{X}^T\mathbf{D}\mathbf{X}\)

For any \(\mathbf{v} \neq \mathbf{0}\): \[\mathbf{v}^T(-\mathbf{H})\mathbf{v} = \mathbf{v}^T\mathbf{X}^T\mathbf{D}\mathbf{X}\mathbf{v}\]

Let \(\mathbf{u} = \mathbf{X}\mathbf{v}\): \[= \mathbf{u}^T\mathbf{D}\mathbf{u} = \sum_{i=1}^n p_i(1-p_i)u_i^2\]

Since \(0 < p_i < 1\): all \(p_i(1-p_i) > 0\)

Sum of positive terms → \(\geq 0\)

Equals 0 only if \(\mathbf{u} = \mathbf{0}\)

If \(\mathbf{X}\) full rank: \(\mathbf{X}\mathbf{v} = \mathbf{0} \Rightarrow \mathbf{v} = \mathbf{0}\)

Therefore: \(-\mathbf{H} \succ 0\) (positive definite)

Convexity implications:

| Property | Convex (Logistic) | Non-convex (Neural Net) |

|---|---|---|

| Local minima | None (only global) | Many |

| Optimization | Any method works | Can get stuck |

| Convergence | Guaranteed | No guarantee |

| Initial point | Doesn’t matter | Critical |

| Solution | Unique (if full rank) | Multiple |

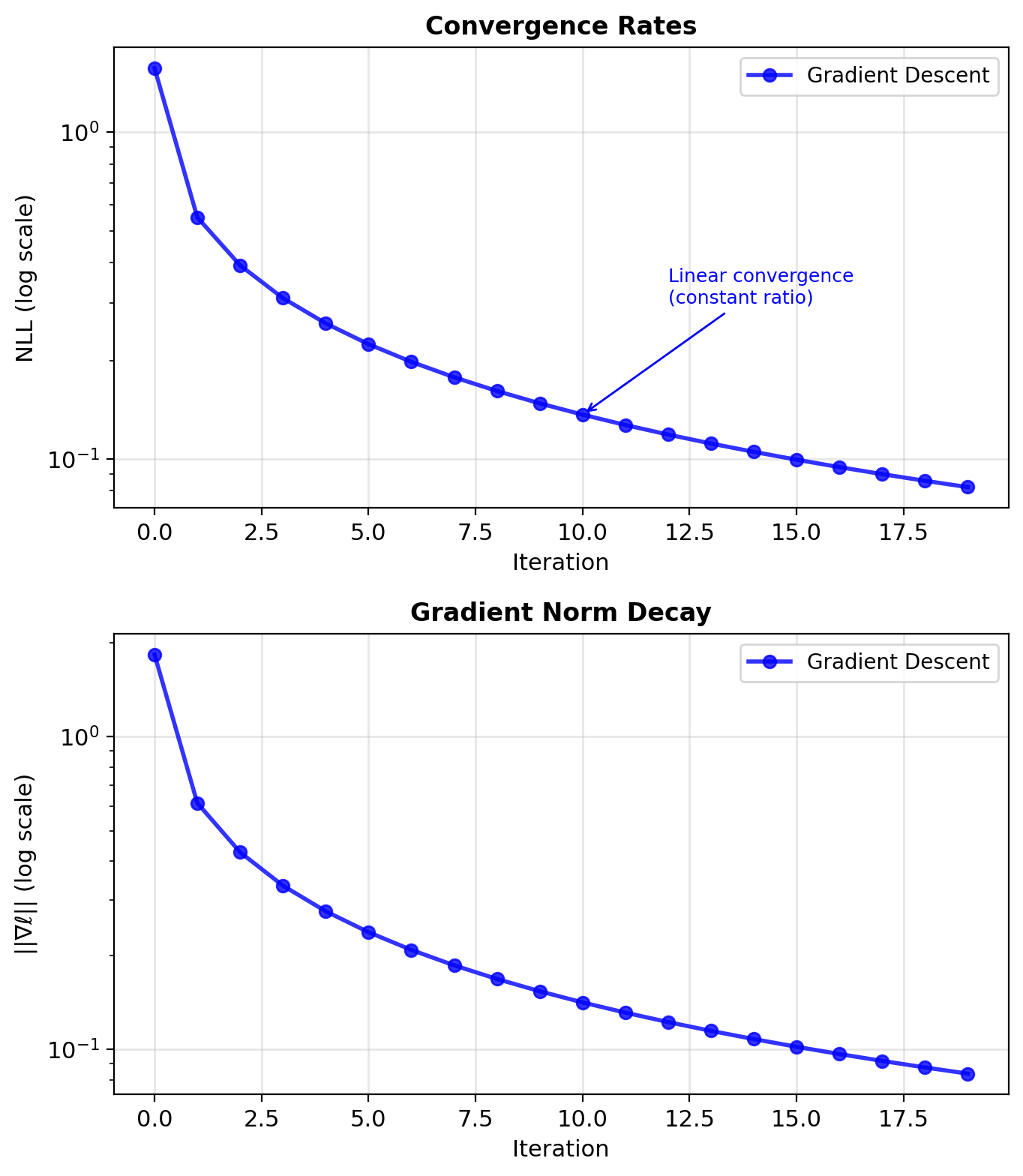

Newton’s Method Converges Quadratically

Gradient Descent:

- Linear convergence: \(\epsilon_{t+1} \leq \rho \cdot \epsilon_t\)

- Rate depends on condition number

- Many iterations needed

- Simple, memory efficient

Newton’s Method:

- Quadratic convergence: \(\epsilon_{t+1} \leq c \cdot \epsilon_t^2\)

- Few iterations (5-10 typical)

- Each iteration expensive: \(O(d^3)\)

- Needs to store/invert Hessian

Trade-off:

- Small \(d\) (<1000): Use Newton

- Large \(d\): Use gradient methods

- Very large \(d\): Use stochastic gradient

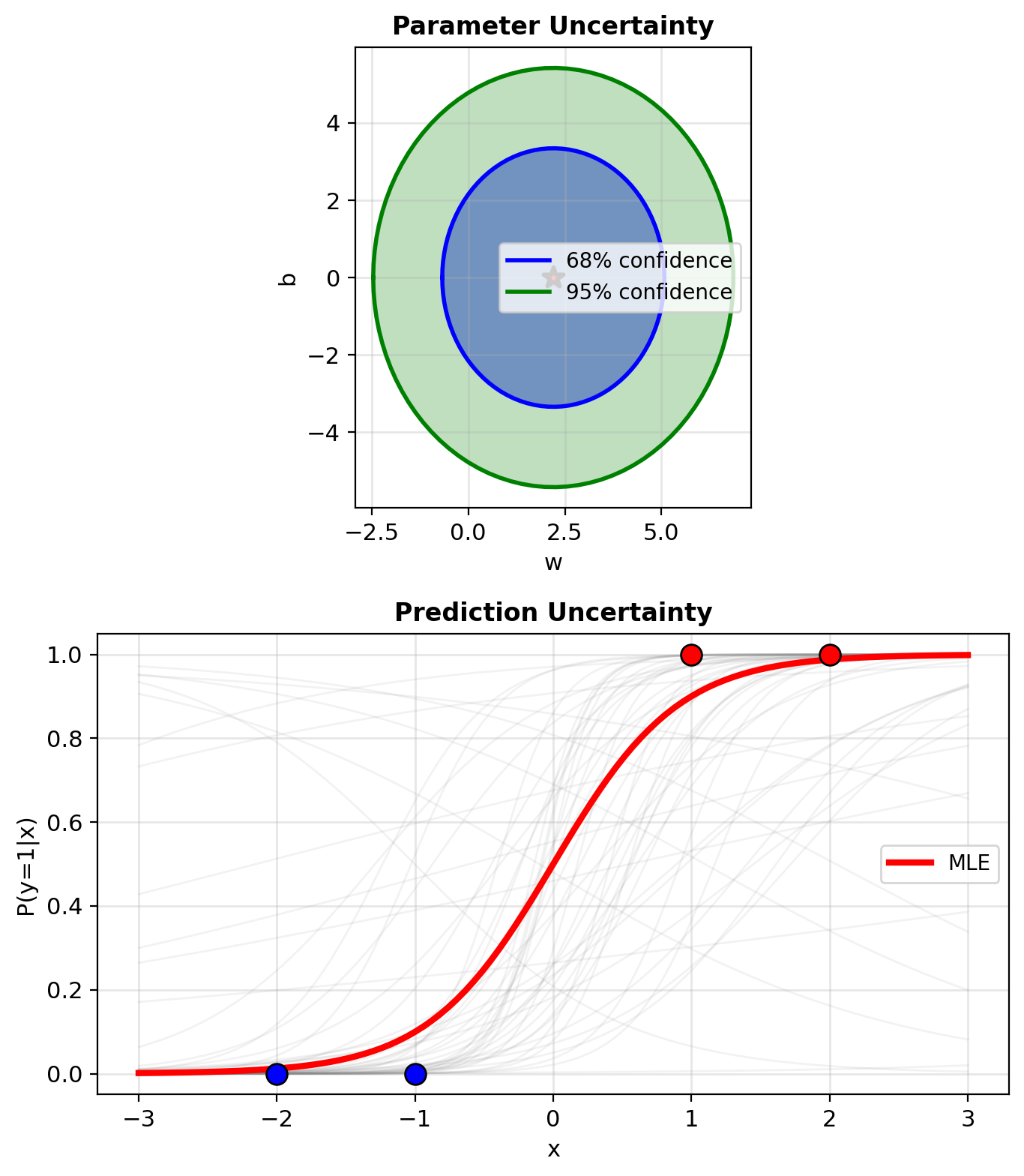

Fisher Information Measures Parameter Certainty

Fisher Information measures parameter certainty: \[\mathcal{I} = \mathbb{E}[-\mathbf{H}] = \mathbb{E}[\mathbf{X}^T\mathbf{D}\mathbf{X}]\]

At convergence for our example:

- \(w^* \approx 2.2\), \(b^* \approx 0\)

- \(p^* = [0.013, 0.050, 0.950, 0.987]\)

Weights at optimum:

- Points 1,4: \(p(1-p) \approx 0.013\) (low)

- Points 2,3: \(p(1-p) \approx 0.048\) (low)

Low weights everywhere → High certainty

Asymptotic distribution: \[\hat{\mathbf{w}} \sim \mathcal{N}(\mathbf{w}^*, \mathcal{I}^{-1}/n)\]

High Fisher information → Low variance → Confident estimates

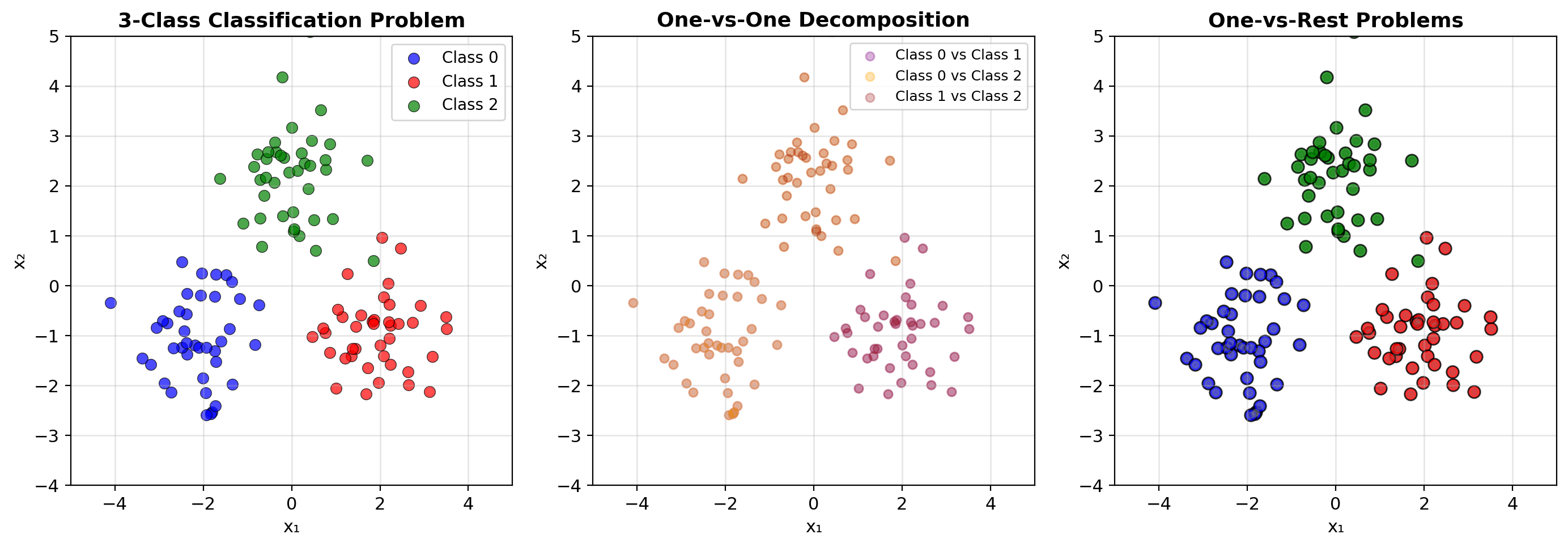

From Binary to K > 2 Classes

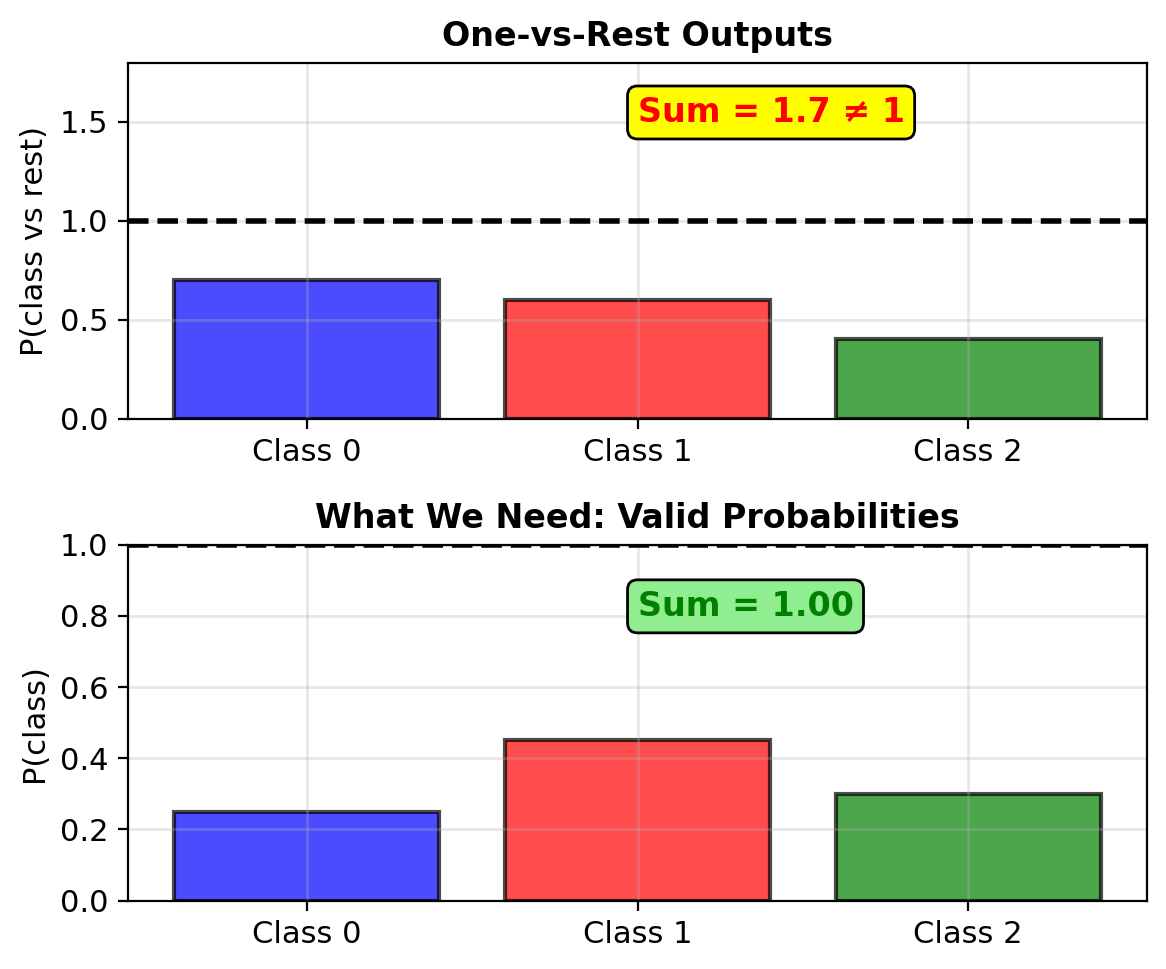

Why One-vs-Rest Fails

One-vs-Rest approach:

- Train K binary classifiers

- Classifier k: class k vs all others

- Predict: argmax of K outputs

Problem: Probabilities do not sum to 1

Example with 3 classes:

- Classifier 0: P(0 vs rest) = 0.7

- Classifier 1: P(1 vs rest) = 0.6

- Classifier 2: P(2 vs rest) = 0.4

Sum = 1.7 ≠ 1

Not valid probabilities for the K classes

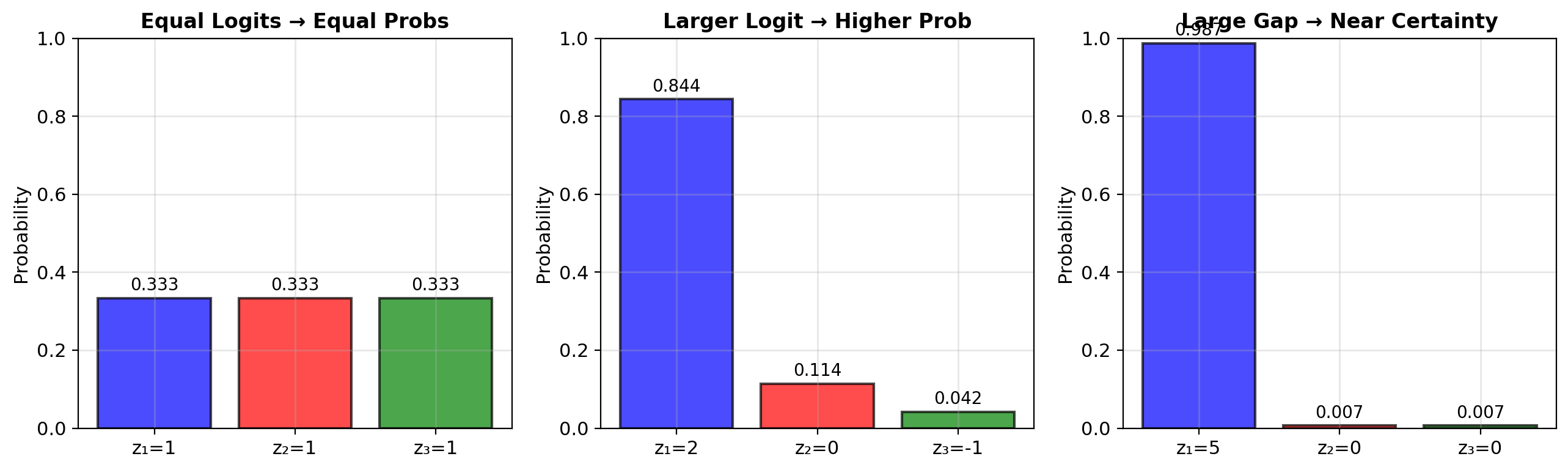

The Softmax Function

Generalize sigmoid to K dimensions:

\[\text{softmax}(\mathbf{z})_k = \frac{e^{z_k}}{\sum_{j=1}^K e^{z_j}}\]

For binary case (K=2):

- Let \(z_1 = 0\) (reference class)

- Then: \(p_2 = \frac{e^{z_2}}{e^0 + e^{z_2}} = \frac{1}{1 + e^{-z_2}} = \sigma(z_2)\)

Softmax reduces to sigmoid when K=2

Softmax Guarantees Valid Probability Distributions

Valid probabilities: All outputs in (0,1), sum to 1 \[\sum_{k=1}^K \text{softmax}(\mathbf{z})_k = 1\]

Preserves order: If \(z_i > z_j\), then \(p_i > p_j\)

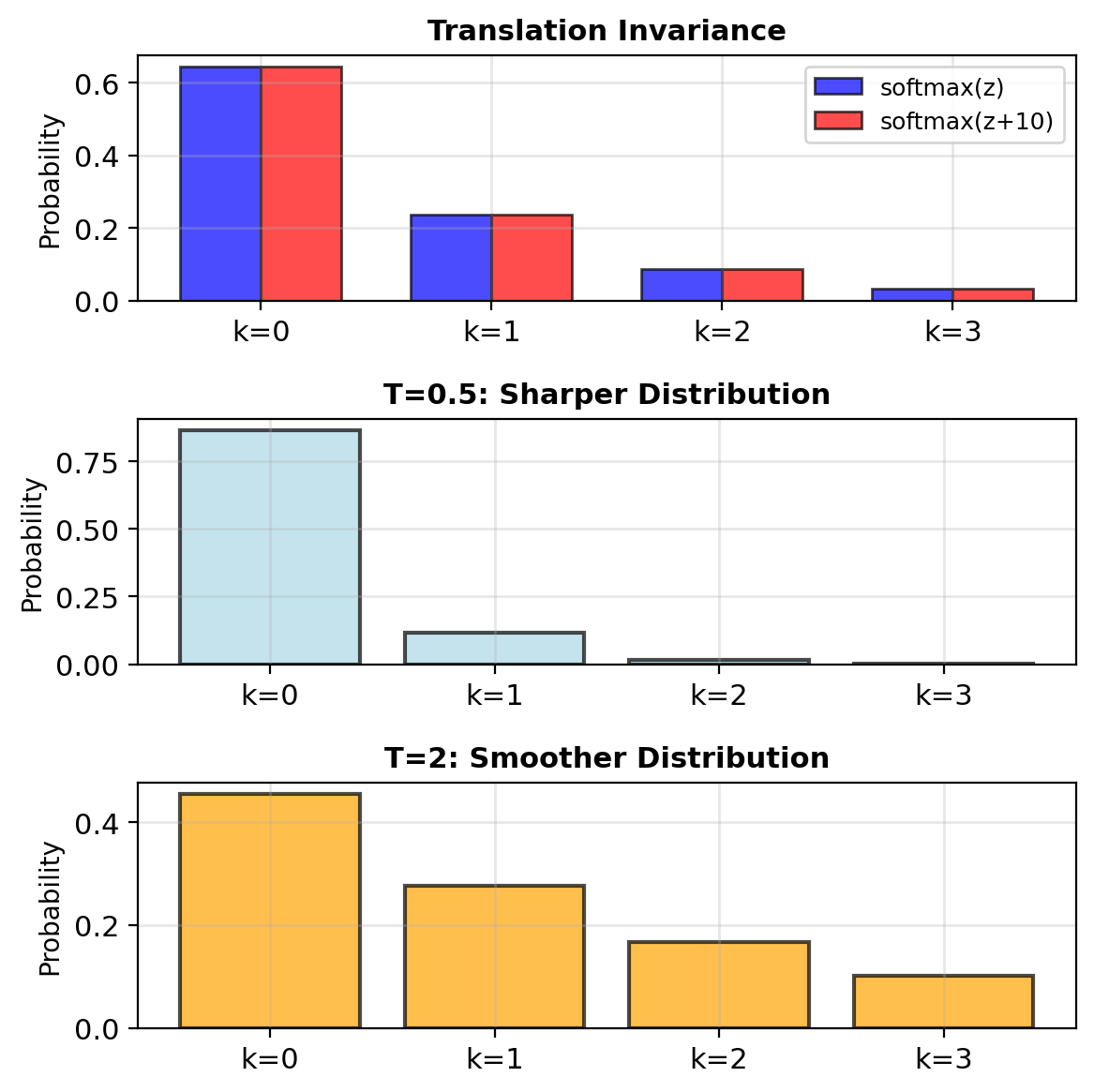

Translation invariant: \[\text{softmax}(\mathbf{z} + c) = \text{softmax}(\mathbf{z})\]

Since: \(\frac{e^{z_k + c}}{\sum_j e^{z_j + c}} = \frac{e^c \cdot e^{z_k}}{e^c \cdot \sum_j e^{z_j}} = \frac{e^{z_k}}{\sum_j e^{z_j}}\)

Temperature scaling: \[\text{softmax}(\mathbf{z}/T)\]

- \(T \to 0\): approaches argmax (one-hot)

- \(T \to \infty\): uniform distribution

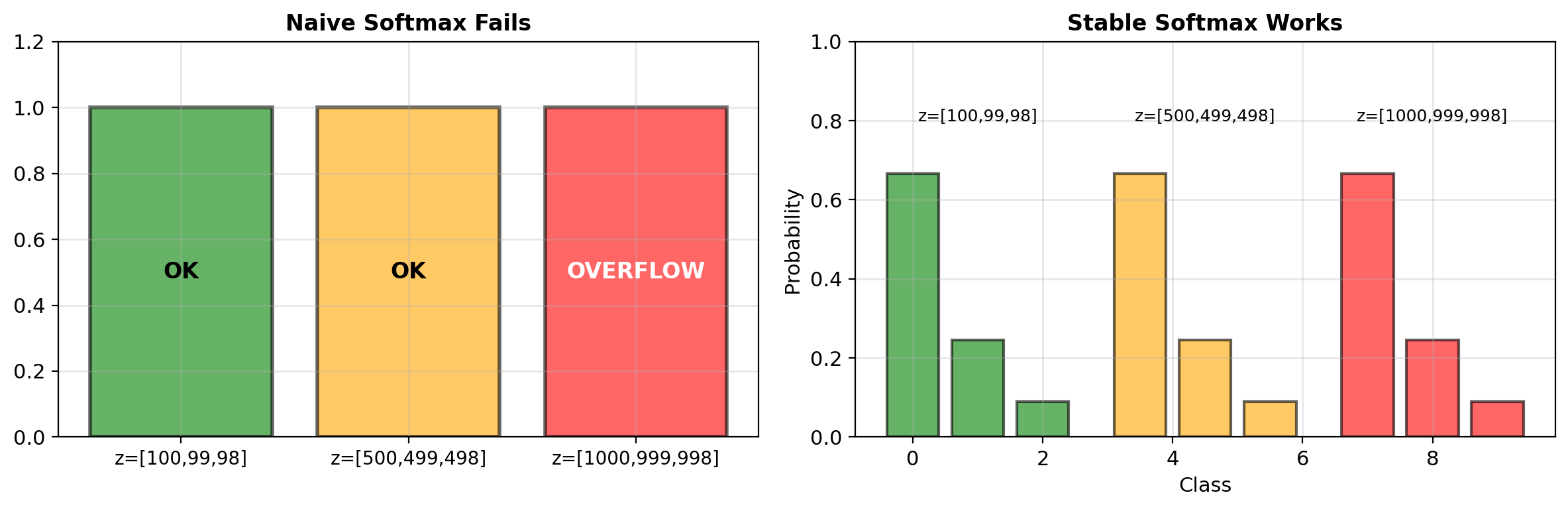

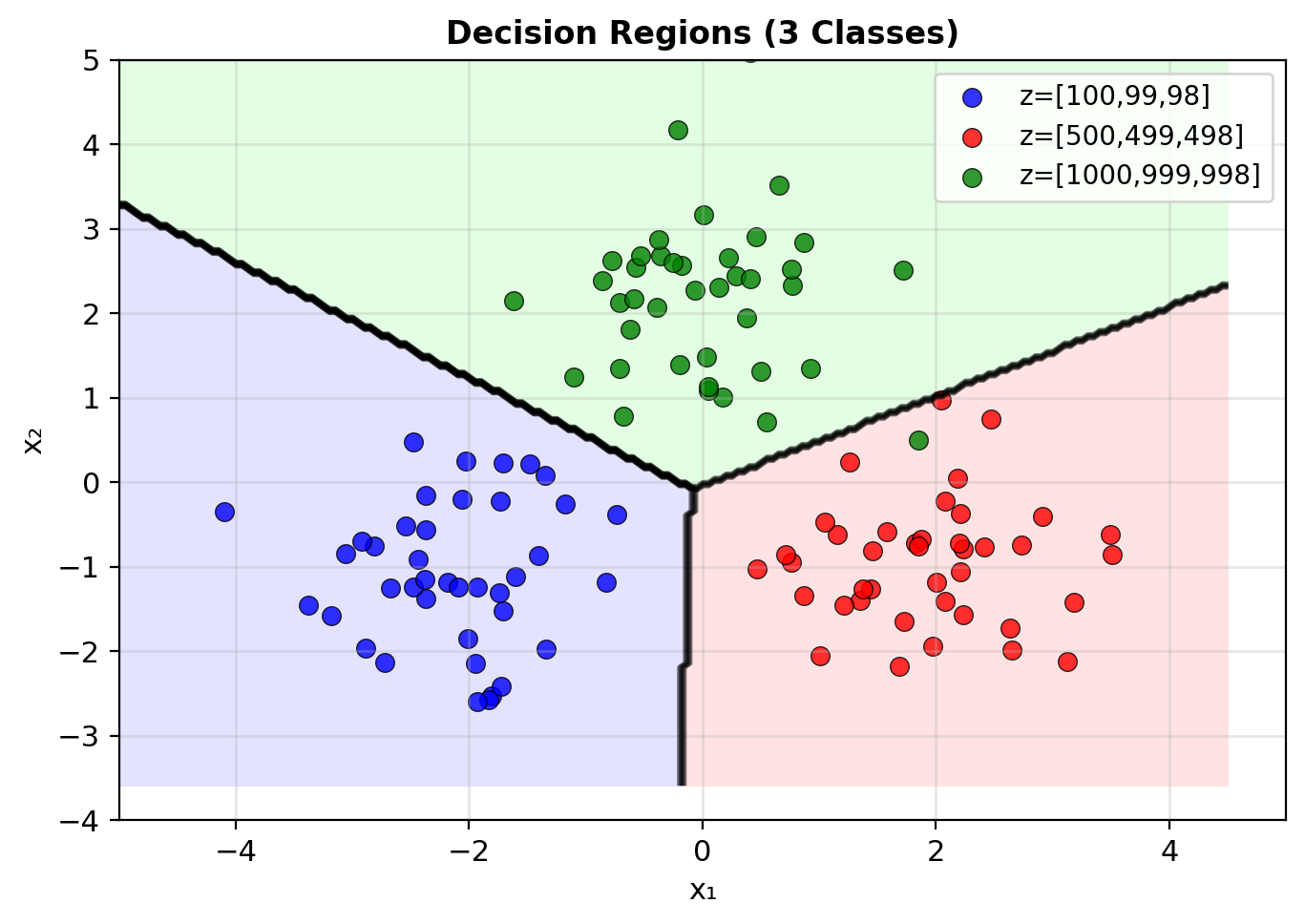

Numerical Stability of Softmax

Problem: Exponentials overflow/underflow

z = [1000, 999, 998]

exp(1000) → inf # OverflowSolution: Take advantage of translation invariance

Subtract maximum before exponent

\[\text{softmax}(\mathbf{z}) = \text{softmax}(\mathbf{z} - \max(\mathbf{z}))\]

z = [1000, 999, 998]

z_stable = z - max(z) = [0, -1, -2]

softmax(z_stable) = [0.665, 0.245, 0.090] # Valid

Multinomial Logistic Regression – One Linear Model per Class

For K classes, we need:

- K linear models: \(z_k = \mathbf{w}_k^T\mathbf{x} + b_k\)

- Parameter matrix: \(\mathbf{W} \in \mathbb{R}^{d \times K}\)

- Bias vector: \(\mathbf{b} \in \mathbb{R}^K\)

Model: \[\mathbf{z} = \mathbf{W}^T\mathbf{x} + \mathbf{b}\] \[P(y=k|\mathbf{x}) = \text{softmax}(\mathbf{z})_k\]

Over-parameterized:

- Can set \(\mathbf{w}_K = \mathbf{0}\), \(b_K = 0\) (reference class)

- Still get valid probabilities

- Reduces parameters by \(d+1\)

Each boundary is linear (hyperplane)

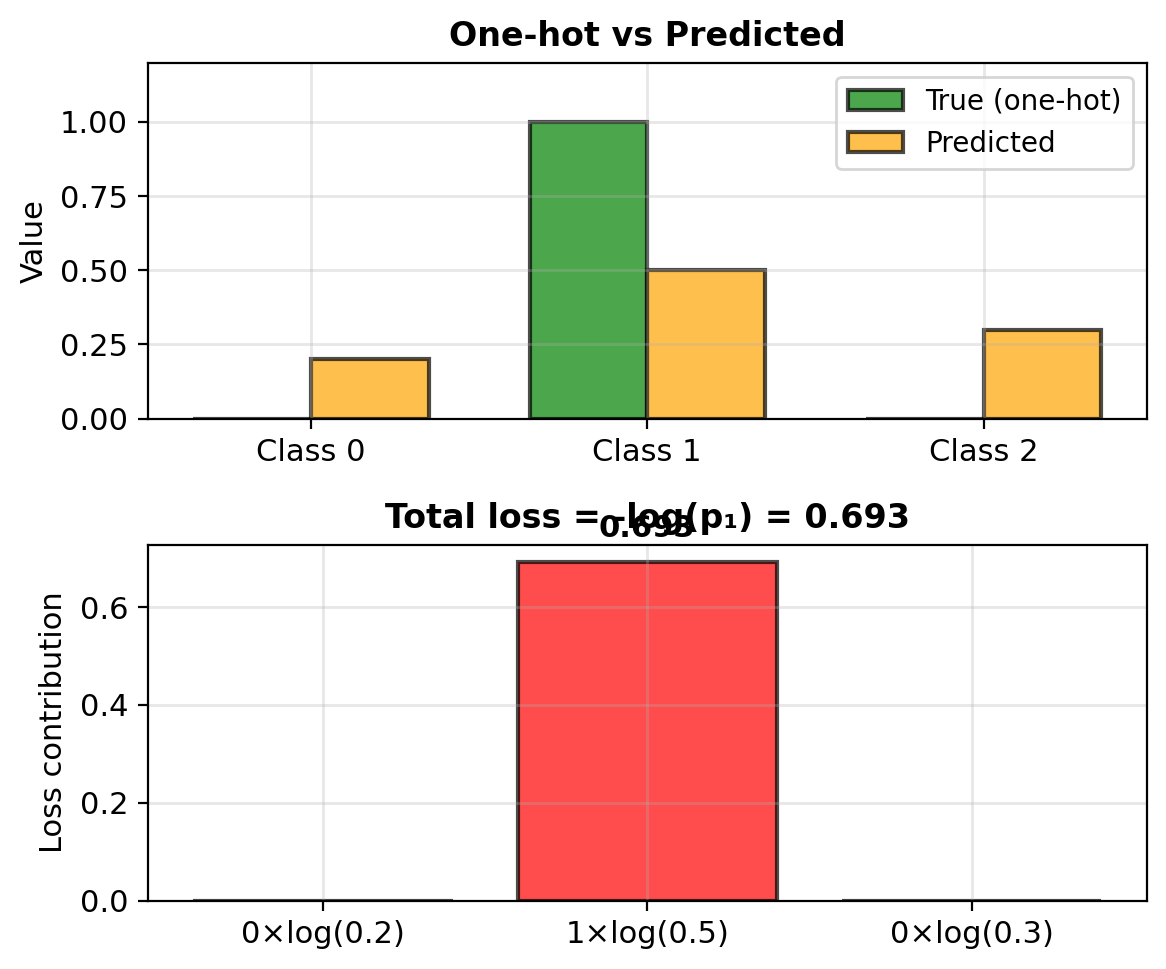

Cross-Entropy for Multi-Class

One-hot encoding for labels:

- Class 0: \(\mathbf{y} = [1, 0, 0]\)

- Class 1: \(\mathbf{y} = [0, 1, 0]\)

- Class 2: \(\mathbf{y} = [0, 0, 1]\)

Cross-entropy loss: \[\mathcal{L} = -\sum_{k=1}^K y_k \log p_k\]

Since only one \(y_k = 1\): \[\mathcal{L} = -\log p_{\text{true class}}\]

For entire dataset: \[\text{NLL} = -\sum_{i=1}^n \log p_{i,y_i}\]

where \(p_{i,y_i}\) is predicted probability for true class of sample \(i\)

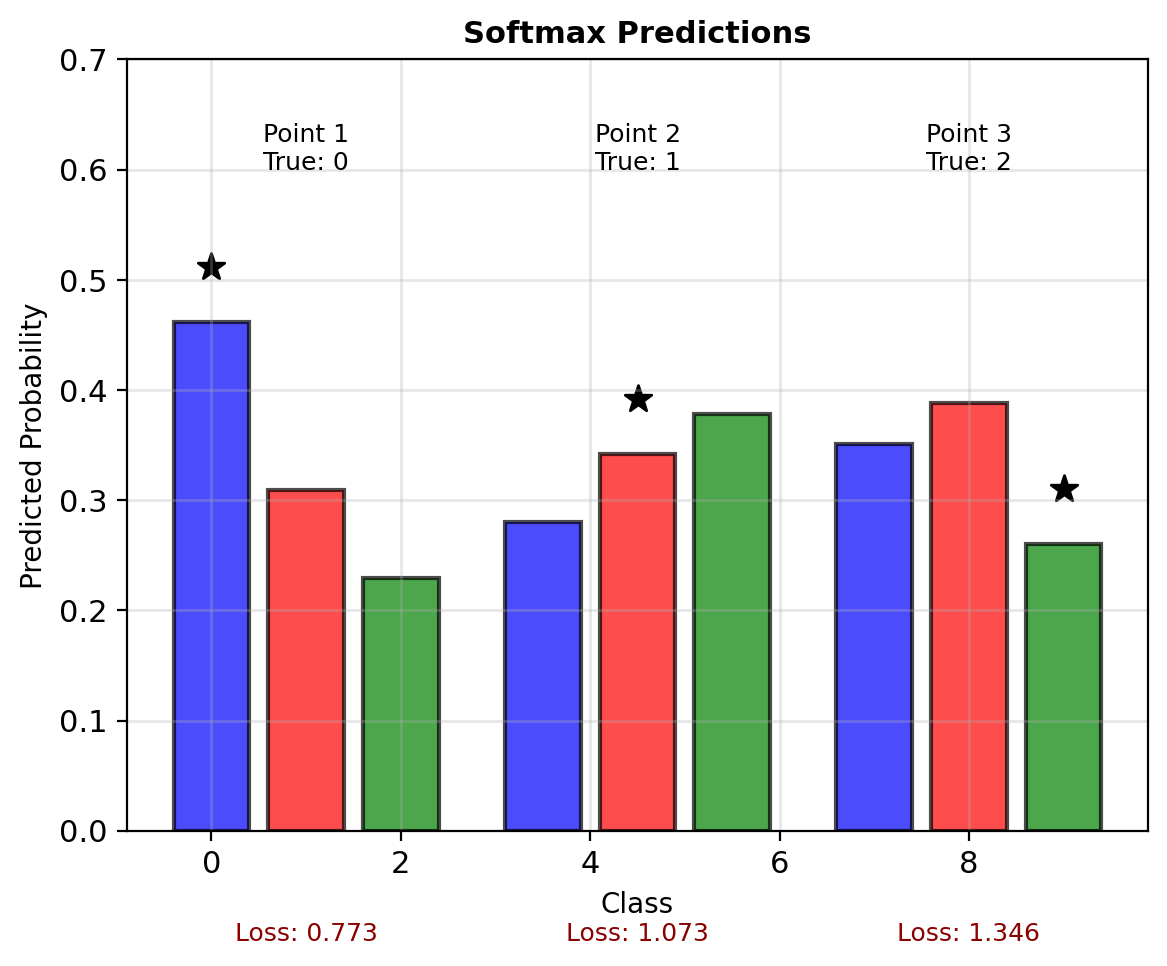

3-Class Softmax Computation

Data: 3 points, 3 classes

X = [[1, 0], [-1, 0], [0, 1]]

y = [0, 1, 2] # Class labelsCurrent parameters:

W = [[0.5, 0.2, 0], # w for class 0

[0.1, 0.3, 0]] # w for class 1,2

b = [0.1, 0, -0.1]Computing predictions:

Point 1: \(\mathbf{x} = [1, 0]\)

- \(z_0 = 0.5(1) + 0.1(0) + 0.1 = 0.6\)

- \(z_1 = 0.2(1) + 0.3(0) + 0 = 0.2\)

- \(z_2 = 0(1) + 0(0) - 0.1 = -0.1\)

- \(\mathbf{p} = \text{softmax}([0.6, 0.2, -0.1]) = [0.47, 0.32, 0.21]\)

- True class: 0, Loss: \(-\log(0.47) = 0.76\)

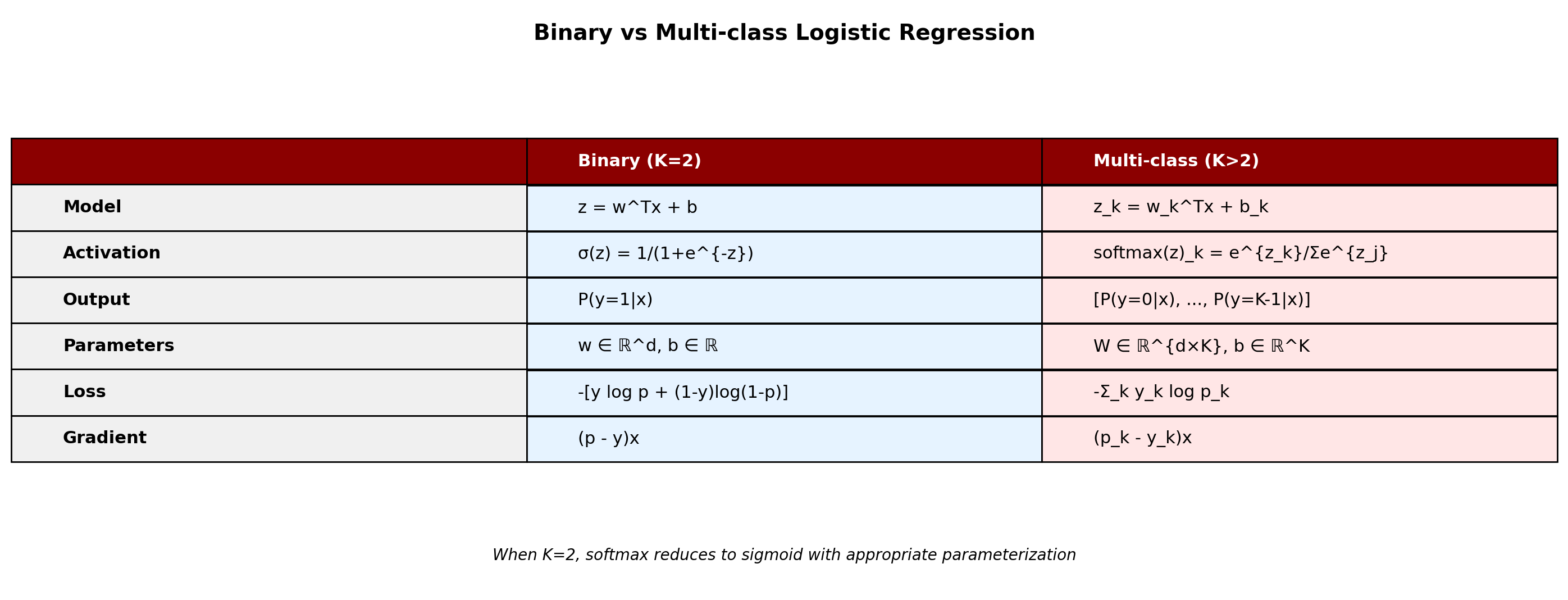

Binary to Multiclass – A Unified View

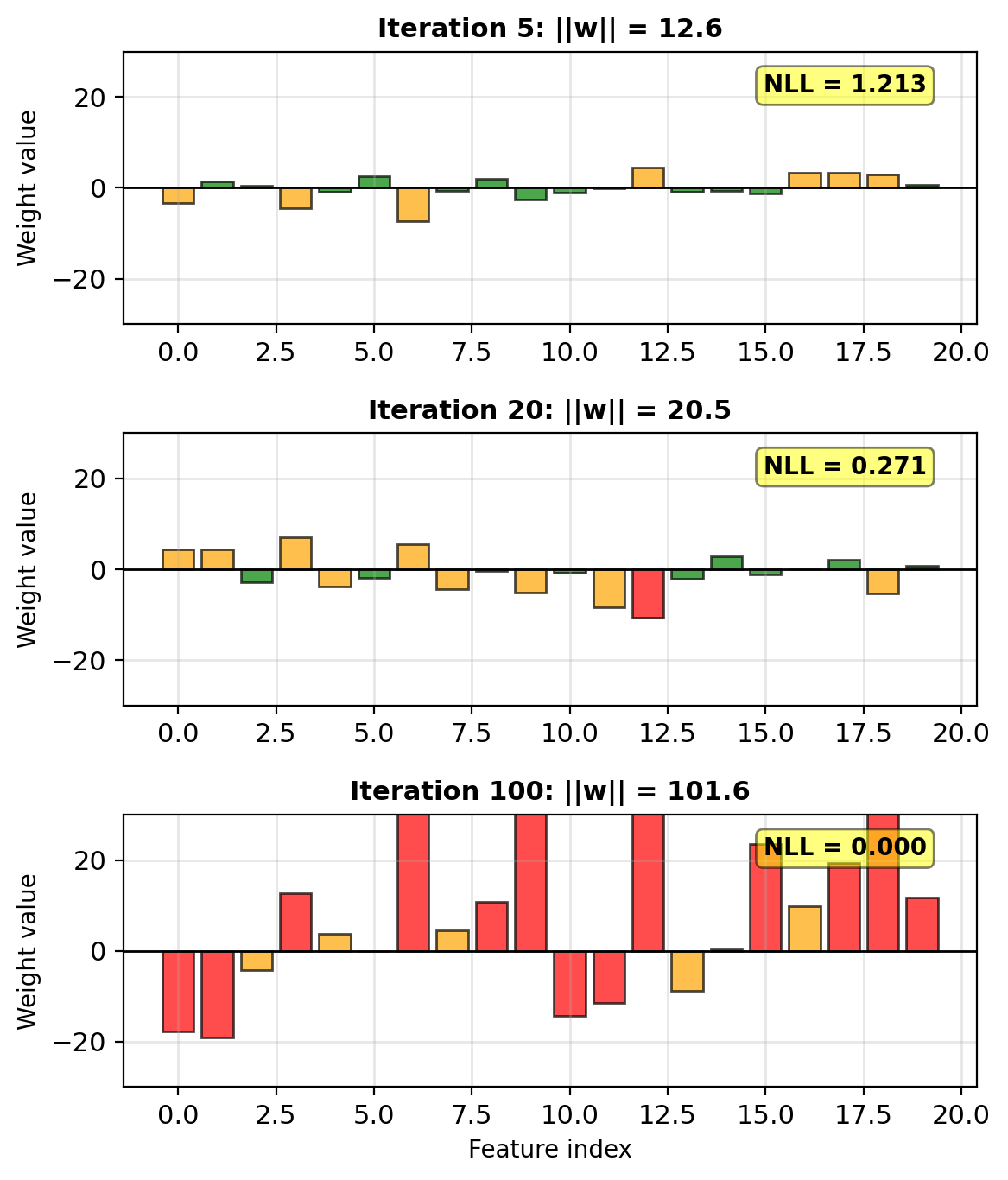

Separable Data Leads to Weight Explosion in MLE

Perfect separation scenario:

# 2D data with polynomial features

X = [[-2, -1], [-1, -2], [1, 2], [2, 1]]

y = [0, 0, 1, 1]

# Add polynomial features

X_poly = [[x1, x2, x1², x2², x1x2]

for x1, x2 in X]With 5 features for 4 points:

- Can achieve perfect separation

- MLE drives weights → ∞

- Predictions become 0 or 1 exactly

- No unique solution

The problem:

- Loss keeps decreasing: NLL → 0

- But weights explode: ||w|| → ∞

- Model becomes overconfident

- Poor generalization to new data

As ||w|| increases:

- Decision boundary sharpens

- Probabilities → 0 or 1

- Model becomes “too sure”

Weight Explosion in High Dimensions

Example: 100 features, 80 samples

Without regularization:

n, d = 80, 100 # More features than samples

X = np.random.randn(n, d)

y = (X @ w_true + noise > 0).astype(int)What happens during optimization:

- Early iterations: Reasonable weights

- Middle: Some weights grow large

- Late: Many weights explode

- “Solution”: Perfect training accuracy

- But: Poor generalization (test performance)

Weight explosion occurs when:

- \(d > n\) (more features than samples)

- Features are highly correlated

- Perfect or near-perfect separation exists

Loss decreases but weights are unstable.

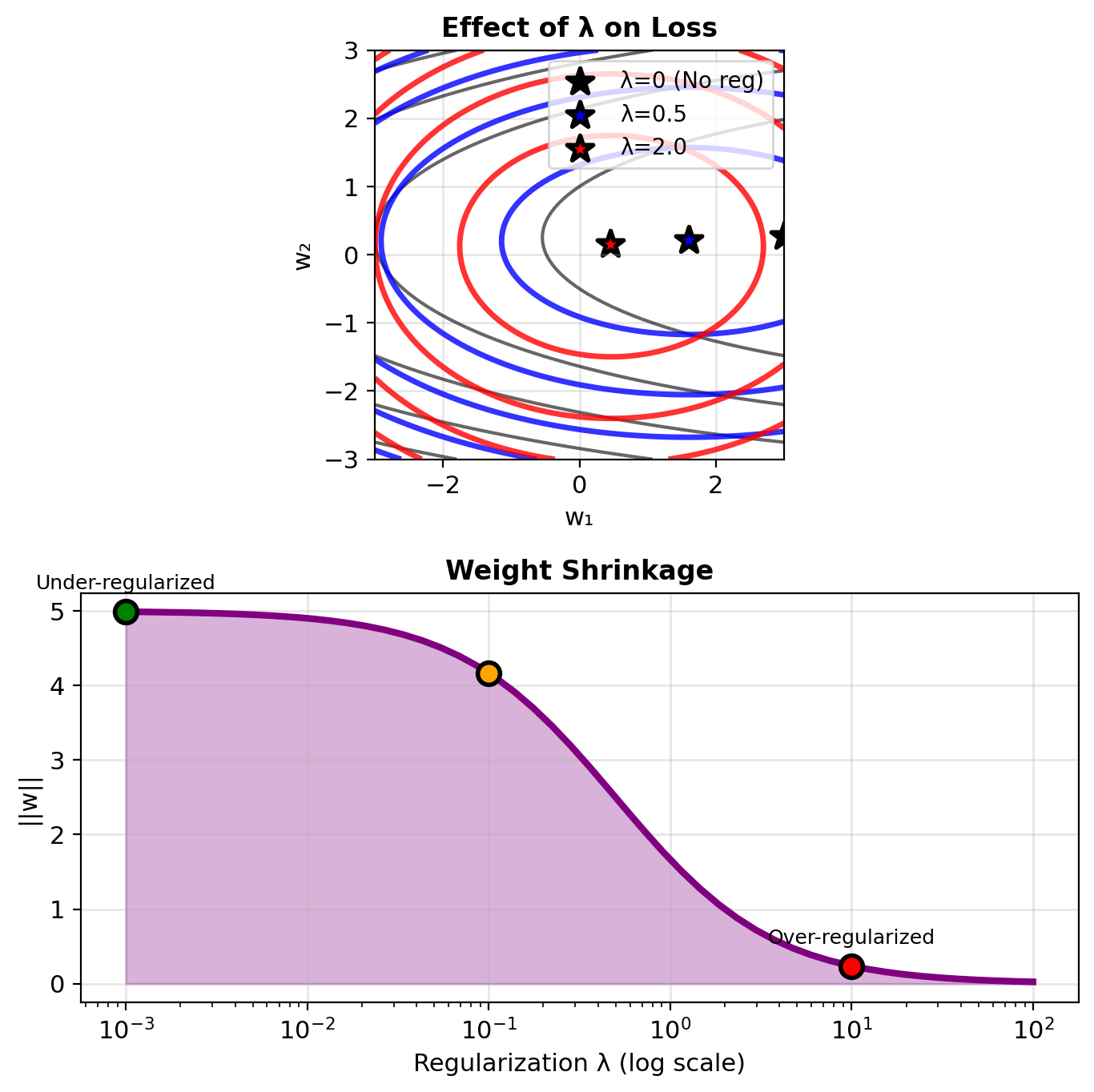

Ridge (L2) Regularization Penalizes Large Weights

Modified objective: \[\mathcal{L}_{\text{ridge}} = \underbrace{-\ell(\mathbf{w})}_{\text{NLL}} + \underbrace{\lambda ||\mathbf{w}||^2}_{\text{penalty}}\]

Gradient with regularization: \[\nabla \mathcal{L}_{\text{ridge}} = -\mathbf{X}^T(\mathbf{y} - \mathbf{p}) + 2\lambda\mathbf{w}\]

Compare to unregularized: \[\nabla \ell = \mathbf{X}^T(\mathbf{y} - \mathbf{p})\]

Effect: Pull weights toward zero

Update rule: \[\mathbf{w} \leftarrow \mathbf{w} - \eta[\nabla \ell - 2\lambda\mathbf{w}]\] \[= (1 - 2\eta\lambda)\mathbf{w} - \eta\nabla \ell\]

Weight decay: Shrink by factor \((1 - 2\eta\lambda)\)

L2 Regularization = Bias toward smaller weights.

Larger λ → Smaller weights → More stable model

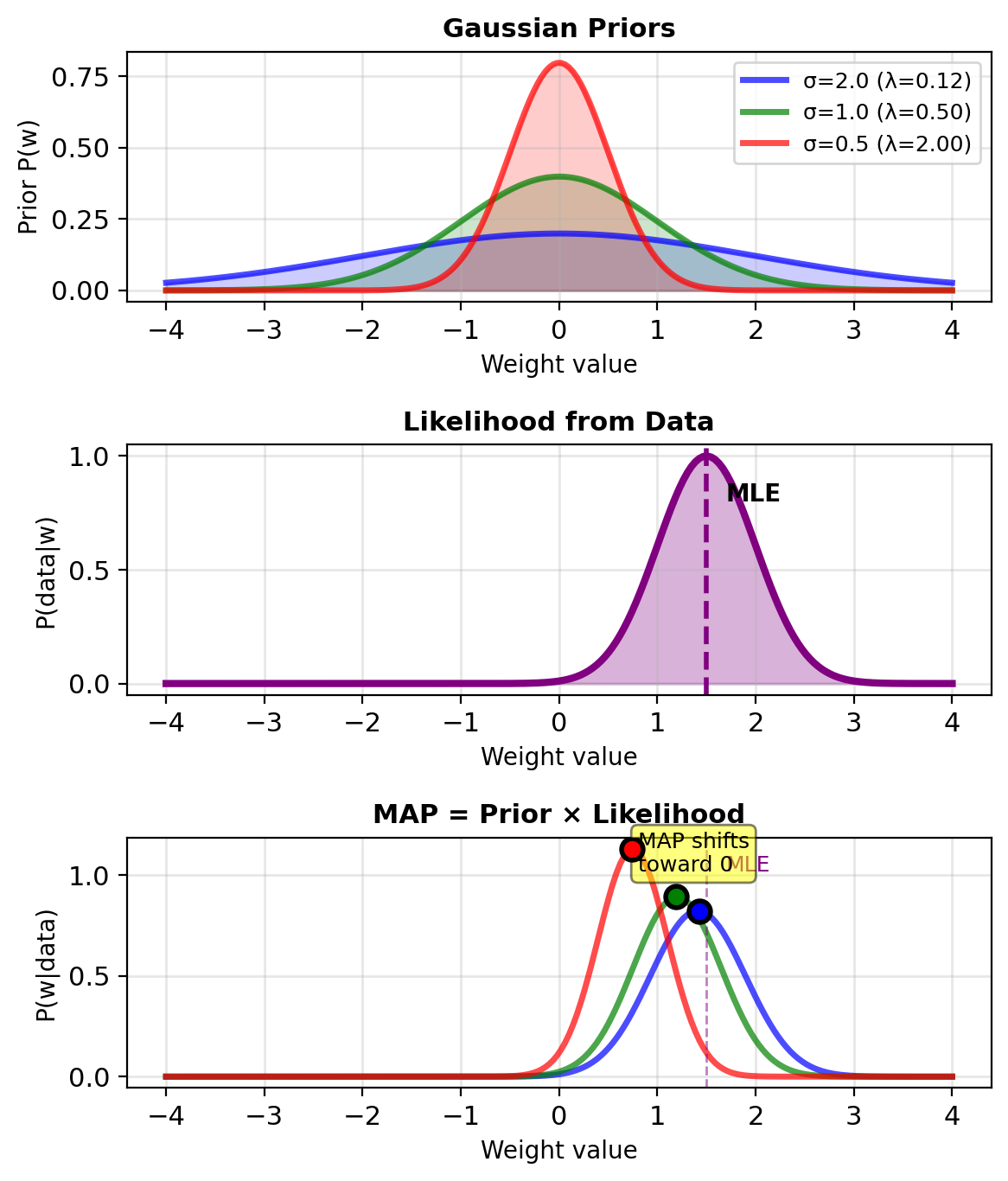

L2 Regularization = Gaussian Prior on Weights

L2 regularization = Gaussian prior

Prior on weights: \[P(\mathbf{w}) = \mathcal{N}(\mathbf{0}, \sigma^2\mathbf{I})\] \[\propto \exp\left(-\frac{||\mathbf{w}||^2}{2\sigma^2}\right)\]

MAP estimation: \[\hat{\mathbf{w}}_{\text{MAP}} = \arg\max_\mathbf{w} P(\mathcal{D}|\mathbf{w})P(\mathbf{w})\]

Taking logarithm: \[= \arg\max_\mathbf{w} \left[\log P(\mathcal{D}|\mathbf{w}) + \log P(\mathbf{w})\right]\] \[= \arg\max_\mathbf{w} \left[\ell(\mathbf{w}) - \frac{||\mathbf{w}||^2}{2\sigma^2}\right]\]

With \(\lambda = \frac{1}{2\sigma^2}\): \[= \arg\min_\mathbf{w} \left[-\ell(\mathbf{w}) + \lambda ||\mathbf{w}||^2\right]\]

This is Ridge regression

Smaller σ gives stronger regularization

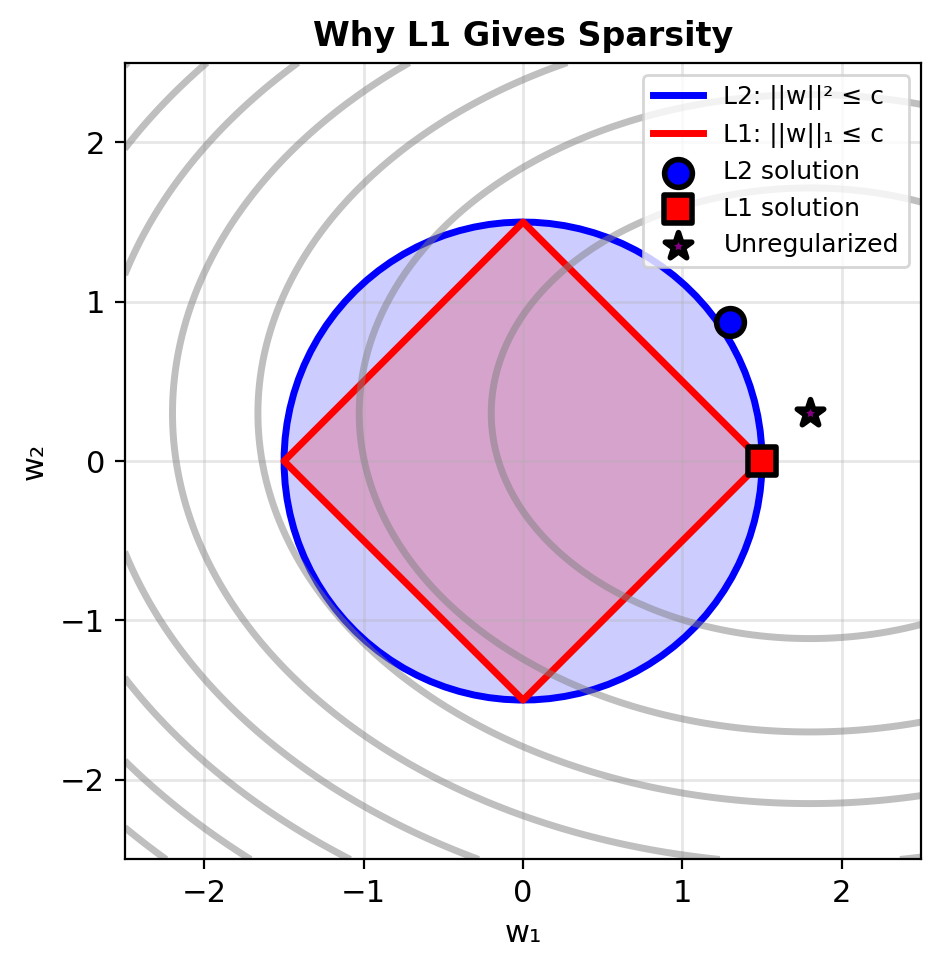

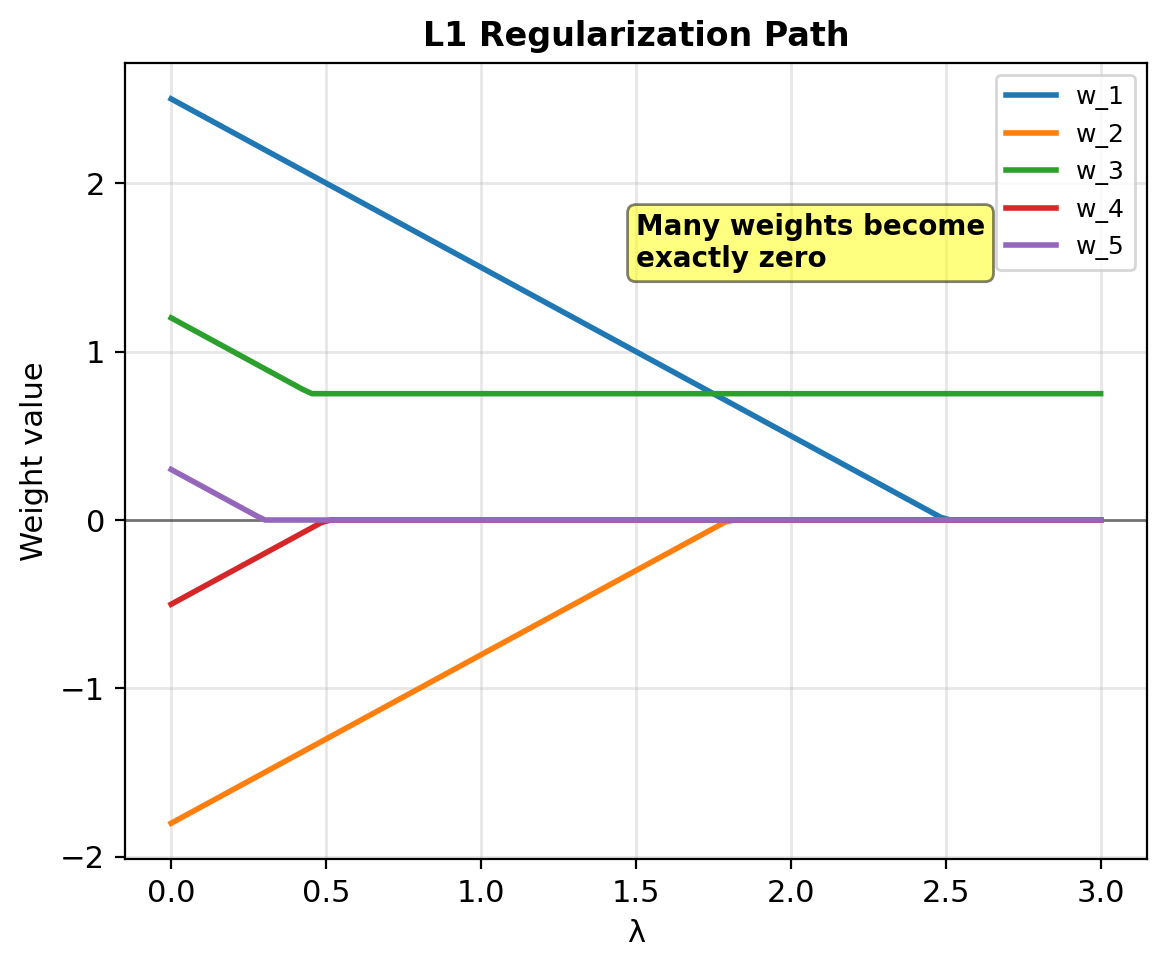

LASSO (L1) Regularization Drives Weights to Exactly Zero

LASSO (Least Absolute Shrinkage and Selection Operator)

L1 penalty: \[\mathcal{L}_{\text{lasso}} = -\ell(\mathbf{w}) + \lambda ||\mathbf{w}||_1\] \[= -\ell(\mathbf{w}) + \lambda \sum_{j=1}^d |w_j|\]

Subgradient (not differentiable at 0): \[\partial_{w_j} \mathcal{L} = -\frac{\partial \ell}{\partial w_j} + \lambda \cdot \text{sign}(w_j)\]

where \(\text{sign}(w) = \begin{cases} +1 & w > 0 \\ [-1, 1] & w = 0 \\ -1 & w < 0 \end{cases}\)

Induces exact sparsity: Many weights become exactly zero

Bayesian view: Laplace prior \[P(\mathbf{w}) \propto \exp(-\lambda ||\mathbf{w}||_1)\]

L1 hits corners → Some weights exactly 0

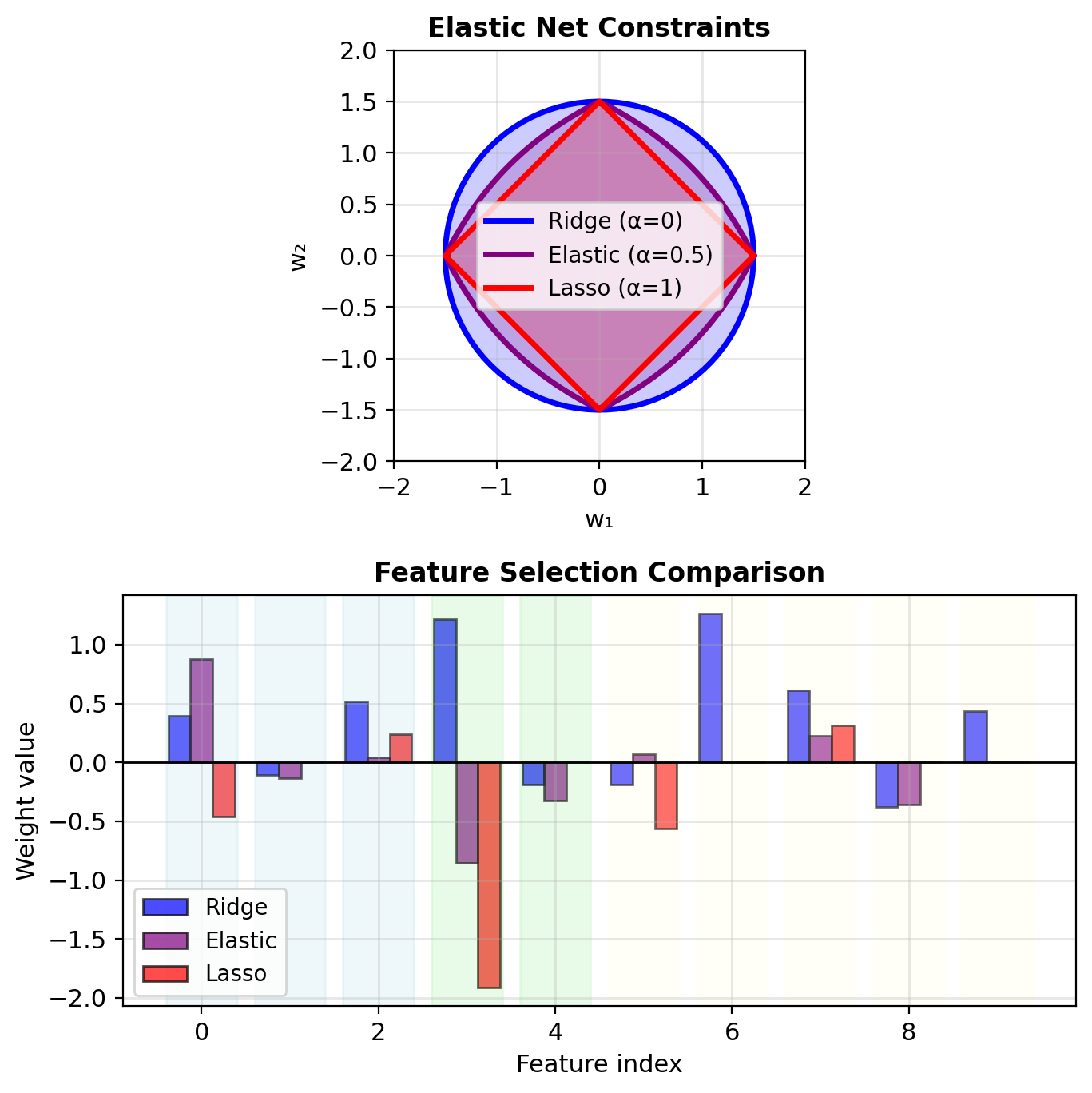

Elastic Net: Combined L1 and L2

Combine L1 and L2: \[\mathcal{L}_{\text{elastic}} = -\ell(\mathbf{w}) + \lambda_1 ||\mathbf{w}||_1 + \lambda_2 ||\mathbf{w}||^2\]

Alternative parameterization: \[= -\ell(\mathbf{w}) + \lambda\left[\alpha ||\mathbf{w}||_1 + \frac{1-\alpha}{2}||\mathbf{w}||^2\right]\]

where:

- \(\alpha = 1\): Pure L1 (Lasso)

- \(\alpha = 0\): Pure L2 (Ridge)

- \(0 < \alpha < 1\): Mix of both

Advantages:

- Sparsity from L1

- Grouping from L2 (correlated features)

- Stability when \(p > n\)

Elastic Net: Selects groups of correlated features

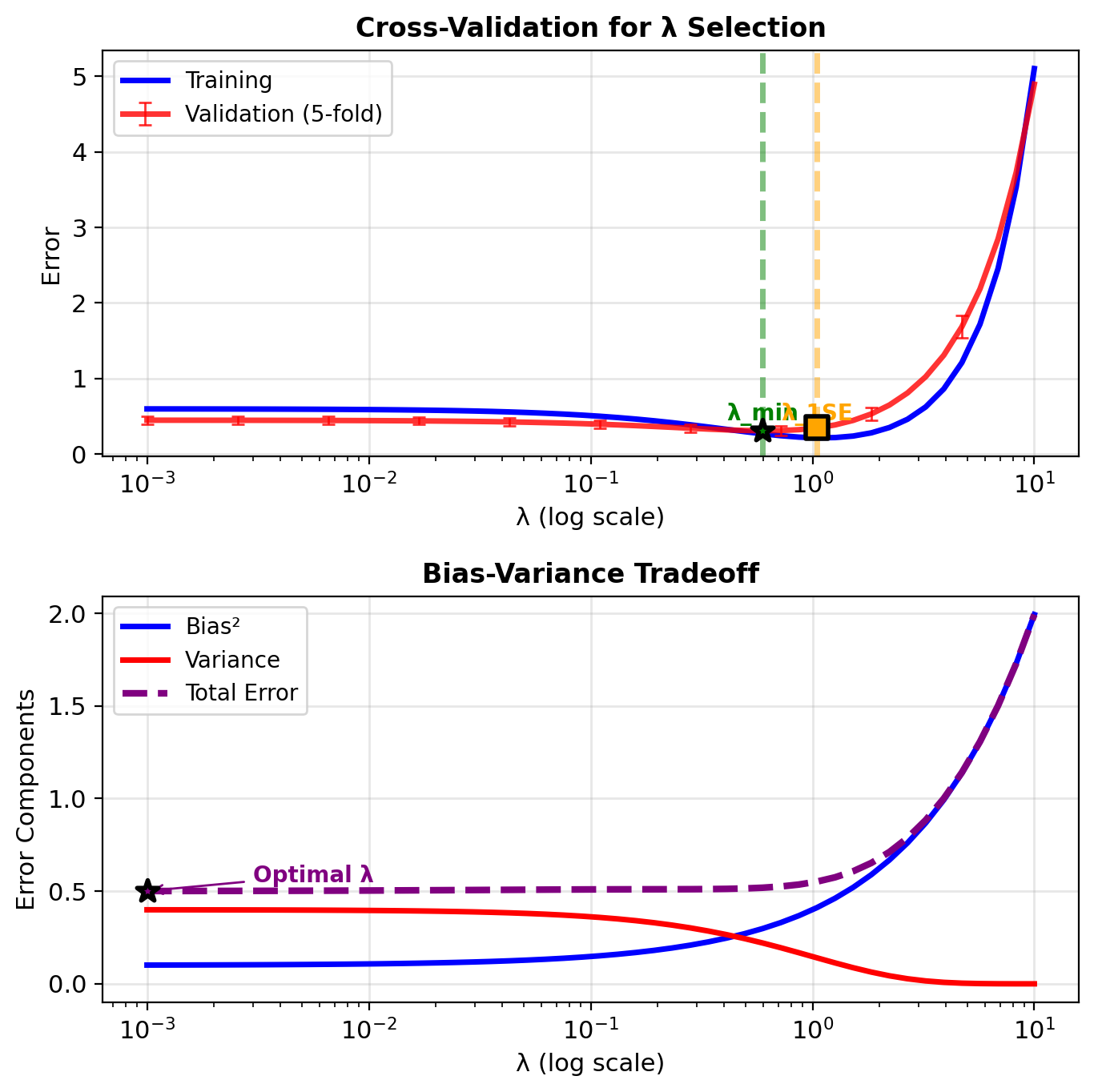

Choosing Regularization Strength (\(\lambda\)) by Cross-Validation

k-fold cross-validation:

Split data into \(k\) “folds”

For each \(\lambda\):

- Train on \(k-1\) folds

- Validate on remaining fold

- Repeat \(k\) times

Average validation error

Choose \(\lambda\) with lowest error

Common choices:

- \(k = 5\) or \(k = 10\)

- Leave-one-out: \(k = n\) (expensive)

One standard error rule:

- Find \(\lambda_{\text{min}}\) with minimum validation error

- Find largest \(\lambda\) within 1 standard error of minimum

- Choose simpler model (larger \(\lambda\)) when comparable

Larger λ within 1 SE yields simpler models with comparable performance

The “XOR Problem”

Linear decision boundaries cannot solve XOR.

XOR (Exclusive OR):

- (0,0) → Class 0 (blue)

- (0,1) → Class 1 (red)

- (1,0) → Class 1 (red)

- (1,1) → Class 0 (blue)

No linear boundary exists

Any line through the space:

- Misclassifies at least 2 points

- 50% accuracy at best

Logistic regression fails because: \[P(y=1|\mathbf{x}) = \sigma(\mathbf{w}^T\mathbf{x} + b)\] enforces linear decision boundary

Solution: Add hidden layer

- Transform features nonlinearly

- Create linearly separable representation

- 2 hidden units sufficient for XOR

Logistic Regression Computes Exactly One Neuron’s Forward Pass

Same equations, different vocabulary:

| Logistic Regression | Neural Network |

|---|---|

| \(z = \mathbf{w}^T\mathbf{x} + b\) | pre-activation |

| \(p = \sigma(z)\) | activation |

| \(\mathcal{L} = -[y\log p + (1-y)\log(1-p)]\) | cross-entropy loss |

| \(\nabla_\mathbf{w}\ell = (y-p)\mathbf{x}\) | backpropagation (1 layer) |

Forward pass: \[\mathbf{x} \to \mathbf{w}^T\mathbf{x} + b \to \sigma(\cdot) \to p\]

Backward pass (chain rule): \[\frac{\partial \ell}{\partial \mathbf{w}} = \underbrace{(y - p)}_{\partial \ell / \partial z} \cdot \mathbf{x}\]

A single neuron with sigmoid activation is logistic regression. The gradient computation is backpropagation through one layer.

Stacking Neurons Creates Nonlinear Decision Boundaries

Two-layer network: \[\mathbf{h} = \sigma(\mathbf{W}_1\mathbf{x} + \mathbf{b}_1)\] \[p = \sigma(\mathbf{w}_2^T\mathbf{h} + b_2)\]

- \(\mathbf{W}_1 \in \mathbb{R}^{m \times d}\): first layer weights

- \(\mathbf{h} \in \mathbb{R}^m\): hidden representation

- \(\mathbf{w}_2 \in \mathbb{R}^m\): output layer weights

What stays the same:

- Cross-entropy loss

- Gradient = (error \(\times\) features), extended by chain rule

What changes:

- Hidden layer learns representation \(\mathbf{h}\) where data becomes linearly separable

- Optimization is non-convex: multiple local minima, initialization matters

- Parameters: \((d+1)m + (m+1)\) vs \(d+1\) for logistic

Non-Convexity Means Initialization and Learning Rate Matter

Logistic regression (convex):

- Any starting point → global optimum

- Solution is unique (if \(\mathbf{X}\) full rank)

Neural networks (non-convex):

- Different initializations → different local minima

- Different minima → different generalization

Zero initialization breaks symmetry:

- All hidden units compute \(\sigma(\mathbf{0}^T\mathbf{x} + 0) = 0.5\)

- All receive identical gradients

- All learn the same function

- \(m\) hidden units collapse to 1

Random initialization:

- Breaks symmetry: each unit starts differently

- Scale matters: too large → saturation, too small → slow

Permutation symmetry: \(m\) hidden units → \(m!\) equivalent solutions from reordering alone

Adding Depth Changes Optimization, Not the Learning Principle

Logistic regression = neural network with 0 hidden layers

Adding layers:

- Same loss function (cross-entropy)

- Same gradient principle (chain rule extends naturally)

- New representational power: universal approximation with sufficient width

What breaks:

- Convex \(\to\) non-convex: no guarantee of global optimum

- Initialization matters (zero init causes symmetry problems)

- Multiple solutions with different generalization behavior

Parameter growth:

| Architecture | Parameters |

|---|---|

| Single neuron | \(d + 1\) |

| 1 hidden (\(m\) units) | \((d+1)m + (m+1)\) |

| \(L\) layers | \(\sum_{l=1}^{L} (d_{l-1}+1)d_l\) |